Chapter 13 bankruptcy help starts with understanding what your repayment plan actually does and how to build one that survives the full 3 to 5 years ahead.

Most people filing Chapter 13 make preventable mistakes-underestimating expenses, ignoring income changes, or misunderstanding their commitment. We at Hurst Law Firm, P.A. in Memphis TN have seen these errors derail plans that could have worked.

This guide walks you through the real mechanics of Chapter 13 and shows you how to construct a plan with honest numbers from the start.

How Chapter 13 Reorganizes Your Financial Life

Chapter 13 bankruptcy restructures your debts into a single repayment plan lasting three to five years, with payments going directly to a court-appointed trustee who distributes money to your creditors according to a strict priority system. The moment you file, an automatic stay takes effect under 11 U.S.C. § 362, which stops wage garnishments, collection calls, lawsuits, and foreclosure proceedings immediately. This isn’t a theoretical protection-creditors must cease collection efforts the same day your case is filed. Your secured debts, like mortgages and car loans, get paid through the plan while you keep the property itself. Unsecured debts like credit cards and personal loans are reorganized so you pay what you can afford rather than facing aggressive collection tactics. The plan forces creditors to accept partial or full repayment on your timeline instead of their demands.

What Happens to Your Home and Assets

Chapter 13 allows you to keep your house, car, and personal belongings while you repay debts. If you fall behind on mortgage payments, the plan cures those arrears over the life of the case, meaning you catch up on past-due amounts while continuing regular monthly payments. Many people facing foreclosure stop the process entirely through Chapter 13 filing. Your retirement accounts like 401(k)s and IRAs remain protected and untouched-the bankruptcy code prevents creditors from forcing withdrawals to pay debts. Vehicle loans can be restructured through cramdown provisions, potentially lowering your monthly car payment if the vehicle’s current value is less than what you owe. You retain assets rather than liquidate them as in Chapter 7; instead, you reorganize how you pay what you owe.

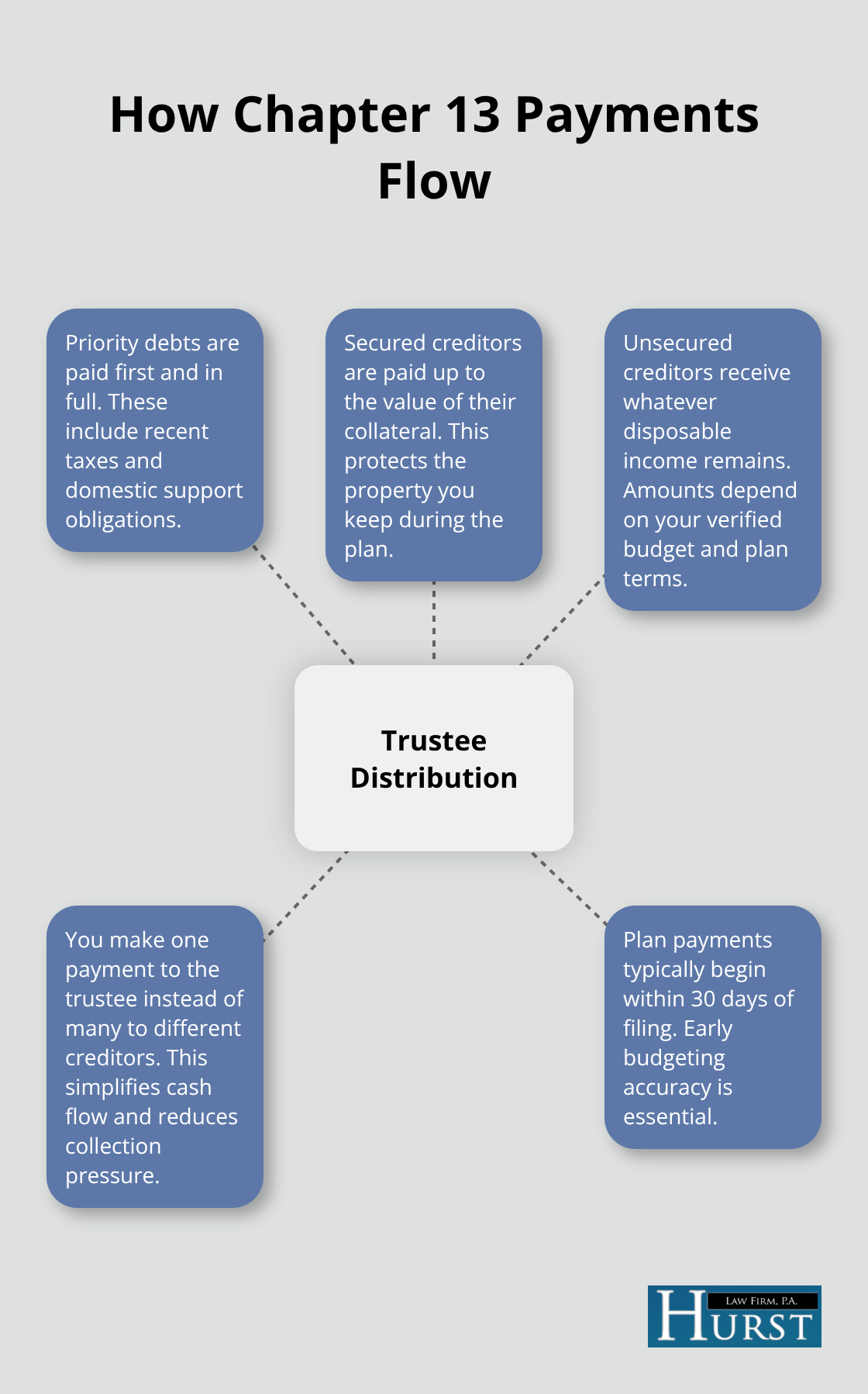

How the Trustee Collects and Distributes Your Payments

The Chapter 13 trustee collects your monthly or biweekly payments and distributes them according to the confirmed plan’s priority structure. Priority debts like recent taxes and child support receive payment first and in full. Secured creditors receive enough to cover the value of their collateral. Unsecured creditors receive whatever disposable income remains after you cover living expenses and priority obligations.

This system (governed by 11 U.S.C. § 1322 and § 1325) removes the burden of negotiating directly with each creditor. You make one payment to one trustee instead of juggling multiple creditors with conflicting demands. Plan payments typically begin within 30 days of filing, so you need a realistic budget from day one.

Why Your Budget Determines Plan Success

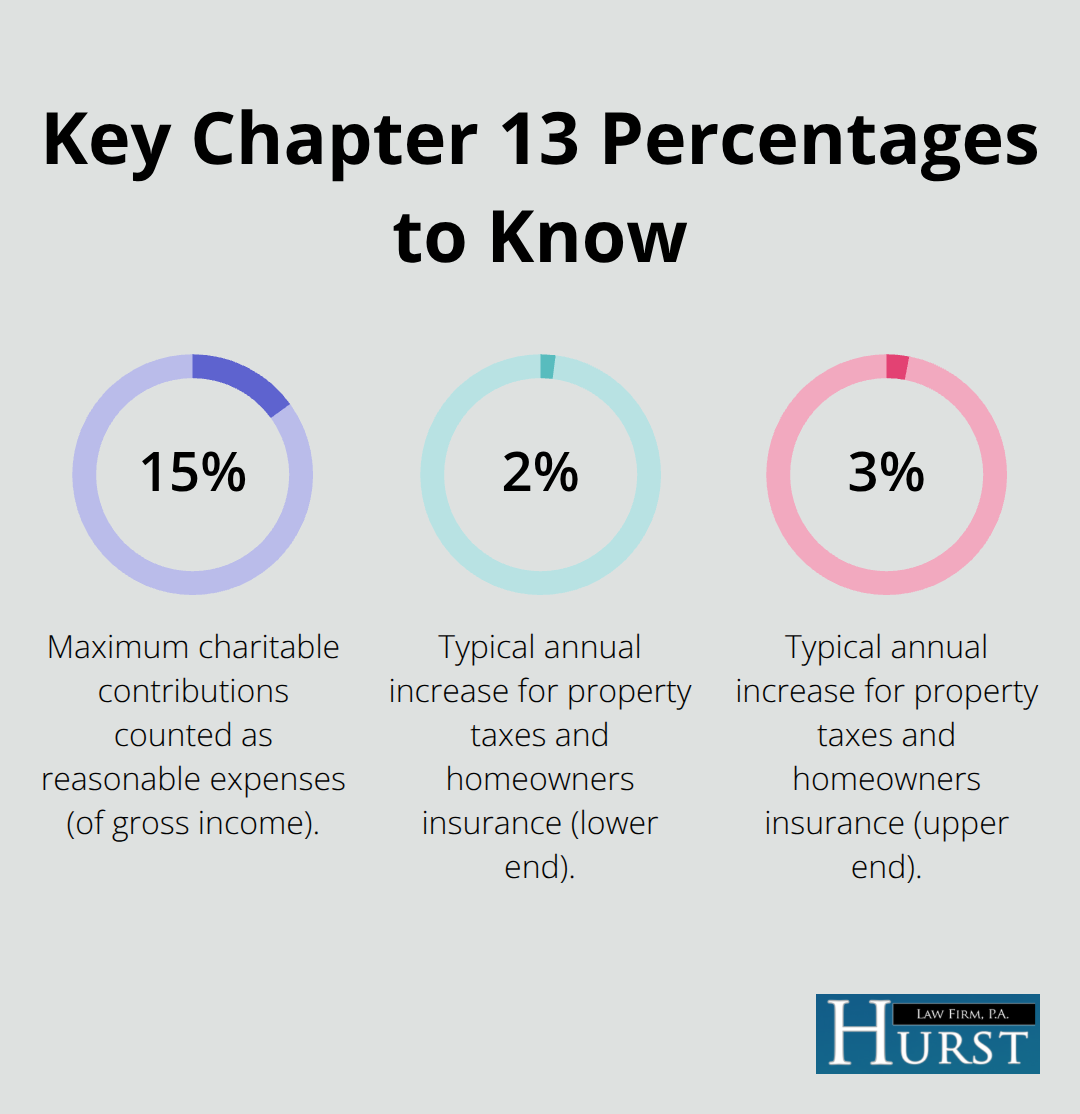

The trustee and court examine your disposable income-what remains after you subtract reasonable living expenses and certain charitable contributions (up to 15% of gross income) from your monthly earnings. This calculation determines how much you actually pay toward debts each month. If your budget inflates expenses or underestimates income, the court will reject your plan at the confirmation hearing. Creditors object when they see unrealistic numbers because they know the plan will fail. The court applies the best interests test, meaning unsecured creditors must receive at least what they would get in a Chapter 7 liquidation. Your honest numbers protect the plan’s viability and move you toward discharge. Understanding this connection between accurate budgeting and plan confirmation shapes everything that follows in your case.

Where Chapter 13 Plans Actually Fail

Most Chapter 13 plans collapse not because the law is unfair, but because people build budgets disconnected from reality. Unrealistic figures trigger objections at the confirmation hearing that delay or kill your plan. The trustee and creditors scrutinize these numbers carefully-someone estimates their grocery bill at $300 monthly when they actually spend $450, or they ignore the annual property tax increase that will hit their budget in year two. The court applies the disposable income test under 11 U.S.C. § 1325(b)(2), which means every dollar of your actual discretionary income must go toward the plan. If you underestimate expenses, you commit to a higher monthly payment than you can sustain. When the payment becomes unaffordable six months in, you miss it, and the trustee can move to dismiss your case or convert it to Chapter 7 liquidation. The difference between a plan that survives five years and one that fails is often just $50 or $100 monthly-the gap between what you claimed you’d spend and what you actually spend on utilities, insurance, gas, or groceries.

Income Changes Derail Plans Built on False Assumptions

Income changes wreck plans because people treat their current job as permanent. A salary increase looks good until you realize the court will demand that extra money go into the plan, extending your payments or forcing a modification. Job loss, reduced hours, or commission fluctuations are common in the real world, yet many debtors build plans assuming flat income for 60 months straight. The Bankruptcy Code measures current monthly income as the six-month average before filing under 11 U.S.C. § 101(10A), so seasonal workers or commission-based earners often overstate what they’ll actually earn going forward. If your income drops after confirmation, you can modify the plan, but modification takes time and court approval-months where you still owe the original payment amount.

Hidden Costs Emerge Over Three to Five Years

The three-to-five-year commitment itself trips up filers who underestimate how long this process actually feels. Five years of sending money to a trustee instead of paying down debts directly creates psychological fatigue. Property taxes rise. Insurance premiums increase. Medical expenses emerge. Children age into new costs. A realistic plan accounts for these predictable increases before you file, not after the court confirms your case. These expenses (property taxes, insurance, and childcare) grow steadily throughout your plan term, yet most budgets treat them as static numbers locked in at filing. The court expects you to absorb these increases within your existing disposable income, which means your actual financial flexibility shrinks each year even if your income stays flat.

Why Accurate Numbers Matter Before You File

Building an honest budget from the start protects your plan’s viability and moves you toward discharge. The trustee and court examine your disposable income-what remains after you subtract reasonable living expenses and certain charitable contributions (up to 15% of gross income) from your monthly earnings. This calculation determines how much you actually pay toward debts each month. Creditors object when they see unrealistic numbers because they know the plan will fail. The court applies the best interests test, meaning unsecured creditors must receive at least what they would get in a Chapter 7 liquidation. Your honest numbers satisfy this requirement and prevent the objections that derail cases before confirmation even happens.

Understanding where plans fail reveals what you must do differently when you construct yours.

How to Build Your Chapter 13 Plan With Honest Numbers in Memphis TN

Calculate Your Real Monthly Income

Start with your actual take-home pay over the last six months, not what you hope to earn. The Bankruptcy Code under 11 U.S.C. § 101(10A) measures current monthly income as your average earnings during the six calendar months before filing, which means seasonal income swings, bonuses, or commission fluctuations get averaged into a single figure. Many filers artificially inflate this number by including overtime they rarely work or bonuses that come sporadically. The trustee pulls your tax returns and pay stubs to verify this calculation, so inflating income gets caught immediately at the confirmation hearing.

Subtract Every Legitimate Living Expense

Once you have your real monthly income, subtract every legitimate living expense: rent or mortgage, utilities, groceries, transportation, insurance, childcare, and medical costs. The court allows reasonable expenses under 11 U.S.C. § 1325(b)(2), which means your grocery budget must reflect what you actually spend, not a theoretical minimum. Property taxes and homeowners insurance increase annually (typically 2 to 3 percent per year according to the National Association of REALTORS), so your year-one budget cannot be your year-five budget. You can also deduct charitable contributions up to 15 percent of your gross income, which some filers use strategically to reduce disposable income.

The number that remains after all legitimate expenses becomes your disposable income, and that becomes your monthly plan payment. If you overstate expenses here, creditors object and the court reduces your payment, forcing you to commit more of your actual income to the plan. If you understate expenses, you commit to a payment you cannot afford and your plan fails within months.

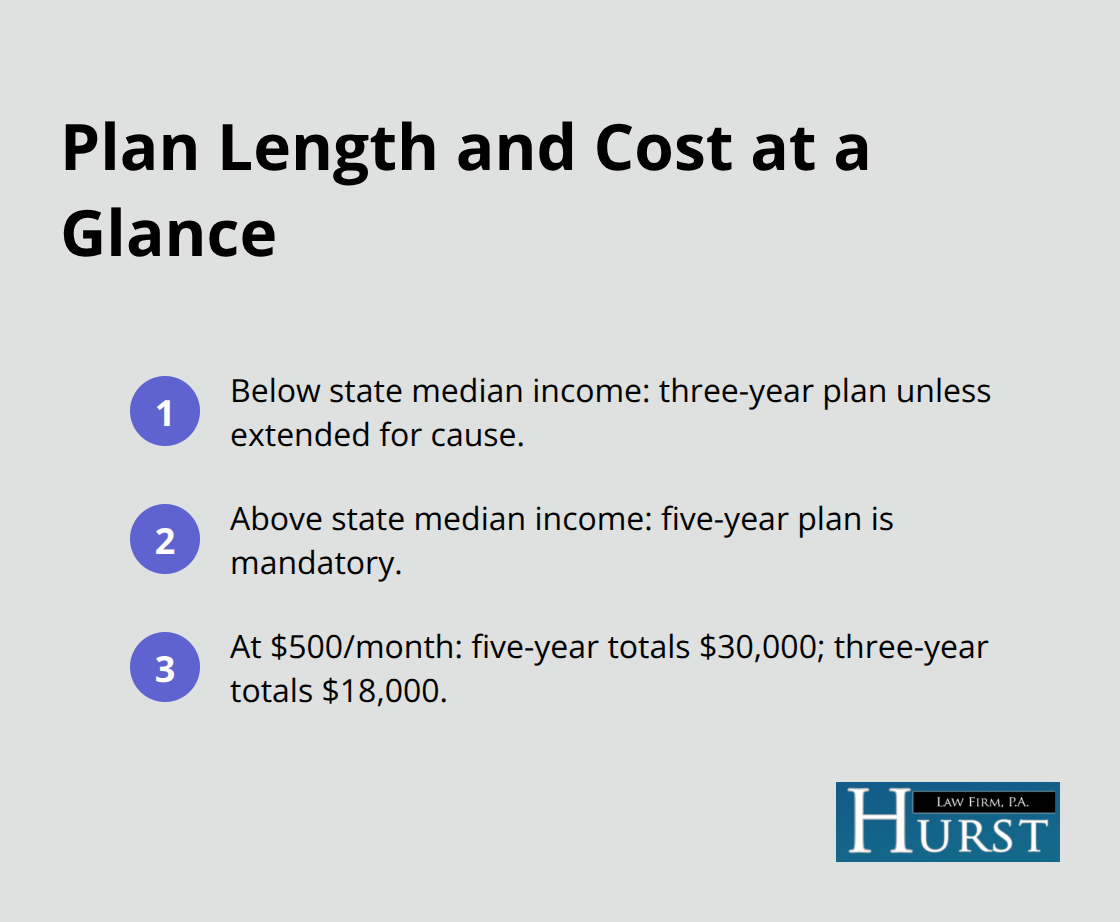

Determine Your Plan Length: Three Years or Five Years

The three-versus-five-year choice hinges entirely on whether your current monthly income falls above or below your state’s median for your family size. Under 11 U.S.C. § 1325(d), if you earn below the median, your plan runs three years unless the court extends it for cause. If you earn above the median, the plan must run five years, period. This is not negotiable, and the difference matters significantly: a five-year plan at five hundred dollars monthly costs thirty thousand dollars total, while a three-year plan at the same payment costs eighteen thousand dollars. Memphis residents filing Chapter 13 in 2025 face a state median of approximately fifty-two thousand dollars annually for a family of four, meaning many above-average earners cannot escape the five-year commitment regardless of their circumstances. Before you file, calculate exactly where you fall against that median because this decision shapes your entire repayment obligation.

Understanding Chapter 13 bankruptcy versus Chapter 7 helps clarify whether a repayment plan aligns with your financial goals.

Apply the Best Interests Test to Your Plan

The court applies the best interests test under 11 U.S.C. § 1325(a)(4), meaning unsecured creditors must receive at least what they would get in Chapter 7 liquidation, so a shorter plan does not automatically mean less payment to creditors if your disposable income supports higher amounts. This requirement protects creditors while holding you accountable to realistic numbers. Your honest income and expense figures satisfy this test and prevent the objections that derail cases before confirmation even happens.

Organize Your Documentation Before Filing

Gather recent pay stubs, tax returns, property valuations, and a detailed list of every creditor before the petition reaches the court. The confirmation hearing typically occurs within forty-five days of filing, and missing documentation at that point delays confirmation and frustrates your fresh start. Incomplete filings trigger objections from the trustee that extend your timeline unnecessarily. Having all numbers verified and all documents organized protects your case from preventable delays.

Final Thoughts

Chapter 13 bankruptcy help requires honest numbers and realistic planning from the moment you decide to file. The difference between a plan that survives five years and one that collapses within months comes down to whether you built your budget on actual income and genuine expenses or on wishful thinking. Creditors and trustees have seen thousands of cases-they recognize inflated income claims and understated living costs immediately.

An attorney who understands Chapter 13 mechanics can spot budget problems during preparation, not after the court rejects your plan. They verify your income calculations against tax returns, identify expenses you might overlook, and position your case for confirmation on the first hearing. This guidance costs far less than rebuilding a failed plan or converting to Chapter 7 after months of wasted payments.

We at Hurst Law Firm, P.A. in Memphis, Tennessee handle Chapter 13 filings with the attention to detail that protects your plan’s viability and moves you toward discharge. Contact Hurst Law Firm, P.A. to discuss your Chapter 13 options and start building a plan designed to succeed.