Debt can feel overwhelming, but you have real options. Chapter 7 bankruptcy offers Memphis residents a legitimate path to eliminate unsecured debts and start fresh.

At Hurst Law Firm, P.A., we help people understand their Memphis bankruptcy options in 2025. This guide walks you through Chapter 7 from start to finish, so you can make an informed decision about your financial future.

How Chapter 7 Works and Who Qualifies

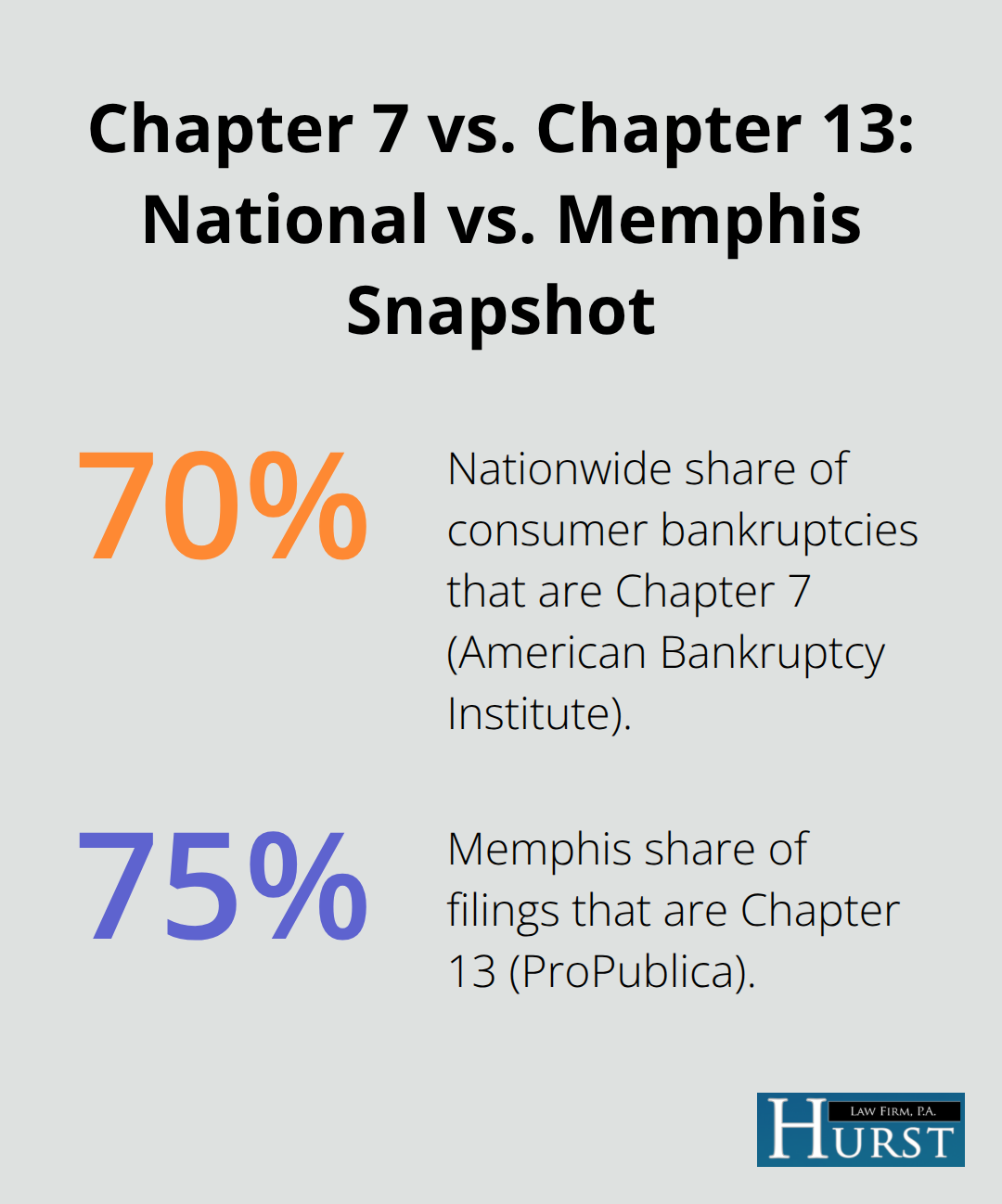

Chapter 7 bankruptcy is straightforward: you file a petition, list your debts and assets, and a trustee liquidates non-exempt property to pay creditors. Most unsecured debts-credit cards, medical bills, personal loans-are discharged, meaning you no longer owe them. The American Bankruptcy Institute reports that Chapter 7 accounts for roughly 70% of consumer bankruptcy filings nationwide because it delivers fast relief. In Memphis specifically, about 75% of bankruptcy filings are Chapter 13 cases, according to ProPublica, which means Chapter 7 filers choose a less common but often more efficient path.

The entire process typically takes 3 to 6 months from filing to discharge in Memphis, and the court filing fee is $338 (though you can request a waiver if you cannot afford it).

Income Thresholds Determine Your Eligibility

The means test determines whether you qualify for Chapter 7. As of 2025, single filers in Tennessee must have income under $39,759 over the past six months to pass the initial threshold; a family of four must be under $93,767. These numbers are based on the Tennessee median income and change annually. If your income exceeds these limits, you do not automatically disqualify-the means test allows deductions for necessary expenses like housing, utilities, and food. After subtracting allowed expenses, if you have little to no disposable income remaining, you may still qualify. The means test was designed to identify people who genuinely cannot pay their debts, not those with significant monthly surplus income.

Asset Exemptions Protect What Matters

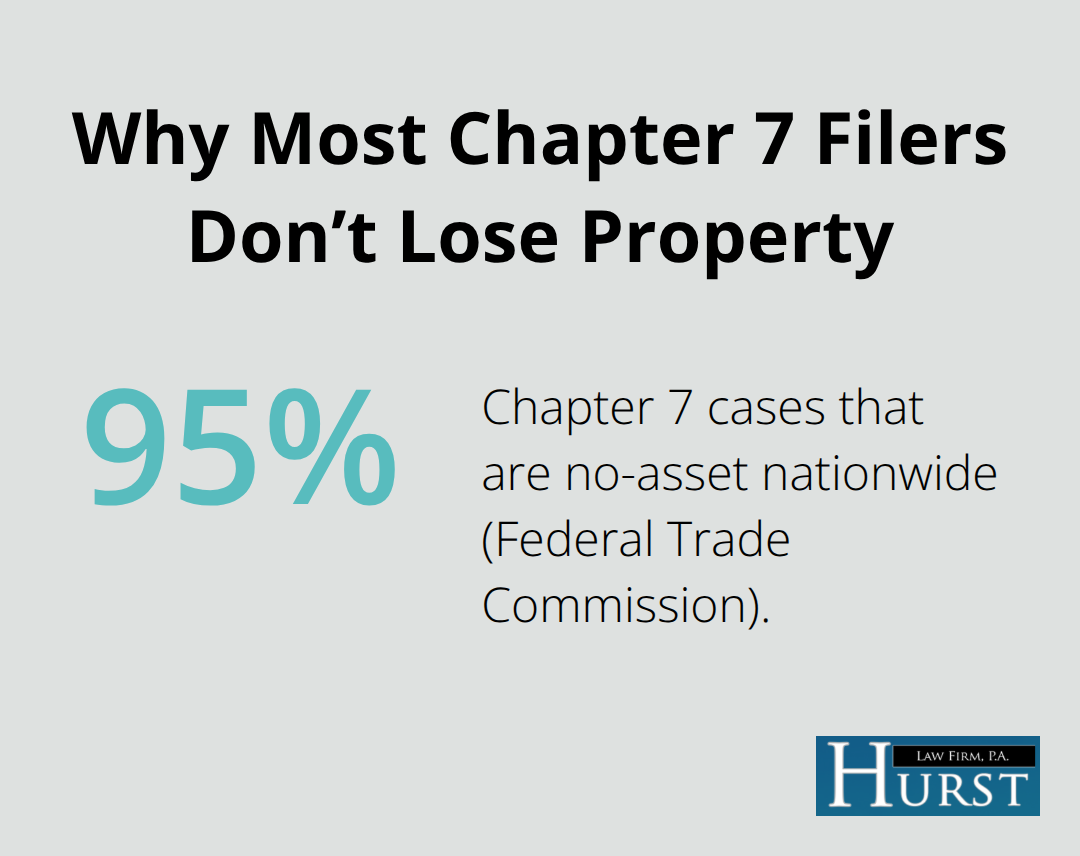

Tennessee law protects certain assets in Chapter 7 cases. Your primary residence receives a homestead exemption of up to $5,000 in equity (or $7,500 for married couples), meaning you can keep your home if your equity falls within that limit. Personal property exemptions also shield clothing, household goods, and other essentials. The Federal Trade Commission reports that more than 95% of Chapter 7 filings nationwide are no-asset cases, meaning most filers have no non-exempt assets for the trustee to liquidate. This matters because it means Chapter 7 often results in debt discharge without losing significant property.

When Your Assets Suggest a Different Path

If you own a home with substantial equity or valuable assets, Chapter 7 may not be your best option. High-equity homeowners risk liquidation under Chapter 7, which is why Chapter 13 becomes the better choice for those situations. Chapter 13 allows you to keep everything while repaying debts through a structured plan over three to five years. Understanding whether your assets fit Chapter 7 or Chapter 13 requires looking at your specific situation-and that comparison is exactly what we explore next.

From Filing to Discharge: What to Expect

Prepare Your Documents and Complete Credit Counseling

Getting your Chapter 7 case started requires preparation and focus. Before you file, you must complete a free credit counseling session with a court-approved agency-this is mandatory and typically takes about two hours. During this session, you will review your budget, explore alternatives to bankruptcy, and receive a certificate proving completion. This certificate must accompany your petition or the court will dismiss your case. Gather your financial documents next: pay stubs from the last six months, tax returns for the past two years, bank statements, a list of all debts with creditor names and account numbers, and documentation of your assets. The $338 filing fee applies unless you request a fee waiver, which the court grants based on your inability to pay. This preparation phase typically takes two to four weeks and determines whether your case moves forward smoothly or encounters delays.

File Your Petition and Activate the Automatic Stay

Once you file your petition in the Western District of Tennessee, the automatic stay takes effect immediately-creditors must stop collection calls, wage garnishment, repossession attempts, and foreclosure actions. This relief is not temporary; it lasts throughout your case and provides genuine breathing room. The means test calculation verifies your income qualifies under Tennessee’s thresholds and forms the foundation of your filing. Within 21 to 40 days, you attend the 341 meeting of creditors, a brief hearing where the trustee reviews your documents and asks questions about your assets, debts, and financial situation.

Attend Your Meeting and Receive Your Discharge

Most Chapter 7 meetings last five to ten minutes, and creditors rarely attend. After the meeting, the trustee has 60 days to investigate whether non-exempt assets exist to liquidate. Since over 95% of Chapter 7 cases nationwide are no-asset cases according to the Federal Trade Commission, most filers face no asset liquidation.

If the trustee finds no assets worth pursuing, your discharge typically arrives within three to six months from filing. The discharge order eliminates your legal obligation to pay unsecured debts, though certain debts like student loans, child support, and recent tax obligations remain non-dischargeable. This timeline is predictable and manageable-most Memphis filers complete the entire process without surprises if they stay organized and responsive to trustee requests.

Understanding what happens to your debts after discharge matters just as much as the filing process itself, and that fresh start requires knowing exactly which obligations disappear and which ones remain.

Chapter 7 or Chapter 13: How to Choose the Right Path

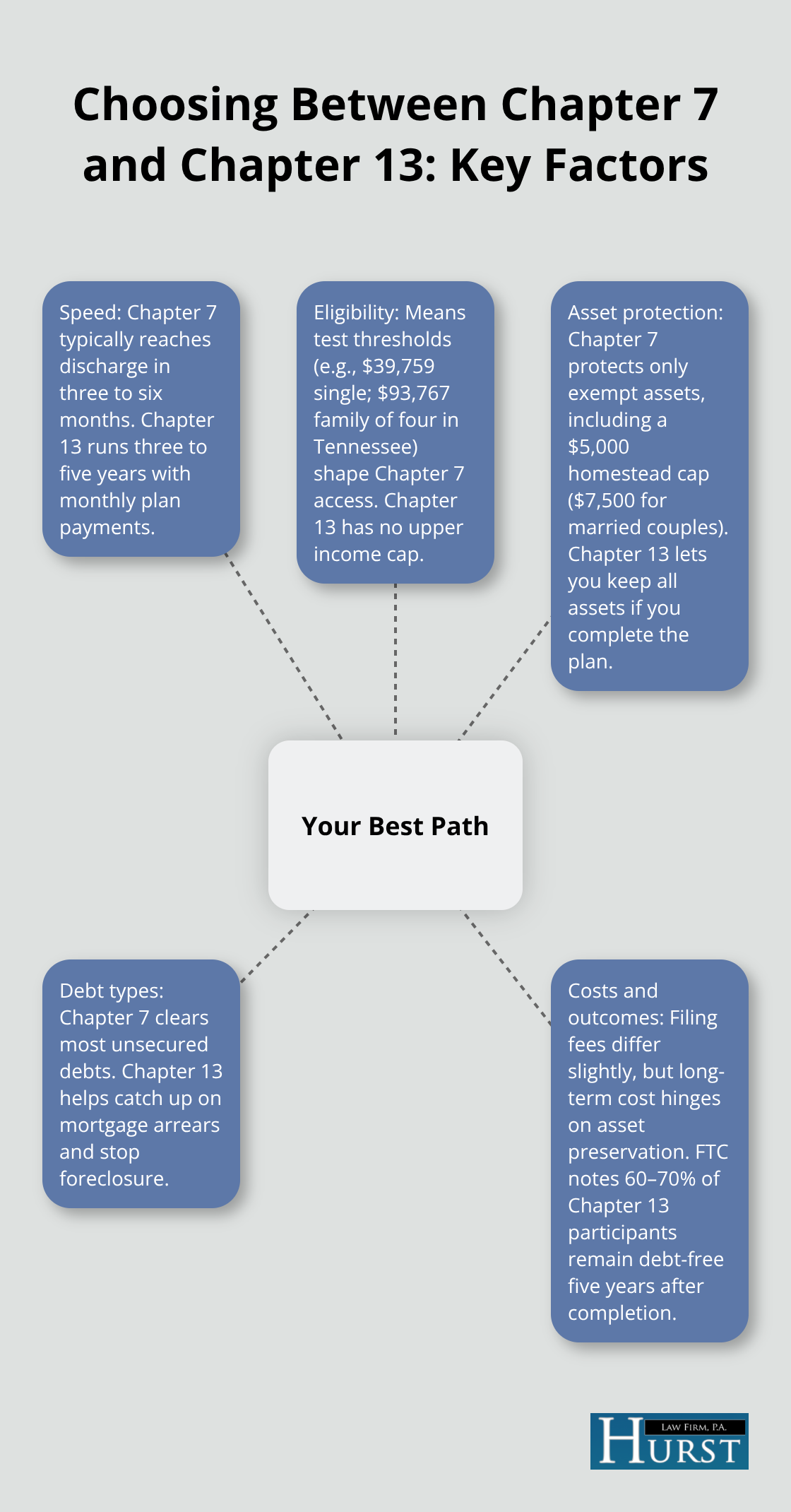

Speed and Timeline Shape Your Decision

The speed of Chapter 7 appeals to many Memphis residents, but it is not always the right choice. Chapter 7 delivers discharge in three to six months and eliminates most unsecured debts permanently. Chapter 13, by contrast, requires a three to five year commitment with monthly payments to a court-appointed trustee. The American Bankruptcy Institute reports that Chapter 7 accounts for roughly 70% of consumer filings nationwide, yet in Memphis specifically, about 75% of filers choose Chapter 13 according to ProPublica. This local pattern reveals something important: Memphis residents often have assets or income levels that make Chapter 13 more practical, even though Chapter 7 is faster.

Income Thresholds Determine Your Eligibility Path

Your income and disposable income determine eligibility for Chapter 7. Single filers earning under $39,759 and families of four earning under $93,767 can qualify for Chapter 7 under the 2025 Tennessee means test. If your income exceeds these thresholds, Chapter 13 becomes your only option because there is no upper income cap for Chapter 13 eligibility. The means test calculation subtracts allowed expenses from your income, so earning above the threshold does not automatically disqualify you if your disposable income remains low.

Asset Protection Favors Chapter 13 for Homeowners

Your assets matter enormously when you choose between these paths. Chapter 7 allows you to keep only exempt property, with homestead protection capped at $5,000 in equity for your primary residence. If you own a home with $50,000 in equity or a vehicle worth $15,000, Chapter 7 puts those assets at risk of liquidation. Chapter 13 protects all your assets as long as you complete your plan and stay current with payments. This protection makes Chapter 13 the practical choice for Memphis homeowners facing foreclosure or those who want to preserve significant property.

Debt Types and Your Financial Goals

Your debt types shape the outcome of each bankruptcy path. Chapter 7 discharges credit cards, medical bills, and personal loans but leaves student loans, child support, and most tax obligations untouched. Chapter 13 can address mortgage arrears, allowing you to catch up on missed payments through your plan while keeping your home. If you have missed mortgage payments, Chapter 13 stops foreclosure and restructures your obligation into a manageable repayment schedule.

Comparing Costs and Long-Term Outcomes

A Chapter 13 filing costs $313 in court fees compared to $338 for Chapter 7, but the real financial comparison extends beyond filing fees. Chapter 13 lets you keep property worth tens of thousands of dollars, while Chapter 7 may force liquidation of non-exempt assets. The Federal Trade Commission reports that 60 to 70% of Chapter 13 participants remain debt-free five years after completing their plans, showing that those who commit to the process succeed. Memphis filers often discover that Chapter 13 actually costs less than Chapter 7 when you factor in asset losses and long-term financial stability. The wrong choice can cost thousands in unnecessary asset liquidation or years of unnecessary payments. We at Hurst Law Firm, P.A. help you evaluate whether your home equity, vehicle, income level, and debt composition point toward Chapter 7 or Chapter 13. Contact us at 901-725-1000 or visit our office at 2287 Union Avenue to discuss your specific situation and determine which bankruptcy path actually fits your financial reality.

Your Fresh Start Begins Now

Once the court grants your Chapter 7 discharge, your legal obligation to pay unsecured debts vanishes. Credit cards, medical bills, and personal loans no longer haunt you, and this discharge is permanent and cannot be reversed. Student loans, child support, and most tax obligations remain, but the weight of consumer debt lifts immediately, giving you genuine financial breathing room to rebuild.

Your credit score recovers faster than many people expect after Chapter 7. With responsible credit use, many Chapter 7 filers reach credit scores above 650 within two to three years, and lenders focus more on recent activity than old bankruptcy filings. Opening a secured credit card, making on-time payments, and keeping credit utilization low accelerates your recovery (the Federal Trade Commission reports that consistent, responsible behavior after discharge produces measurable credit improvement within months, not years).

We at Hurst Law Firm, P.A. understand that navigating Memphis bankruptcy options 2025 feels overwhelming, but you do not have to face this alone. Contact us at 901-725-1000 or visit us at 2287 Union Avenue to discuss your situation and take the first step toward financial freedom.