Filing Chapter 7 bankruptcy doesn’t mean losing everything you own. Federal and state exemption laws protect certain assets from liquidation, allowing you to keep your home, vehicle, retirement accounts, and essential household items.

At Hurst Law Firm, P.A., we help clients understand Chapter 7 exemptions basics so they can navigate this process with confidence. Knowing which property you can protect makes a real difference in your financial recovery.

How Exemptions Work in Chapter 7

Chapter 7 exemptions are state or federal laws that carve out specific assets you can keep when you file for bankruptcy. Without exemptions, the trustee appointed to your case would liquidate most of your property to pay creditors. Exemptions act as a shield, protecting essential items and equity in major assets so you retain the foundation for financial recovery. The moment you file, an automatic stay halts collection actions, and your exemption schedule tells the court exactly what property falls off-limits. This protection directly determines whether you walk away from bankruptcy with your home, vehicle, and retirement savings intact or lose them to the liquidation process.

Your State Determines What You Keep

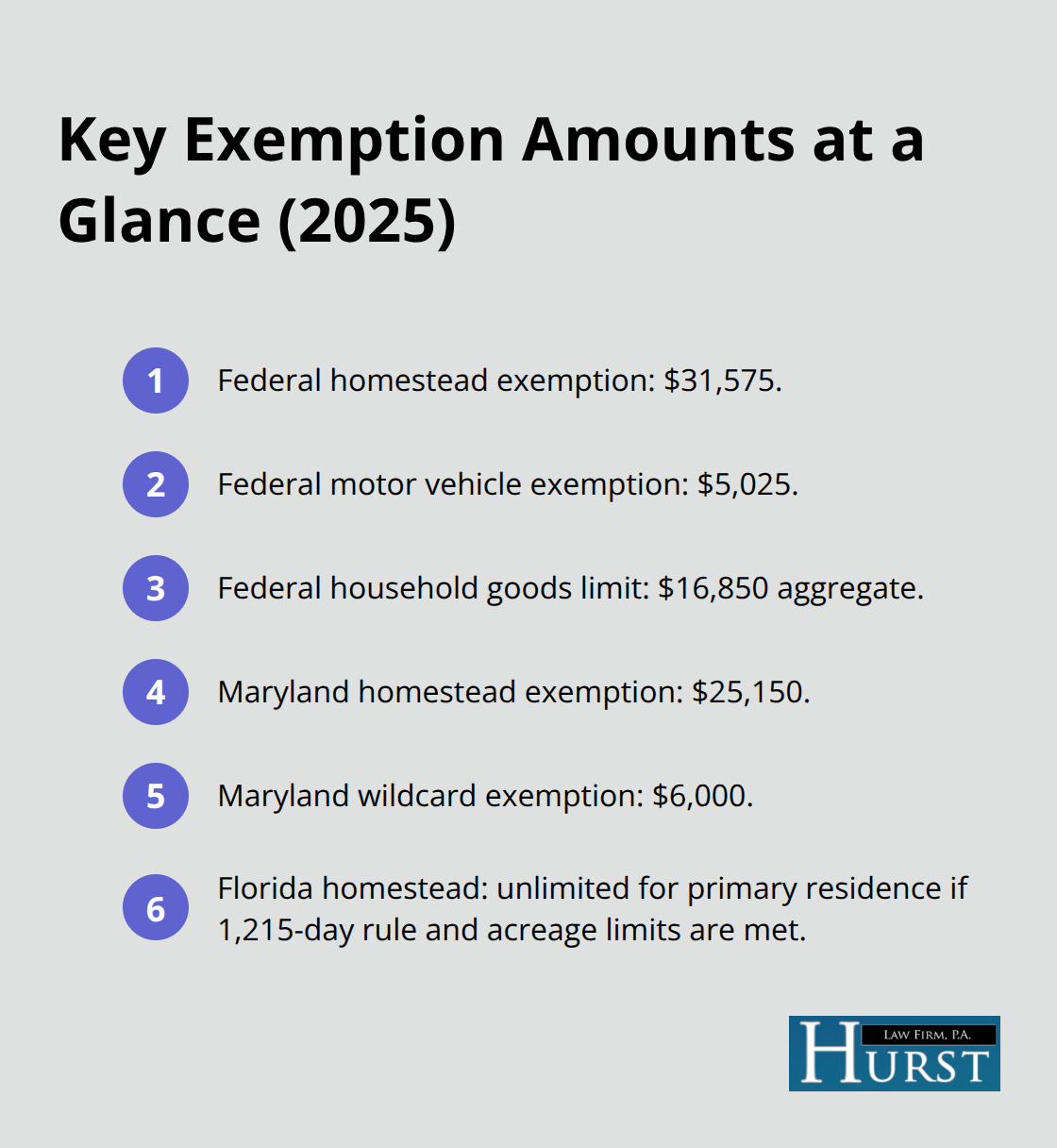

Your location matters enormously in Chapter 7. Some states allow you to elect federal exemptions under 11 U.S.C. § 522(d), while others require you to use only state exemptions. As of April 1, 2025, federal exemption amounts increased due to inflation adjustments under Bankruptcy Code § 104(b). The homestead exemption now stands at $31,575, motor vehicle exemption at $5,025, and household goods protection at $16,850 aggregate.

Maryland residents benefit from a $25,150 homestead exemption for owner-occupied real estate and a $6,000 wildcard exemption that protects additional assets like vehicle equity. Florida takes a dramatically different approach, offering unlimited homestead protection for primary residences if you meet the 1,215-day ownership requirement and property size limits of ½ acre inside cities or 160 acres outside. The difference between states is substantial-a $50,000 vehicle in Florida might receive complete protection under homestead rules, while in Maryland the same vehicle would require wildcard exemptions to shield equity beyond $1,000. You cannot assume your property is protected; the exemption laws of your specific state determine what actually stays with you.

Retirement Accounts and Personal Property Protection

Retirement accounts receive exceptional protection across nearly all states and federal law. Qualified IRAs, 401(k)s, and pension plans are exempt up to $1,711,975 in aggregate value, even in states that do not allow federal exemptions. This protection applies automatically without requiring you to list it separately on your exemption schedule. Household furnishings, clothing, books, and appliances typically fall within protected categories with dollar caps-Maryland exempts up to $1,000 of household goods per item, while federal law allows $800 per item with a $16,850 total limit. Tools of your trade receive protection if you use them to earn income; Maryland caps this at $5,000 for work-related equipment, clothing, and instruments.

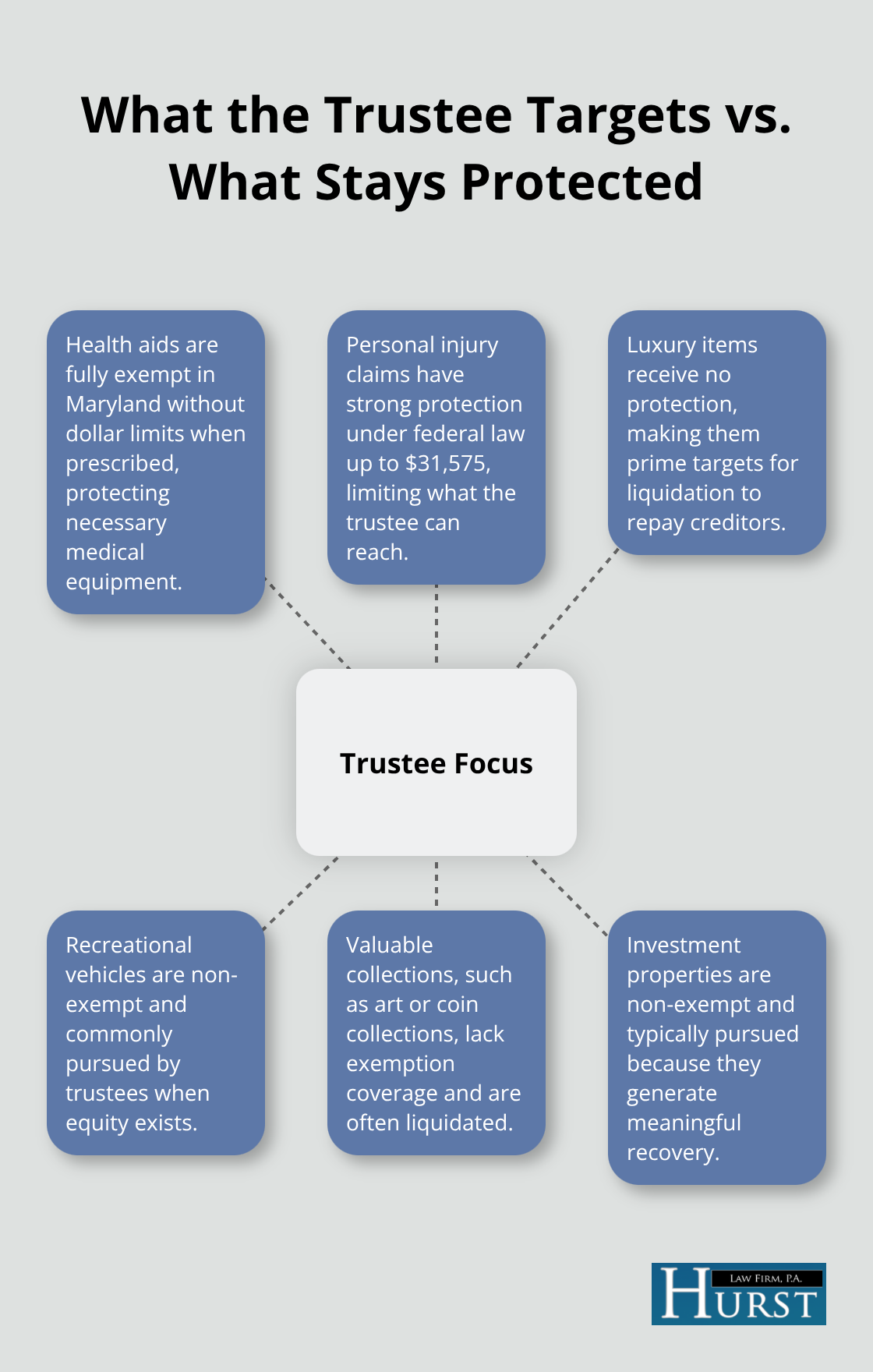

What the Trustee Will Pursue

Health aids prescribed by a professional are exempt without dollar limits in Maryland, covering medical equipment for you and your dependents. Personal injury settlements and court awards for injuries to your person (not property) receive strong protection-the federal personal injury claims exemption is now $31,575. Luxury items, recreational vehicles, valuable collections, and investment properties receive no protection under exemption laws. The trustee will pursue these assets aggressively because they generate meaningful recovery for creditors.

Your jewelry exemption under federal law is $2,125, and life insurance proceeds are protected only when your spouse or dependent child is the beneficiary. Understanding these categories prevents surprises during the 341 meeting when the trustee questions your property valuations and exemption claims. The specific assets you list on your exemption schedule directly affect what the trustee can seize, making accuracy and completeness essential as you prepare your bankruptcy filing.

What Property You Actually Keep in Chapter 7

Your Home and Homestead Protection

Your home represents the single largest asset most people protect in Chapter 7, and homestead exemptions determine whether you keep it or lose it to the trustee. If you live in Florida and own your primary residence, you benefit from unlimited homestead protection as long as you meet two conditions: you must have owned the property for at least 1,215 days before filing, and the property must not exceed ½ acre inside city limits or 160 acres outside them. This means a $500,000 home with $400,000 in equity receives complete protection in Florida Chapter 7, a reality that makes Chapter 7 genuinely attractive for Florida homeowners drowning in unsecured debt.

Maryland offers substantially less generous protection with a $25,150 homestead exemption, meaning you keep that amount of equity and lose anything above it to the trustee unless other exemptions apply. Federal exemptions provide $31,575 for homestead protection as of April 1, 2025, following the inflation adjustment that occurs every three years under Bankruptcy Code § 104(b).

Calculate your home equity before filing: take your home’s current fair market value, subtract your mortgage balance and any liens, and compare the result to your state’s homestead exemption limit. If your equity falls below the exemption, your home stays completely protected. If equity exceeds the limit, you face a choice: proceed with Chapter 7 knowing the trustee will pursue the excess equity, or explore Chapter 13 to protect the home by repaying debt over three to five years. Married couples filing jointly can double federal homestead exemptions in most cases, but not in Maryland, so your filing status matters significantly.

Vehicles and How Liens Affect Protection

Your vehicle exemption under federal law is $5,025 as of April 2025, while Maryland limits vehicle protection to $1,000 unless you apply the wildcard exemption for additional coverage. If you own a financed vehicle, the trustee cannot seize it as long as you continue making payments because the lender holds a secured interest that survives bankruptcy.

If you own a vehicle free and clear worth $8,000 and live in Maryland, you lose $7,000 of equity to the trustee unless you use your $6,000 wildcard exemption to protect additional vehicle equity, leaving $1,000 unprotected. The trustee will pursue vehicles aggressively when equity exceeds exemption limits because they generate meaningful recovery for creditors.

Retirement Accounts and Education Savings

Retirement accounts including IRAs, 401(k)s, and pension plans receive exceptional treatment: the aggregate exemption is $1,711,975, and this protection applies automatically without requiring separate action on your exemption schedule. Education savings accounts including 529 plans and ABLE accounts receive exclusion from your bankruptcy estate entirely if you funded them 365 to 720 days before you filed, with a maximum exclusion of $8,575 per account. The practical takeaway is that retirement savings face virtually no risk in Chapter 7 regardless of your state, making them genuinely safe from creditors.

Household Goods and Personal Property

Household goods including furniture, appliances, clothing, and books receive protection up to $1,000 per item with an aggregate federal limit of $16,850, while Maryland caps household goods at $1,000 total. Luxury items, jewelry beyond $2,125 in federal exemptions, and recreational vehicles receive zero protection, so the trustee will pursue them aggressively if you own them.

Understanding what the trustee can and cannot seize shapes your entire Chapter 7 strategy. The next section walks you through the actual process of claiming these exemptions on your bankruptcy filing and what happens when the trustee questions your valuations.

Claiming Exemptions in Your Chapter 7 Filing

Filing Schedule C with the Bankruptcy Court

Claiming exemptions happens through specific schedules you file with the bankruptcy court, not through a separate application or request. When you file your Chapter 7 petition, you must complete Schedule C, which lists every asset you claim as exempt and identifies which exemption law protects it. The court requires you to cite the specific statute-for example, 11 U.S.C. § 522(d)(1) for federal homestead protection or Maryland Code Ann., Real Prop. § 8-201 for state homestead exemptions. Accuracy matters intensely here because incomplete or incorrect listings give the trustee grounds to challenge your exempt property or seize property you thought was protected.

You must list the property description, its estimated fair market value, the amount of equity you claim is exempt, and the exemption statute that applies. If you own a $200,000 home with a $150,000 mortgage in Maryland, you would list the home’s value, calculate $50,000 equity, and cite the $25,150 homestead exemption-meaning $24,850 becomes available for the trustee to pursue unless other exemptions apply.

Filing Fees and Credit Counseling Requirements

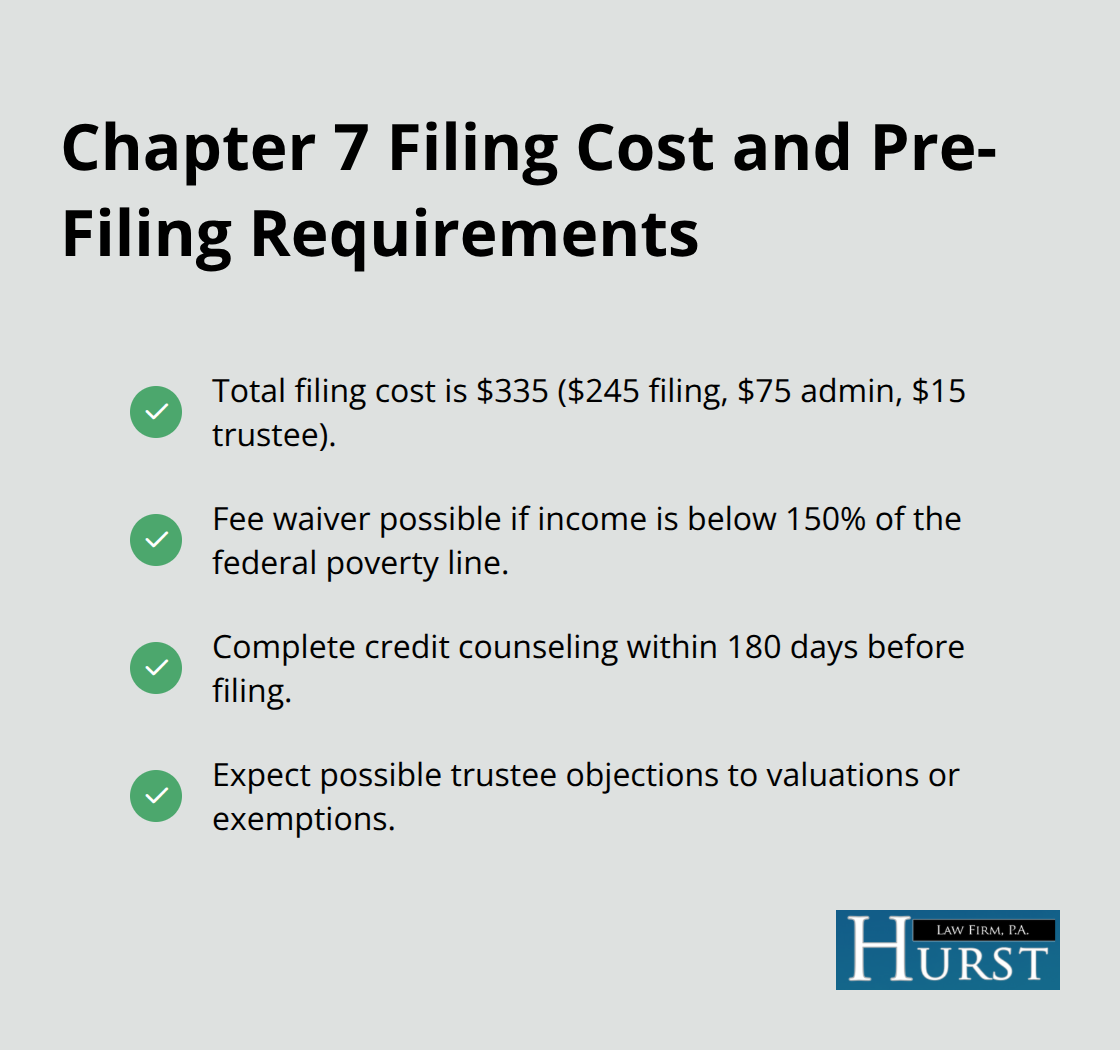

The filing fee for Chapter 7 is $245 plus a $75 administrative fee and $15 trustee surcharge, totaling $335. You can request a waiver if your income falls below 150% of the federal poverty line. Before filing, you must complete credit counseling within 180 days, which confirms you understand your options and have considered alternatives to bankruptcy.

The trustee receives your exemption schedule immediately and has the right to object if they believe your valuations are inflated or your exemptions are improper.

Preparing for the 341 Meeting

The 341 meeting, held approximately 21 to 40 days after filing, is where the trustee directly examines your exemptions and property valuations under oath. Bring documentation supporting every significant asset you claimed as exempt-recent home appraisals, vehicle market value reports from Kelley Blue Book or NADA Guides, retirement account statements, and receipts for household goods. The trustee will ask specific questions about how you determined values, whether liens exist on property you listed, and whether you own assets you failed to disclose.

If your vehicle valuation is $8,000 but you provide no documentation and the trustee knows similar vehicles sell for $12,000, they will challenge your exemption and pursue the additional equity. Conversely, if you bring a current appraisal showing your home’s value is $180,000 rather than the $220,000 you initially estimated, the trustee may abandon pursuit because lower equity means less recovery.

Responding to Exemption Challenges

The discharge typically enters 60 to 90 days after the 341 meeting, but this timeline assumes no exemption challenges occur. If the trustee objects to your claimed exemptions, you must respond within 14 days with additional evidence or written arguments explaining why the exemption applies. Exemption disputes can be litigated in bankruptcy court, and if you lose, property previously thought protected becomes available for liquidation. This is why filing accurate values from the start prevents costly disputes later.

Final Thoughts

Chapter 7 exemptions basics determine what you keep and what you lose when you file for bankruptcy. Your state’s exemption laws create the actual boundaries of what stays with you, and those boundaries vary dramatically depending on where you live. A homeowner in Florida with $400,000 in home equity keeps everything, while the same homeowner in Maryland loses most of that equity unless other exemptions apply.

Retirement accounts receive exceptional protection across all states, household goods and vehicles receive limited protection with specific dollar caps, and luxury items receive no protection at all. Calculate your home equity, vehicle equity, and personal property values honestly, then compare those numbers to your state’s exemption limits. If your assets exceed exemptions significantly, Chapter 13 may protect more property by allowing you to repay debt over time rather than liquidating assets immediately.

Consulting with a bankruptcy attorney who understands your state’s exemption rules protects you from losing assets you thought were safe. We at Hurst Law Firm, P.A. help Memphis residents navigate Chapter 7 and determine whether Chapter 7 or Chapter 13 makes sense for your circumstances. Contact us to discuss your Chapter 7 options and start moving toward financial recovery.