Chapter 13 bankruptcy offers a structured path to manage debt while keeping your assets. If you’re considering this option in Memphis, understanding how the process works is the first step toward financial stability.

We at Hurst Law Firm, P.A. help clients navigate Chapter 13 help Memphis by breaking down the repayment plan, identifying common pitfalls, and building sustainable payment strategies. This guide walks you through what to expect and how to succeed.

How Chapter 13 Actually Works in Memphis

The Three to Five Year Repayment Structure

Chapter 13 bankruptcy in Memphis follows a court-supervised repayment plan that lasts between three and five years. The length depends on your income relative to Tennessee’s median income for your household size. If your income falls below the state median, your plan runs three years. If it exceeds the median, the plan extends to five years. This isn’t arbitrary-it’s built into the bankruptcy code and affects how much you’ll repay overall.

During this period, you make one monthly payment to a court-appointed trustee, who then distributes those funds to your creditors according to a court-approved plan. The trustee doesn’t handle your money directly from your bank account; you control when and how you pay, though most people set up automatic transfers to avoid missing deadlines.

How Debts Get Organized and Prioritized

Your debts get organized into strict priority classes that the trustee must follow. Priority claims come first-these include recent tax debts, child support, and alimony. Secured debts come next, meaning obligations tied to collateral like your home mortgage or car loan. These must receive enough payment to protect the creditor’s interest in the property. Unsecured debts, such as credit cards and medical bills, receive whatever’s left from your disposable income after living expenses.

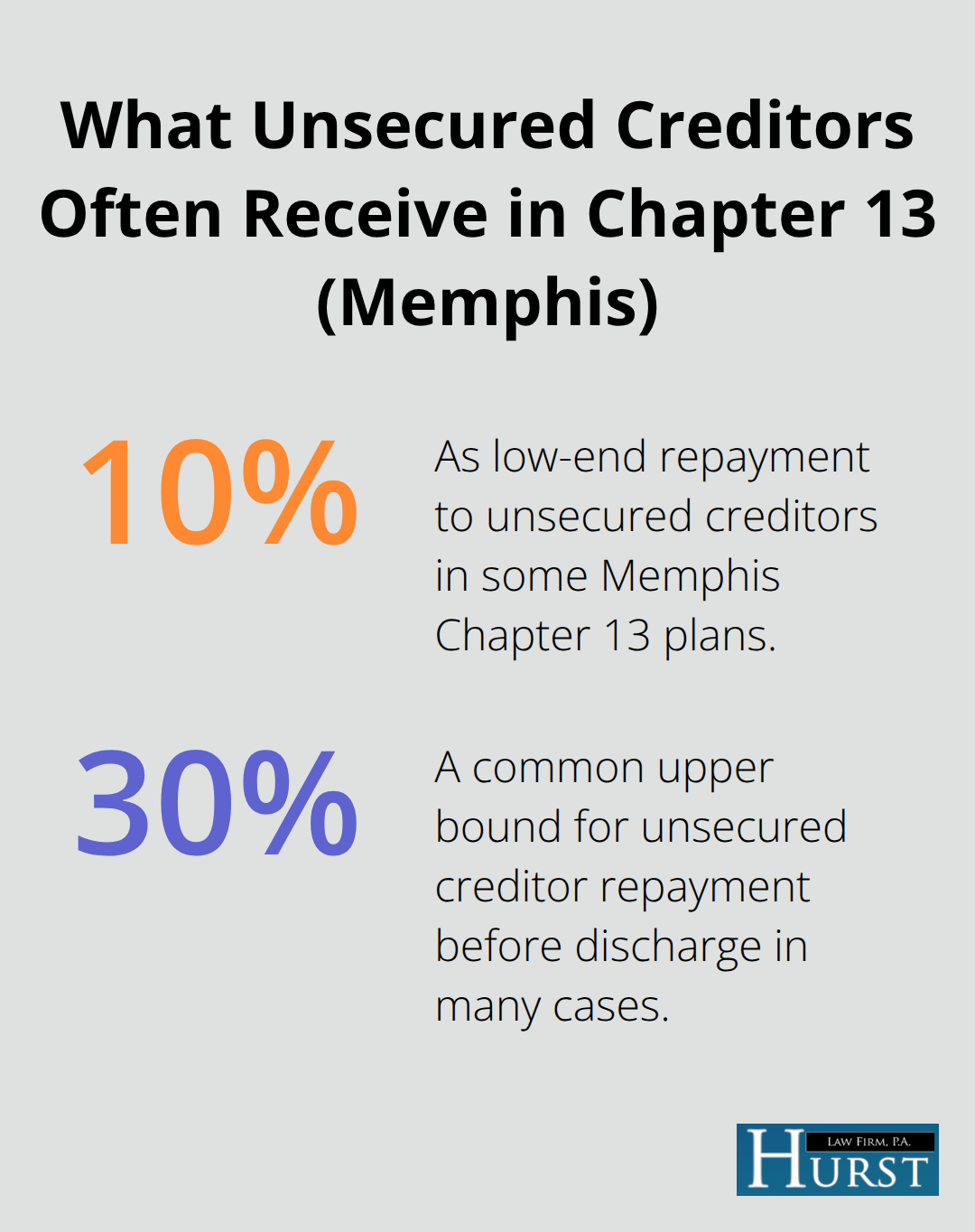

The trustee calculates your disposable income by subtracting reasonable living costs from your gross income using the Tennessee Means Test. This figure determines your monthly plan payment and how much creditors ultimately receive. Many Memphis residents are surprised to learn that unsecured creditors often receive only partial repayment-sometimes as little as 10 to 30 percent of what’s owed-yet the remaining balance gets discharged at plan completion.

Protections That Stay Active Throughout Your Plan

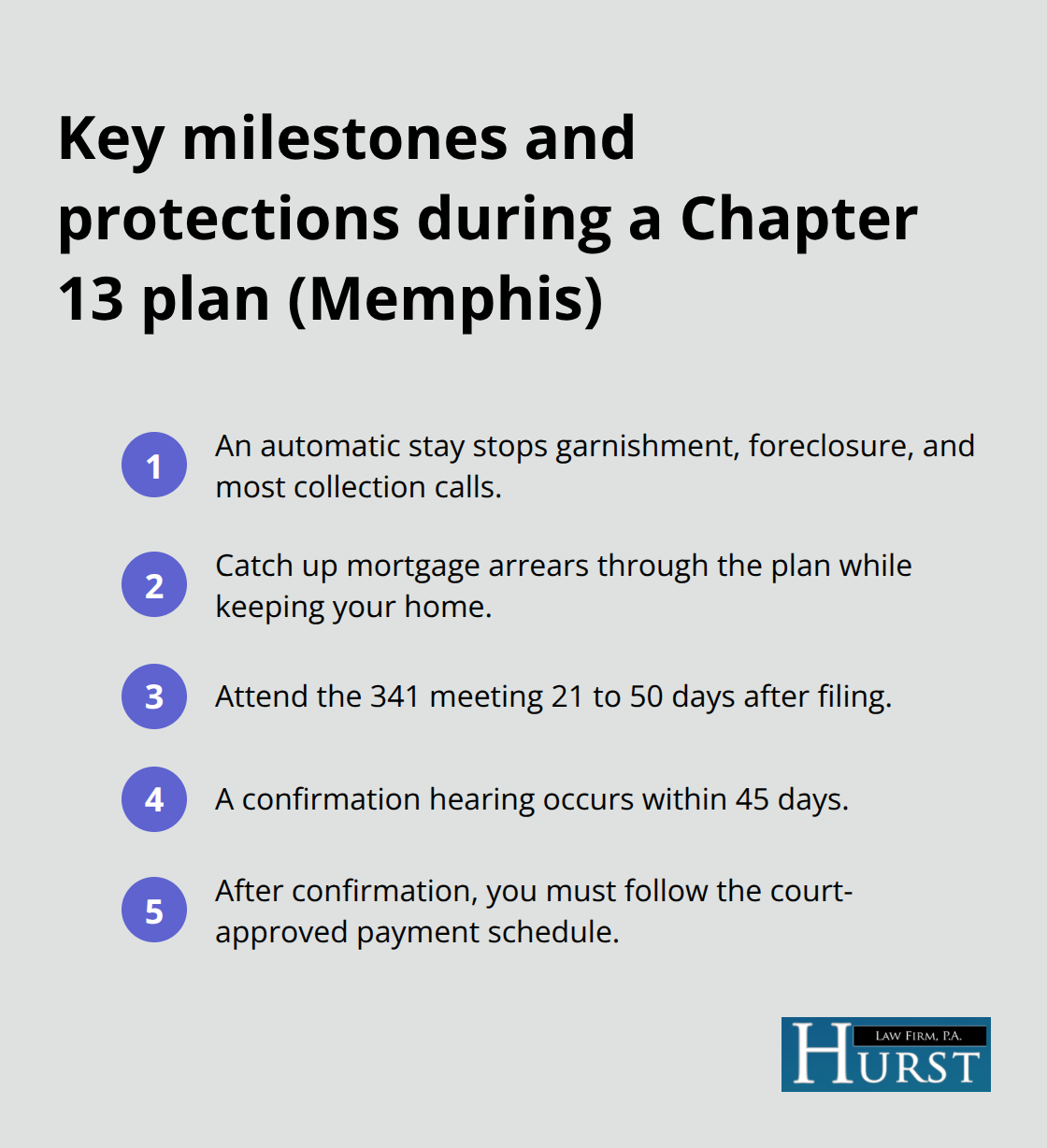

During the three to five year period, several protections remain active. An automatic stay stops wage garnishment, foreclosure proceedings, and most collection calls immediately. If you’re behind on mortgage payments, Chapter 13 lets you catch up those arrears through the plan itself rather than facing immediate foreclosure. This feature makes Chapter 13 particularly valuable for Memphis homeowners in financial crisis.

You must attend a meeting of creditors, typically held 21 to 50 days after filing, where you answer questions under oath about your debts and income. A confirmation hearing follows within 45 days to approve your plan’s feasibility. After confirmation, you’re legally bound to the repayment schedule.

What Happens When You Miss Payments or Your Circumstances Change

Missing payments creates serious consequences-three missed payments in a row can trigger dismissal of your case, which immediately lifts the automatic stay and leaves you vulnerable to foreclosure and garnishment again. Successful completion requires discipline and honest communication with your trustee if circumstances change.

If your income increases, your payment likely increases too. If it decreases, you can request a modification, but only if you report the change promptly. This isn’t a set-it-and-forget-it process; it demands active participation throughout the entire plan period. Understanding these payment obligations and the consequences of noncompliance sets the stage for recognizing the common mistakes that derail many Chapter 13 filers before they reach discharge.

Where Chapter 13 Plans Actually Fall Apart

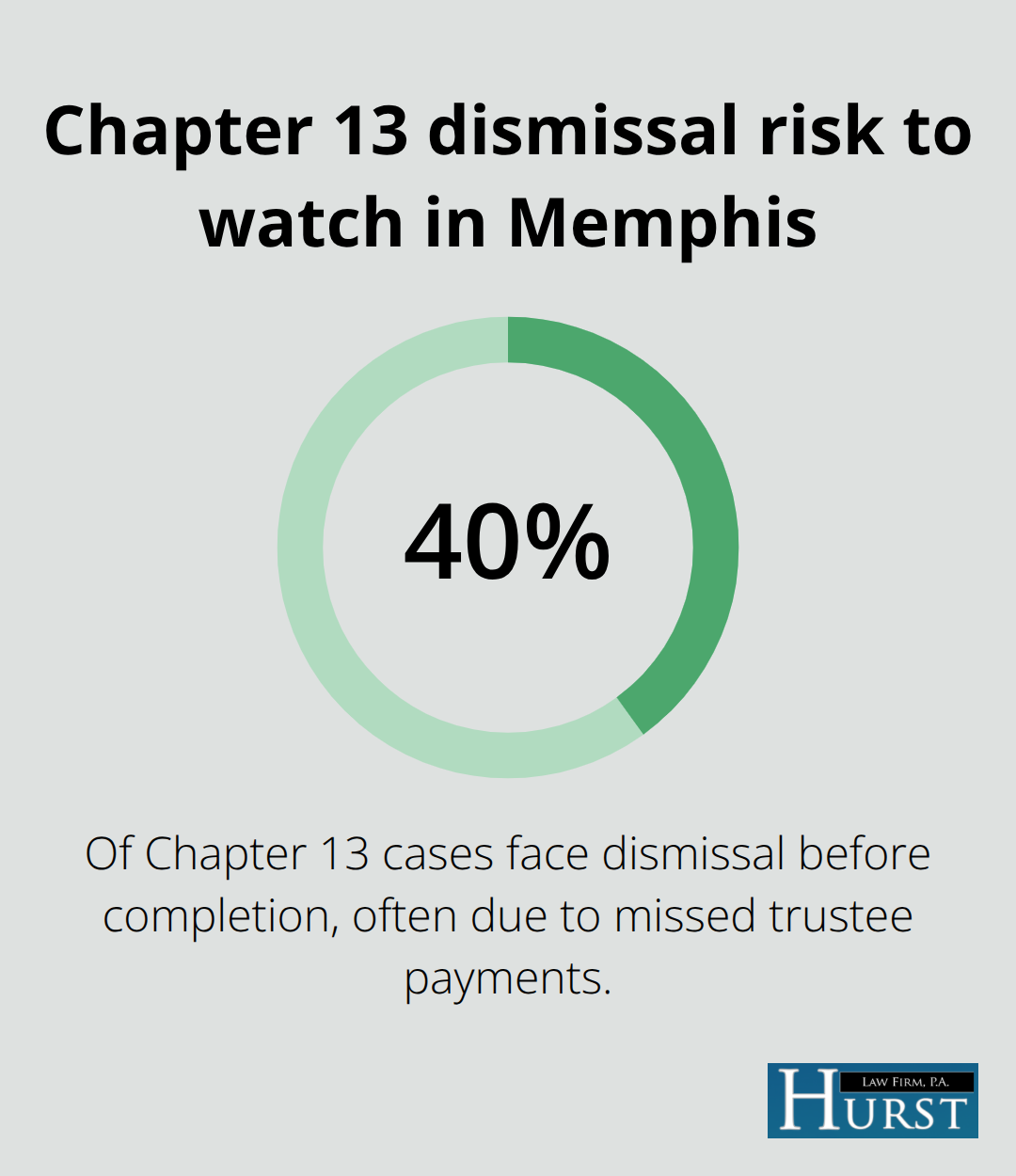

Most Chapter 13 filers underestimate the monthly payment discipline required to reach discharge. The U.S. Courts reported that roughly 40 percent of Chapter 13 cases face dismissal before completion, and the primary reason isn’t rising debt or unexpected emergencies-it’s failure to maintain consistent monthly payments to the trustee.

Memphis residents often enter a plan with optimistic assumptions about their budget, only to discover three months in that their actual living expenses exceed what they reported on the means test. This miscalculation forces a choice: skip a payment or request a modification. Skip one payment and creditors grow impatient. Skip three payments and the trustee files a motion to dismiss, instantly lifting your automatic stay and reopening you to foreclosure, wage garnishment, and collection activity.

The Payment Discipline Problem

The trustee doesn’t care about your excuses; the code requires strict compliance. Before filing, audit your actual monthly spending for the past three months-not what you think you spend, but what bank statements and credit card bills show. Include groceries, utilities, insurance, car maintenance, phone bills, and childcare. Most Memphis filers discover they’ve underestimated food costs by 30 percent or gasoline by 40 percent. If your calculated disposable income leaves no cushion for fluctuation, Chapter 13 becomes a ticking clock rather than a solution.

Misunderstanding Which Debts Actually Discharge

Equally dangerous is misunderstanding which debts survive Chapter 13 discharge. Unsecured debts like credit cards and medical bills get eliminated at the end of your plan-but only if you complete it. Student loans almost never discharge; they remain your obligation even after successful completion unless you qualify for hardship discharge, which courts rarely grant. Recent tax debts within three years of filing don’t discharge either, and the IRS continues collecting even while your plan runs.

Priority Claims That Drain Your Resources

Child support and alimony arrears must be paid in full through your plan before a single dollar goes to credit card companies, which means if your disposable income is tight, creditors receive minimal payment while family obligations drain your resources. Secured debts tied to collateral-your home mortgage, car loan, or furniture financed through a store-get reorganized but not eliminated. You keep the property only if you stay current on payments and the trustee confirms the plan.

The Mortgage Payment Trap

Missing a mortgage payment during Chapter 13 doesn’t just hurt your credit; it triggers foreclosure despite the automatic stay’s protection. Many Memphis homeowners assume their mortgage automatically gets caught up through the plan, only to realize they still owe the current month’s payment directly to the lender. The plan addresses past-due amounts, not ongoing obligations. Understanding this distinction before filing prevents the shock of discovering that your plan pays creditors 15 percent of what they’re owed while you remain obligated to repay priority claims in full. These payment realities shape how successful filers approach their plans from day one, which is why calculating your actual disposable income and building realistic payment systems matters far more than most people realize.

Building a Plan You Can Actually Afford

The gap between what you think you can afford and what you actually can afford determines whether you reach discharge or face dismissal. Most Memphis filers calculate their disposable income once during their initial consultation, then discover six months into the plan that their actual monthly expenses don’t match what they reported on the means test. The Tennessee Means Test uses standardized expense allowances that often underestimate real-world costs. The IRS expense standards for Memphis, for example, set a reasonable grocery allowance for a family of four at around $1,200 monthly, but actual spending frequently runs $1,600 to $1,800 when you account for school lunch costs, special dietary needs, and price inflation since the standards were last updated.

Audit Your Actual Spending Before Filing

Pull three months of bank and credit card statements and categorize every transaction: groceries, utilities, gas, insurance, childcare, medications, and miscellaneous expenses. This real spending history becomes your foundation for calculating whether your proposed plan payment is sustainable. If your calculated disposable income leaves less than $200 monthly cushion after your proposed trustee payment, the plan is fragile and likely to fail. Most Memphis filers discover they’ve underestimated food costs by 30 percent or gasoline by 40 percent when they review actual statements rather than estimates.

Work With Your Trustee From Day One

The trustee isn’t your adversary, despite how the process feels. The trustee’s job is to administer a feasible plan, and a plan that fails harms everyone. When you file, attend the creditors’ meeting prepared to discuss your actual budget, not your theoretical budget. Bring documentation: recent pay stubs, mortgage statements, insurance bills, and a detailed expense spreadsheet. Trustees have reviewed thousands of Memphis cases and spot inflated living expense claims instantly.

If your proposed plan payment seems aggressive based on your income, propose a lower payment that you know you can maintain consistently. A confirmed plan with a $400 monthly payment that you complete beats a $600 payment that triggers dismissal after eighteen months. Some trustees in Memphis allow plan modifications before confirmation if your budget analysis reveals you underestimated expenses. This window typically closes once the judge confirms your plan, so use it strategically. If you have variable income from seasonal work or commission-based employment, propose a payment based on your lowest recent year’s earnings rather than an optimistic average. The trustee will likely accept a conservative estimate because it demonstrates realistic planning.

Set Up Payment Systems That Work

Missing even one payment creates stress and jeopardizes your discharge. Set up automatic payroll deduction with your employer if possible, which removes the temptation to skip a payment and ensures the trustee receives funds on schedule. If automatic deduction isn’t available through your employer, establish an automatic bank transfer scheduled three days before your payment due date. This creates a buffer if the trustee’s banking processes run slower than expected.

Many Memphis filers use a separate savings account dedicated solely to trustee payments, depositing their share of each paycheck immediately rather than waiting until the payment is due. This approach prevents accidentally spending money earmarked for the plan. Track your payment history monthly by reviewing the trustee’s website or requesting statements. The U.S. Courts system allows you to verify payment records online through the bankruptcy court’s PACER system, and discrepancies are far easier to resolve when caught early rather than discovered during your confirmation hearing or discharge process (early detection prevents costly delays and confusion later).

Handle Changes to Your Income or Expenses

If you anticipate a payment difficulty due to a medical emergency, job loss, or major home repair, contact an attorney immediately rather than skipping a payment. Plan modifications exist specifically for these situations, and requesting one proactively demonstrates good faith to the trustee and court. If your income increases, your payment likely increases too. If it decreases, you can request a modification, but only if you report the change promptly. This isn’t a set-it-and-forget-it process; it demands active participation throughout the entire plan period.

Final Thoughts

Chapter 13 success in Memphis depends on three foundational elements: honest budgeting, consistent payment discipline, and proactive communication with your trustee. The filers who reach discharge aren’t those with perfect financial situations-they’re the ones who audit their actual spending before filing, propose realistic payment amounts, and set up automatic systems to prevent missed payments. Understanding that roughly 40 percent of Chapter 13 cases face dismissal before completion shows you exactly what to avoid.

The mistakes outlined in this guide-underestimating monthly expenses, misunderstanding which debts discharge, and falling behind on payments-are entirely preventable with proper planning and accountability. We at Hurst Law Firm, P.A. have guided Memphis residents through Chapter 13 since 1997, helping individuals and families navigate the repayment process with realistic expectations and sustainable plans. Attorney Herbert Hurst and our team focus on breaking down the complexity of bankruptcy law into actionable steps tailored to your specific financial situation.

If you’re considering Chapter 13 help in Memphis, contact Hurst Law Firm, P.A. to discuss whether Chapter 13 fits your situation or whether another path better serves your financial recovery. The sooner you take action, the sooner you stop the cycle of collection calls and wage garnishment and begin rebuilding toward stability.