Overwhelming debt can feel suffocating, but Chapter 7 bankruptcy offers a legitimate way out. If you’re struggling with credit card bills, medical expenses, or other unsecured debts, Chapter 7 bankruptcy in Memphis could give you the fresh start you need.

We at Hurst Law Firm, P.A. help Memphis residents navigate this process from start to finish. This guide walks you through what happens, who qualifies, and how bankruptcy affects your financial future.

What Happens When You File Chapter 7

The Automatic Stay Stops Collection Actions Immediately

Filing Chapter 7 triggers an automatic stay that stops creditor calls, wage garnishments, lawsuits, and collection actions the moment your petition reaches the court. This protection is real and enforceable-creditors who violate the stay face penalties. The automatic stay gives you breathing room to work through the bankruptcy process without constant harassment or threats of asset seizure.

A Trustee Reviews Your Assets and Property

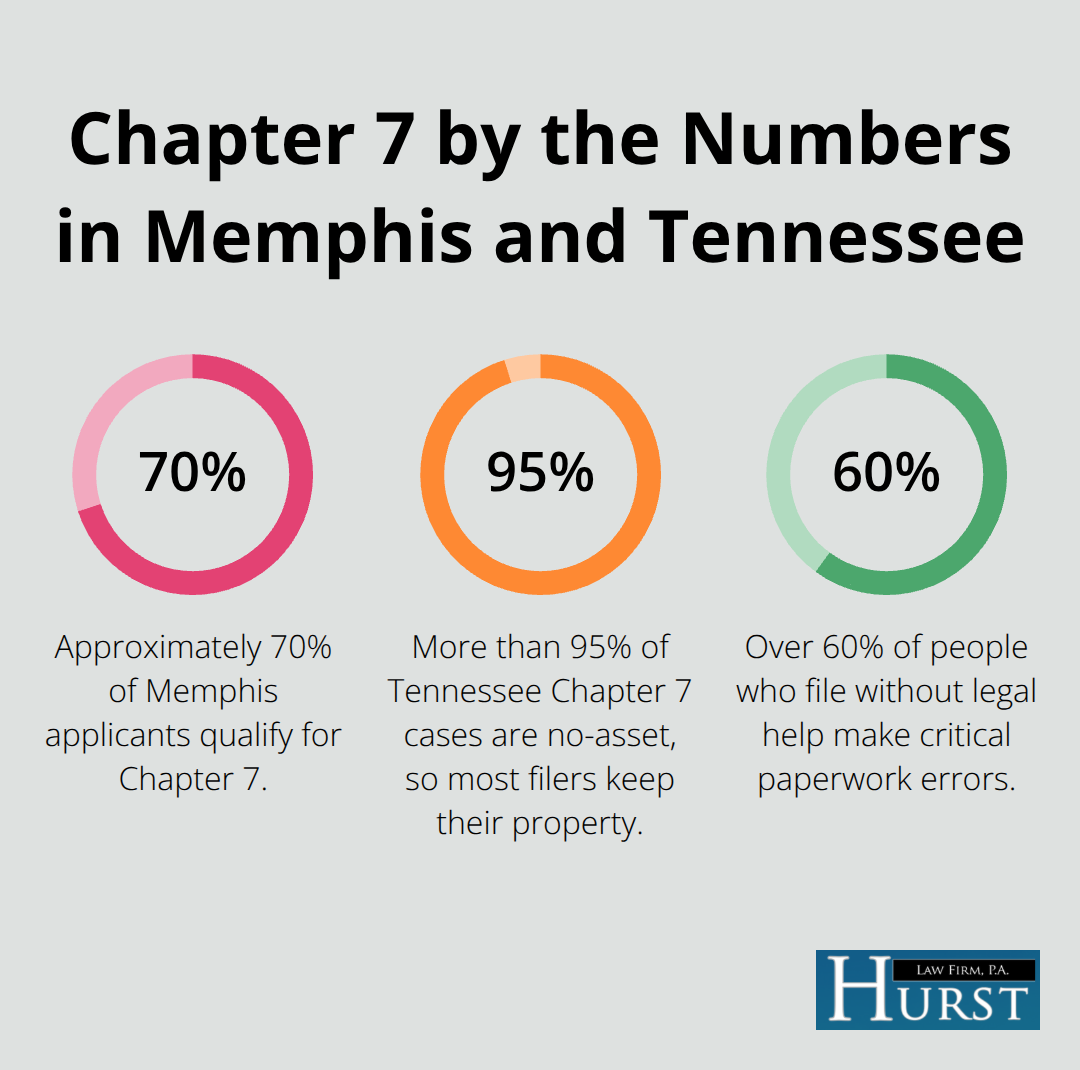

Within days of filing, a bankruptcy trustee is assigned to your case. This trustee’s job is straightforward: review your financial documents, identify any non-exempt assets, and liquidate them if necessary to repay creditors. The good news for Memphis residents is that Tennessee exemption laws are generous. According to the American Bankruptcy Institute, more than 95% of Chapter 7 cases in Tennessee are no-asset cases, meaning most filers keep their property.

You can typically protect up to $5,000 of equity in your primary residence, one vehicle, basic household items, and work tools. The trustee will only sell assets that exceed these exemptions, so understanding what you can keep prevents surprises.

The Timeline Moves Quickly From Filing to Discharge

The timeline from filing to discharge typically runs three to six months. About 30 to 45 days after you file, you’ll attend the 341 Meeting of Creditors-despite its name, creditors rarely show up. The trustee asks questions under oath about your finances and assets; the meeting usually lasts five to ten minutes. Attendance is mandatory; missing it results in automatic dismissal.

After the meeting, you must complete a two-hour debtor education course (costs around $25) before the court grants your discharge. The filing fee is $338, though fee waivers may be available if you qualify.

Accuracy in Your Petition Determines Your Success

Throughout this process, accuracy in your petition matters significantly. The American Bankruptcy Institute notes that over 60% of people who file without legal help make critical errors on their paperwork-mistakes on property schedules or exemptions can trigger asset seizure or dismissal. An attorney helps you avoid these costly errors and moves your case smoothly toward discharge. Understanding your eligibility and what debts you can actually eliminate requires careful analysis of your specific financial situation.

Who Qualifies for Chapter 7 in Memphis TN

The Means Test Determines Your Eligibility

The means test is the first hurdle you face when filing Chapter 7 in Memphis. According to United States Courts, a single filer in 2025 must earn under $39,759 monthly to qualify, while a family of four needs income below $93,767. These thresholds use Shelby County median income data and are updated regularly. However, earning above these limits does not automatically disqualify you.

The means test allows deductions for essential expenses like housing, transportation, utilities, and childcare that the IRS establishes annually. If your gross income exceeds the threshold but your income minus allowable deductions falls below it, you still qualify for Chapter 7. This is where many Memphis residents find relief-seasonal workers, commissioned salespeople, and small-business owners with fluctuating income can often pass the means test once legitimate expenses are calculated.

Income Thresholds and Deductions Work Together

Approximately 70% of bankruptcy applicants in Memphis qualify for Chapter 7 based on these thresholds, according to data from United States Courts. The key is accurate reporting of your actual household income and legitimate deductions; underreporting or hiding income sources creates serious problems later.

Deductions for essentials (housing, food, transportation, medical care) can lower your disposable income significantly and push you below the threshold even if your gross income appears too high.

Dischargeable Debts Vanish After Bankruptcy

Chapter 7 discharges most unsecured debts, meaning the court eliminates them entirely. Credit card balances, medical bills, personal loans, and payday loans vanish after discharge. This is the core benefit of Chapter 7-wiping out obligations you cannot afford to repay.

Debts That Survive Chapter 7 Discharge

Certain debts survive the discharge and remain your legal responsibility. Student loans almost never disappear in Chapter 7 unless you prove undue hardship, a high legal bar that few meet. Child support and alimony obligations cannot be eliminated. Most tax debts also survive, though some older tax liabilities may qualify for discharge depending on when they were assessed. Court fines, restitution orders, and certain HOA fees also typically remain.

Understanding what stays and what goes prevents disappointment after your discharge is granted. Your specific debt situation determines which obligations discharge and which ones you will manage after bankruptcy. This analysis shapes your overall financial recovery strategy moving forward.

How Chapter 7 Bankruptcy Affects Your Financial Future

Your Credit Score Takes a Hit, Then Recovers

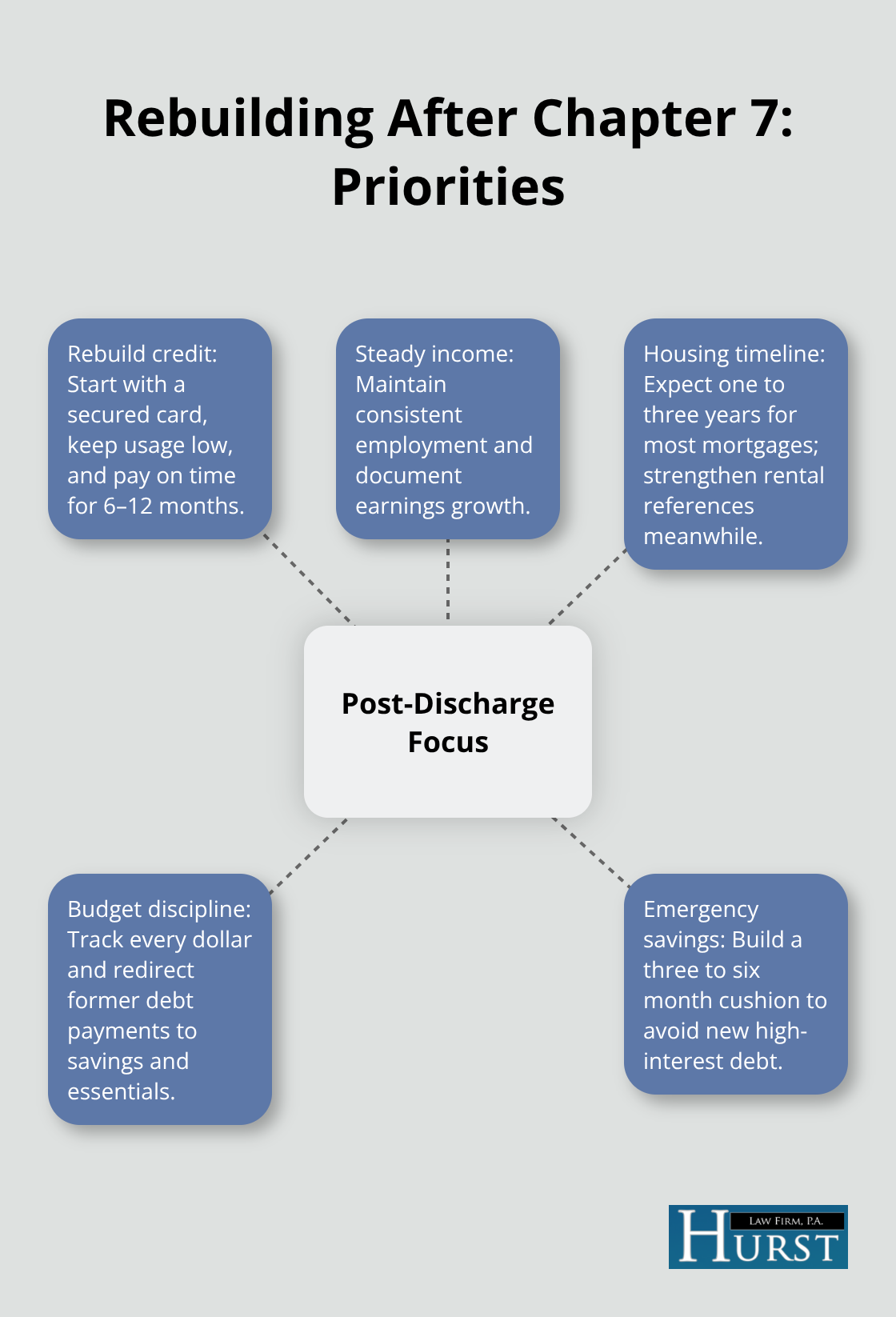

Chapter 7 bankruptcy stays on your credit report for approximately ten years from your filing date. However, this does not mean your credit remains destroyed for a decade. Most people who file Chapter 7 start rebuilding their credit within twelve to twenty-four months after discharge, and many see meaningful score improvements within three to five years.

Your credit score will drop significantly when you file-often 130 to 200 points depending on your starting score-because the filing becomes a public record. The impact softens over time as the bankruptcy ages and you establish new positive credit history. Secured credit cards designed for rebuilding credit typically require a $300 to $500 deposit and charge reasonable interest rates around 18 to 24 percent annually. Use one responsibly for six to twelve months, making small purchases and paying them off monthly, to demonstrate that you can manage credit again. After twelve months of perfect payments, many card issuers convert your account to an unsecured card with better terms.

Employment Remains Available Despite Bankruptcy

Some employers and landlords view bankruptcy unfavorably, but federal law prohibits discrimination based solely on bankruptcy filing. Government employers cannot deny you employment based on bankruptcy. Private employers have more flexibility, though many prioritize recent job performance over historical financial problems.

The bankruptcy itself does not prevent you from working or earning income. Your focus after discharge should shift toward demonstrating stable employment and income growth over the next one to two years. This stability matters far more to most employers than a bankruptcy from years past.

Housing Requires Time and Patience

Housing presents more complexity than employment. Most traditional mortgage lenders require a two to three year waiting period after Chapter 7 discharge before they will consider your application, though some specialized lenders operate in the one to two year window. Rental housing is harder to predict because landlords conduct background checks and may see the bankruptcy as a red flag.

Many landlords focus primarily on recent income stability and rental history rather than a bankruptcy from years past. Building strong rental references and demonstrating stable employment for twelve to twenty-four months after discharge strengthens your housing applications significantly. Start this process early-do not wait until you need housing to establish your track record.

Redirect Your Money Toward Real Financial Stability

The real opportunity after Chapter 7 discharge is redirecting the money you previously sent to creditors toward building genuine financial stability. If you paid $800 monthly toward credit cards and medical debt before filing, that $800 becomes available for emergency savings, retirement contributions, or paying down remaining obligations like student loans.

Create a written budget immediately after discharge and track every dollar of income and expenses. This prevents the spending patterns that created your original debt problems.

Many Memphis residents who file Chapter 7 report that the fresh start forces them to confront their actual spending habits and make intentional financial choices rather than drifting into debt reactively. The discharge gives you a second chance-how you use it determines your long-term financial health.

Final Thoughts

Chapter 7 bankruptcy in Memphis offers a legitimate path to eliminate unsecured debt and rebuild your financial life. The process moves quickly-typically three to six months from filing to discharge-and the automatic stay provides immediate relief from creditor harassment and collection actions. For most Memphis residents, Tennessee’s generous exemption laws mean you keep your home equity, vehicle, and essential property while wiping out credit cards, medical bills, and personal loans that have become unmanageable.

Your credit score will drop when you file, but most people rebuild meaningfully within two to three years by using secured credit cards responsibly and maintaining stable employment. Housing and employment remain accessible with time and demonstrated financial stability. The real opportunity lies in redirecting the money you previously sent to creditors toward genuine savings, retirement contributions, and intentional financial planning.

The bankruptcy petition requires near-perfect accuracy, and over 60% of people who file without legal help make critical errors that delay discharge or trigger asset seizure. We at Hurst Law Firm, P.A. handle the documentation, court procedures, and strategy so you avoid costly mistakes. Contact us at 901.725.1000 or visit our office at 2287 Union Avenue, Memphis, TN 38104 for a free consultation.