Filing for Chapter 7 bankruptcy in Memphis TN raises one immediate question: how long will this take? The Chapter Seven discharge timeline varies significantly based on your specific situation, and understanding what to expect helps you plan ahead.

At Hurst Law Firm, P.A., we’ve guided countless Memphis residents through this process. This guide breaks down each stage, identifies common delays, and shows you exactly what happens from filing day to final discharge.

How Long Your Chapter 7 Case Actually Takes

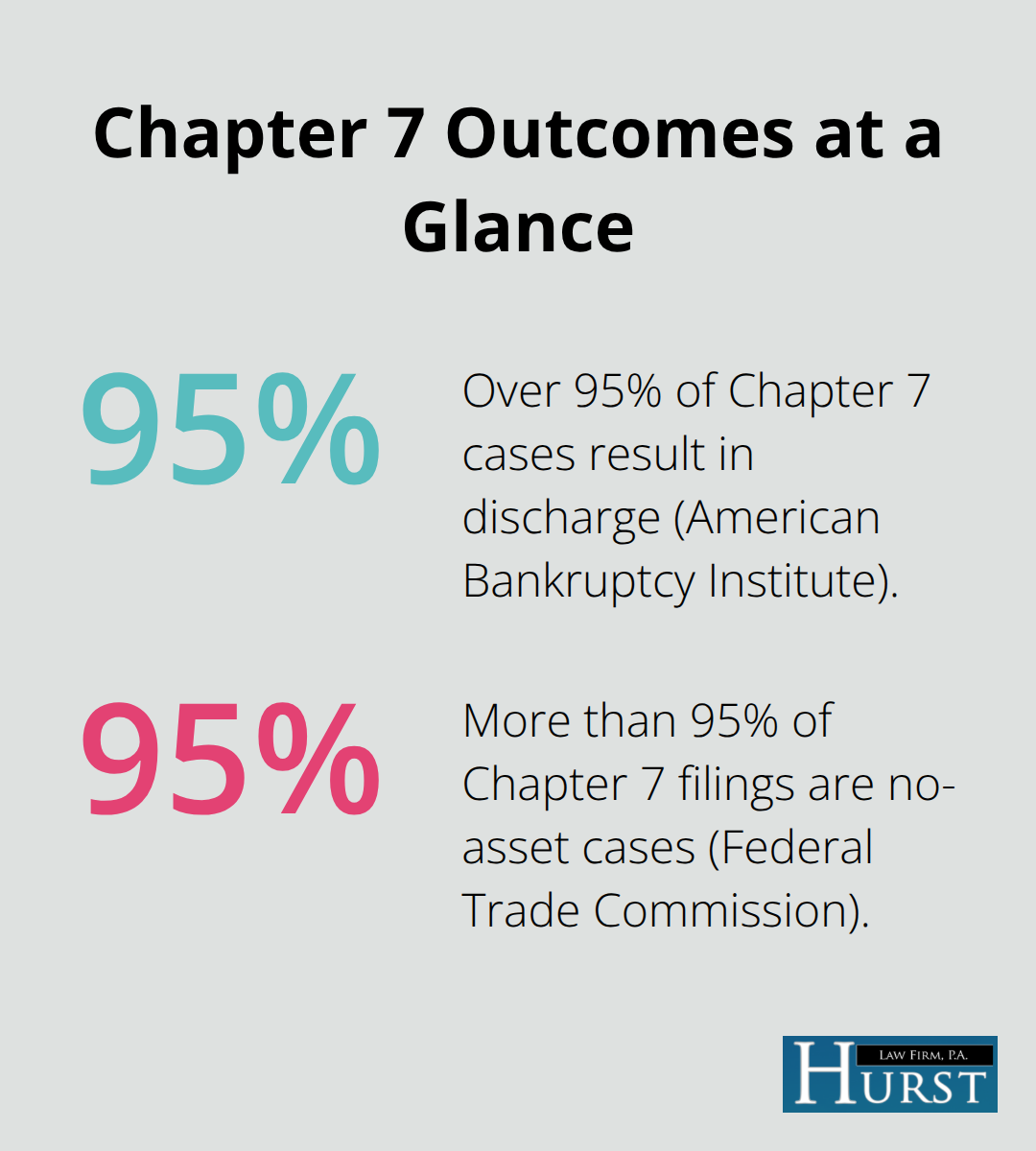

Most Chapter 7 bankruptcy cases in Memphis move faster than people expect. From the moment you file with the U.S. Bankruptcy Court for the Western District of Tennessee until you receive your discharge order, the typical timeline runs three to six months. This speed matters because the automatic stay takes effect immediately and stops creditor calls and wage garnishment, then moves you toward a genuine fresh start within half a year. The American Bankruptcy Institute reports that over 95 percent of Chapter 7 cases result in discharge, and the vast majority of those cases are no-asset situations where the trustee finds little or no property to liquidate. If you fall into this category-which describes most Memphis filers-your case will move toward the faster end of that range. The Federal Trade Commission data shows that more than 95 percent of Chapter 7 filings nationwide involve no significant assets to sell, meaning your timeline depends far more on administrative compliance than on asset liquidation battles.

What Happens in the First 30 to 45 Days

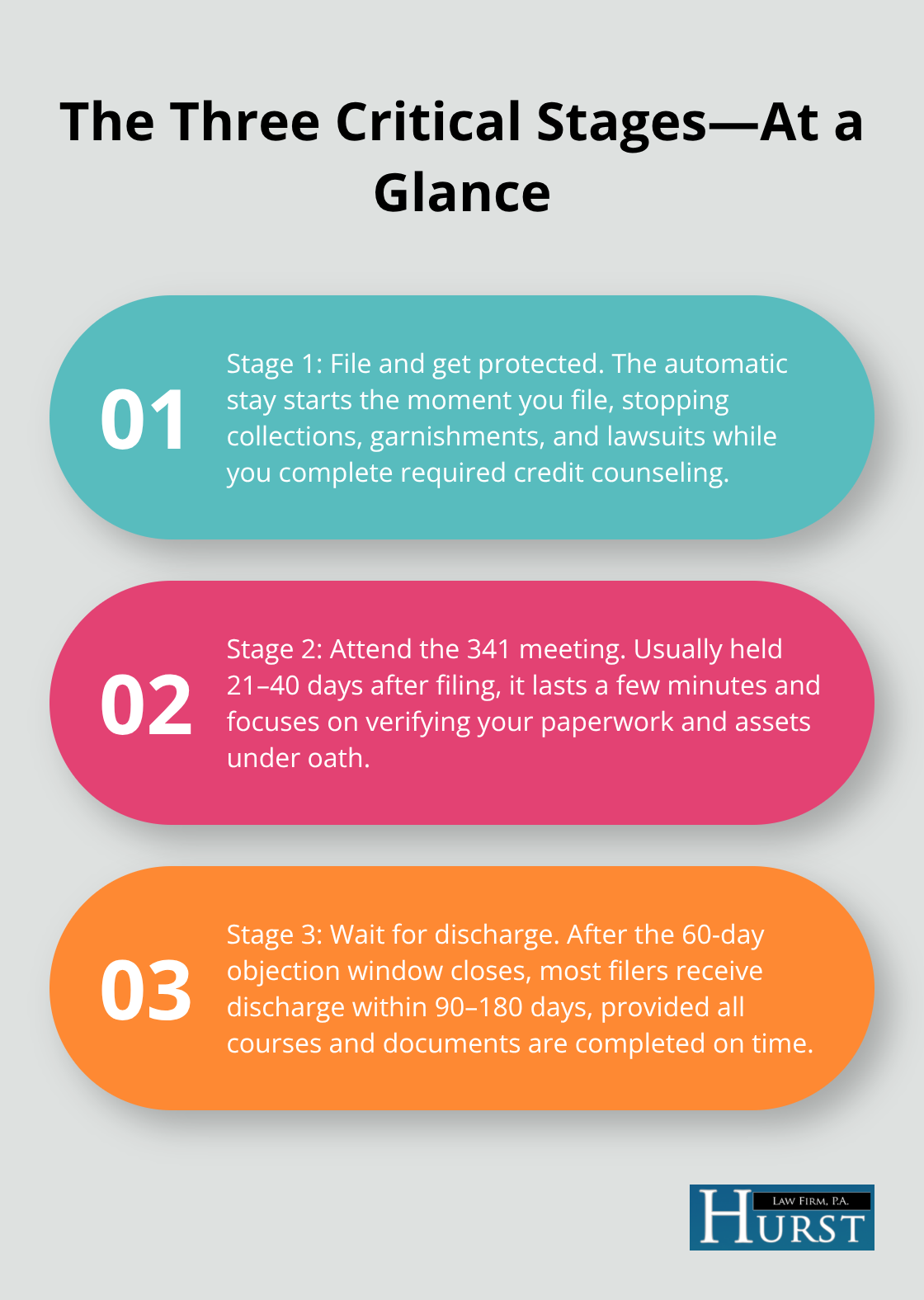

Your case begins the moment you file your petition, and the automatic stay takes effect immediately to stop collection actions. Within 21 to 40 days, you attend the 341 meeting of creditors before the court-appointed trustee, where you answer questions under oath about your debts and assets. This meeting typically lasts only 5 to 10 minutes, and creditors rarely show up to challenge anything. The trustee uses this time to verify that your paperwork matches your statements and to determine whether non-exempt assets exist. Before this meeting happens, you must complete a court-approved credit counseling course, which takes roughly two hours and costs little. The trustee then has 60 days after the 341 meeting to object to your discharge or pursue asset liquidation, but objections are uncommon when you file truthfully and complete required counseling.

The Path to Your Discharge Order

After the 60-day objection window closes with no disputes filed, your discharge order arrives within another 30 to 60 days. Most Memphis filers receive their discharge between 90 and 180 days after filing, putting them well within the three to six month range. The Western District of Tennessee processes these cases consistently, though individual judges’ schedules can shift dates by a few weeks. Delays occur when you miss deadlines, file incomplete paperwork, or fail to complete the predischarge debtor education course before the trustee’s deadline. The fee to file is $338, and you can request a waiver if you cannot afford it. Once your discharge order arrives, debts like credit card balances, medical bills, personal loans, and utility bills are permanently eliminated, though student loans, child support, and recent tax debts survive the discharge and remain your responsibility.

What Comes Next After Discharge

Your discharge order marks the legal end of your Chapter 7 case, but your financial recovery continues beyond that point. The discharge eliminates most unsecured debts permanently, yet you still face the work of rebuilding your credit and establishing new financial habits. Understanding what happens during each stage of your case-from the initial filing through the trustee’s review and into the final discharge phase-helps you prepare for what comes after the court closes your file.

The Three Critical Stages of Your Chapter 7 Case

Filing your Chapter 7 petition triggers immediate legal protection, but understanding what happens at each stage helps you stay on track and avoid costly mistakes. The moment you file with the U.S. Bankruptcy Court for the Western District of Tennessee, the automatic stay takes effect and stops all collection actions, wage garnishment, and creditor lawsuits instantly. This protection is real and enforceable-creditors who violate the stay face court sanctions. Before your 341 meeting arrives in 21 to 40 days, you must complete a court-approved credit counseling course, which takes about two hours and costs between $50 and $200. Gather your documents now: recent pay stubs, tax returns for the last two years, bank statements, a list of all debts with creditor names and account numbers, and documentation of any assets you own. The trustee will compare your petition against these documents, so accuracy matters far more than perfection.

If your paperwork contains errors or contradictions, the trustee will flag them at the 341 meeting, potentially delaying your discharge by weeks or months. The filing fee is $338, though you can request a fee waiver if you cannot afford it by filing Form 103B with your petition.

What Happens at Your 341 Meeting

Your 341 meeting is less intimidating than its name suggests. The trustee sits across from you, asks standard questions about your debts and assets under oath, and verifies that you reported everything accurately. Most meetings last 5 to 10 minutes, creditors almost never attend, and the trustee’s goal is administrative verification, not confrontation. After this meeting, the trustee has 60 days to object to your discharge or pursue asset liquidation. According to the American Bankruptcy Institute, over 95 percent of Chapter 7 cases result in discharge, and the Federal Trade Commission reports that more than 95 percent of filings are no-asset cases where nothing gets liquidated.

The Path From Meeting to Discharge

If your case is no-asset, you simply wait for your discharge order, which typically arrives 90 to 180 days after filing. Once discharged, debts like credit card balances, medical bills, personal loans, and utility bills vanish permanently, though student loans, child support, and recent tax debts survive the discharge. The discharge order itself is permanent and cannot be reversed, even if your financial situation changes later. After discharge, you cannot file another Chapter 7 for eight years, but you regain your legal right to borrow, build credit, and move forward without the weight of discharged debts. Understanding these timelines and requirements positions you to navigate what comes next-the critical decisions about rebuilding your financial life and protecting your assets moving forward.

What Actually Delays Your Chapter 7 Case

The three to six month timeline assumes you stay compliant with every deadline and requirement. Reality often differs. Missing even one deadline or submitting incomplete paperwork can push your discharge back by 30 to 90 days, turning a four month case into a seven month ordeal.

The Predischarge Education Course Deadline

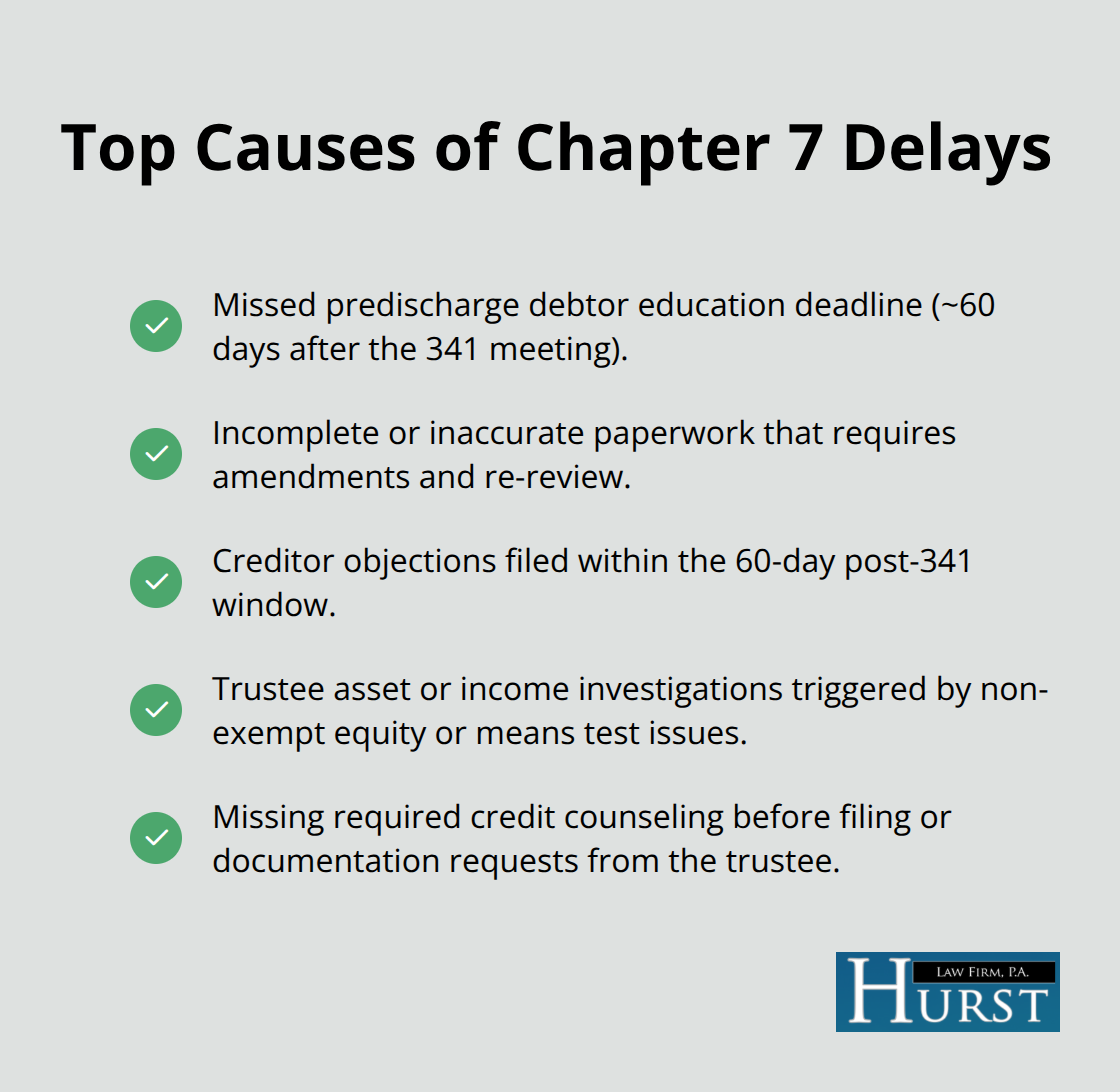

The most common culprit is failing to complete the predischarge debtor education course before the trustee’s deadline, which typically falls 60 days after your 341 meeting. This course takes about two hours, costs $50 to $200, and must be completed through a court-approved provider before the trustee can issue your discharge. Many filers assume they can complete it whenever they want, then scramble when the deadline approaches. If you miss it, the trustee cannot issue your discharge order until you finish, and you remain liable for your debts during that delay.

Paperwork Errors and Inaccuracies

Incomplete or inaccurate paperwork creates similar problems. If your petition lists debts incorrectly, omits assets, or shows conflicting information between your schedules and statements, the trustee will raise these issues at your 341 meeting or shortly after. You then face a choice: file amended paperwork and wait for the trustee to review it again, or explain the discrepancy in writing. Either path adds weeks to your timeline. Accuracy matters far more than perfection, but inaccuracy costs you time.

Creditor Objections and Trustee Investigations

Creditor objections and trustee investigations, while uncommon, create substantial delays when they occur. Over 95 percent of Chapter 7 cases result in discharge, meaning objections are rare, but they happen often enough to matter if you are the one filing. Creditors have 60 days after your 341 meeting to object to the discharge, though most do not bother unless they suspect fraud or see significant non-exempt assets. If a creditor objects, your case enters a dispute phase where you may need to respond in writing or attend another hearing, pushing your discharge back by 60 to 120 days.

Asset and Income Investigations

Trustee investigations into your assets or income also extend timelines significantly. If the trustee suspects you have non-exempt property worth liquidating, they will investigate further, potentially hiring appraisers or requesting additional documents from you. If you own a home with substantial equity above the Tennessee homestead exemption of $5,000 ($7,500 for married couples), the trustee may pursue that equity aggressively, converting your case into an asset case that takes longer to resolve. High income cases, where your income exceeds the Tennessee means test threshold, also trigger deeper trustee scrutiny and longer timelines because the trustee must verify that your disposable income calculations are correct. These investigations rarely result in your discharge being denied, but they absolutely delay it. Submit complete, accurate paperwork from day one, meet every deadline without exception, and complete all required courses on schedule to avoid these delays.

Final Thoughts

Your Chapter 7 discharge timeline in Memphis typically spans three to six months from filing to final discharge, but staying compliant with deadlines and requirements keeps you at the faster end of that range. Accuracy and timeliness matter far more than perfection-submit complete paperwork, finish your credit counseling course before your 341 meeting, and complete your predischarge debtor education course before the trustee’s deadline. These actions alone prevent most delays that extend cases unnecessarily.

After your discharge arrives, your financial recovery begins in earnest. The discharge eliminates credit card balances, medical bills, personal loans, and utility bills permanently, though student loans, child support, and recent tax debts survive and remain your responsibility. Your credit score will recover within 12 to 18 months if you maintain good financial habits-open a secured credit card, make every payment on time, keep your credit utilization low, and monitor your credit report for errors.

We at Hurst Law Firm, P.A. have guided Memphis residents through Chapter 7 bankruptcy since 1997, and we understand the specific challenges you face in the Western District of Tennessee. If you want to understand your Chapter 7 discharge timeline better or discuss whether Chapter 7 fits your situation, contact us for a free consultation at 901-730-4958 or visit our Memphis office at 44 North Second Street, Suite 403.