Wage garnishment can drain your paycheck before you even see it. If creditors are taking money directly from your income, you’re not alone-thousands of workers face this reality every month.

A garnishment dispute requires immediate attention, and that’s where we at Hurst Law Firm, P.A. step in. Bankruptcy offers a powerful legal tool to stop wage garnishment and give you breathing room to rebuild.

How Wage Garnishment Works in Tennessee

The Court Judgment Requirement

Wage garnishment starts when a creditor wins a court judgment against you. Tennessee law allows creditors to withhold a portion of your paycheck directly, but the amount is strictly limited. The maximum garnishment is the lesser of 25% of your weekly disposable income or the amount by which your weekly earnings exceed 30 times the federal minimum wage of $7.25 per hour. This means the first $217.50 of your weekly disposable income stays protected, plus an additional $2.50 per week for each child under 16 living in Tennessee.

If you earn $500 weekly in disposable income, creditors can only take approximately $70.75, not the full 25% they might demand. Your employer receives the garnishment order from the court and must withhold the calculated amount, then send it to the court at least every 30 days. The court distributes those funds to your creditor along with any accrued interest and fees. This process repeats for six months, and creditors can request renewal orders indefinitely until the debt is paid.

Debts That Skip the Lawsuit

Not all debts require a court judgment first. The IRS and Tennessee Department of Revenue can garnish wages administratively without suing you, and federal student loans can garnish up to 15% of your disposable earnings without court involvement. If you ignore a lawsuit and fail to respond within 30 days, the creditor obtains a default judgment, making garnishment virtually automatic.

The Real Financial Toll

The impact on your financial stability depends on your income level and existing expenses. Many workers in Memphis find that even the capped garnishment creates genuine hardship, leaving insufficient funds for rent, utilities, and groceries. If your disposable income falls below $942.50 monthly, no garnishment should apply at all, but proving this requires documentation and often legal action.

The garnishment process itself can feel invasive because your employer learns of your financial problems, and the withholding continues relentlessly unless you take action. A dispute filed within 10 days of receiving the garnishment notice can pause the withholding while you prepare your case, but this approach works only if you can document that the garnishment exceeds what Tennessee law allows. For many workers facing multiple garnishments or insufficient income to cover basic needs, a more permanent solution becomes necessary-one that bankruptcy can provide.

When Garnishment Becomes Unbearable

The Income Reality Check

Wage garnishment hits differently depending on your income level and monthly obligations. If you earn $2,000 monthly in disposable income, losing 25% means $500 vanishes before rent is due. But if you earn $1,200 monthly, that same calculation removes $300, leaving you $900 to cover housing, food, utilities, transportation, and insurance. The numbers reveal the hard truth: garnishment does not affect all workers equally, and for lower-income earners in Memphis, even the legal cap creates genuine financial collapse.

You need legal help immediately if your remaining income after garnishment falls below your basic living expenses. Calculate this honestly: add up rent or mortgage, utilities, groceries, transportation costs, insurance, and childcare. If the total exceeds what remains after garnishment, you cannot sustain that situation indefinitely.

Administrative Garnishments and Stacking Debts

The IRS allows creditors to take money without court orders, and federal student loans can garnish 15% of your disposable earnings administratively. When multiple creditors obtain garnishment orders, the withholdings stack up, and Tennessee law caps total garnishment at 25% of disposable income across all creditors combined-but this protection only helps if you actively monitor what’s being taken.

Many workers discover too late that they should have acted within those critical first 10 days after receiving the garnishment notice. If you miss that window, disputing the amount becomes harder, and the money keeps flowing out of your account every pay period.

When Garnishment Signals Deeper Financial Collapse

The real hardship indicator is not the garnishment amount itself but whether you can pay for food, keep the lights on, and avoid late fees on other bills simultaneously. Memphis residents facing garnishment often have other debts piling up (credit cards, medical bills, or payday loans) that the garnishment does nothing to address. When one creditor’s garnishment prevents you from paying another creditor, or when you choose between groceries and keeping current on a car payment, bankruptcy becomes the practical answer.

Chapter 7 eliminates most unsecured debts within three to six months and stops garnishment immediately through the automatic stay. Chapter 13 restructures your debts into a manageable three- to five-year plan while halting wage withholding right away. The automatic stay works within 24 hours of filing, meaning your paycheck stops being diverted while you reorganize your finances.

Moving Toward Permanent Relief

Your situation may call for a garnishment dispute, negotiation with creditors, or bankruptcy protection. Understanding which path fits your circumstances requires examining both your income and your total debt load. The choice between these options determines whether you gain temporary relief or permanent financial stability.

How Bankruptcy Stops Wage Garnishment

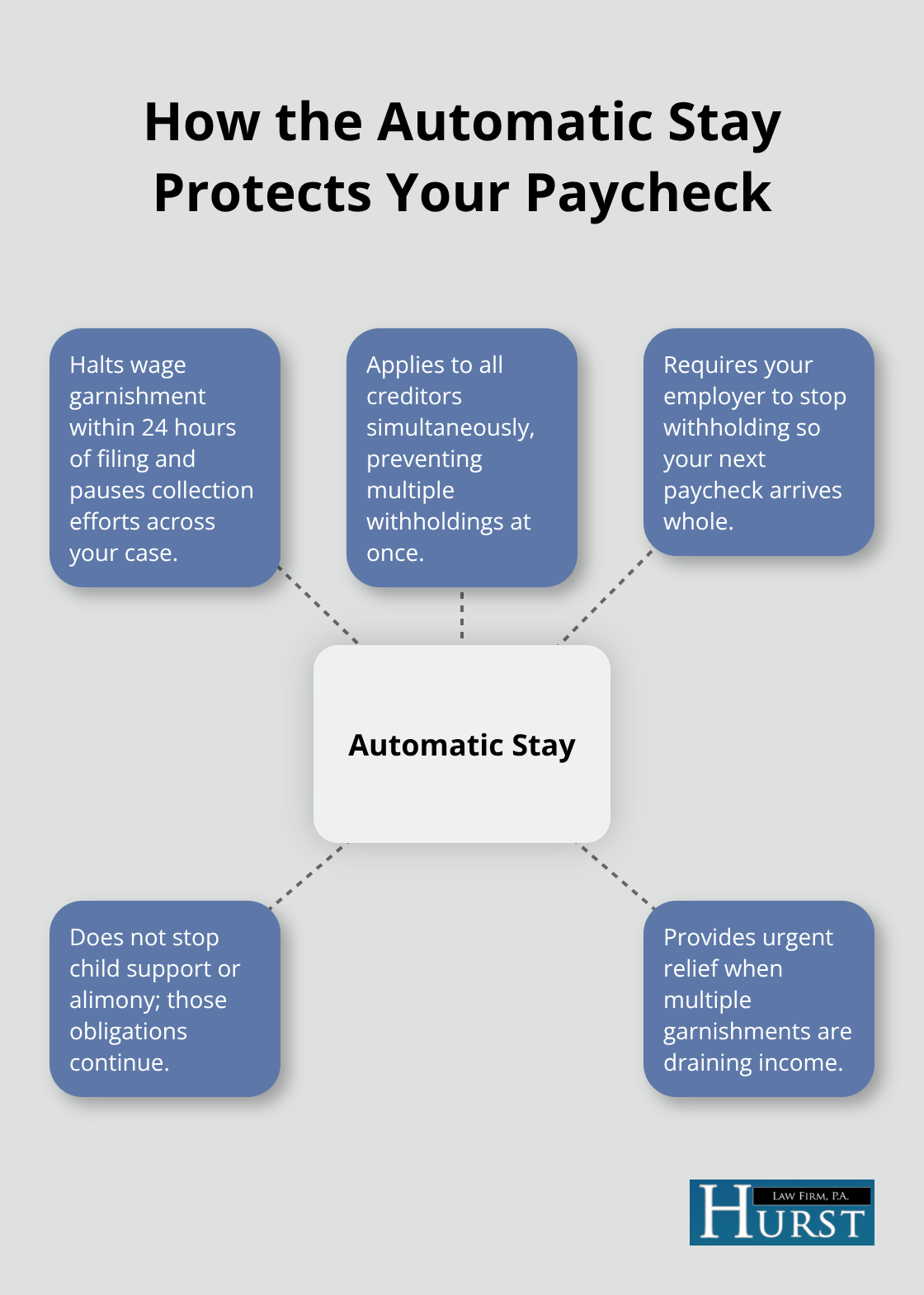

The Automatic Stay Halts Garnishment Immediately

Filing for bankruptcy triggers an automatic stay within 24 hours of submission, and this court order immediately halts wage garnishment across all your debts except child support and alimony. Your employer must stop withholding money the moment the stay takes effect, meaning your next paycheck arrives whole again. The automatic stay works because federal law recognizes that creditors cannot continue collection efforts once a bankruptcy case opens. This protection applies to all creditors simultaneously, which matters enormously if multiple garnishments are draining your income.

Chapter 7 Eliminates the Underlying Debt

Chapter 7 bankruptcy eliminates most unsecured debts like credit cards, medical bills, and payday loans within three to six months if you pass the means test. This elimination removes the underlying judgment that created the garnishment in the first place. Once the debt disappears through discharge, creditors cannot renew the garnishment order because the legal obligation no longer exists. Lower-income workers with minimal assets and substantial unsecured debt find Chapter 7 particularly effective because it wipes out the debts without requiring a repayment plan.

Chapter 13 Restructures Debts Into Affordable Payments

Chapter 13 bankruptcy takes a different approach: it stops garnishment immediately and restructures your debts into a three- to five-year repayment plan based on what you actually can afford. The court calculates your disposable income using the same standards that apply to garnishment calculations, so the amount you pay toward creditors stays reasonable and protects your basic living expenses. Homeowners or vehicle owners who want to keep those assets while reorganizing their obligations benefit most from Chapter 13 protection.

Federal Student Loans and Timing Considerations

Federal student loans present a complication because they cannot be discharged in Chapter 7, but the automatic stay still halts the 15% administrative garnishment while your case is active, giving you breathing room to explore repayment options or income-driven plans. The timing of filing matters significantly because creditors can renew garnishment orders every six months indefinitely. If you file Chapter 7 or Chapter 13 before the six-month renewal, you avoid that cycle entirely.

Why Multiple Garnishments Make Bankruptcy the Practical Choice

Memphis residents facing multiple garnishments gain particular advantage from bankruptcy because the automatic stay stops all collection actions simultaneously, whereas negotiating individual payment plans with each creditor requires separate conversations and carries no guarantee of success. The difference between Chapter 7 and Chapter 13 hinges on whether you have assets to protect or sufficient income to fund a repayment plan. An initial consultation with a bankruptcy attorney determines which path stops your garnishment fastest and delivers the most lasting financial stability.

Final Thoughts

Wage garnishment drains your paycheck month after month, but you have options to stop it. A garnishment dispute Memphis attorney can evaluate whether filing an exemption claim within 10 days makes sense for your situation, or whether bankruptcy offers faster, more permanent relief. Chapter 7 eliminates most unsecured debts and removes the underlying judgment that created the garnishment, while Chapter 13 restructures your obligations into a manageable plan and halts wage withholding immediately (both options trigger an automatic stay within 24 hours).

We at Hurst Law Firm, P.A. understand the pressure of wage garnishment and the urgency of your situation. We offer Chapter 7 and Chapter 13 filings tailored to your circumstances, and we provide a free initial consultation to determine which path stops your garnishment fastest. Every pay period that passes with garnishment in effect is money you cannot use for rent, food, or other essentials.

Contact Hurst Law Firm, P.A. today to discuss your options and take the first step toward financial relief. Your fresh start is within reach.