Chapter 13 bankruptcy offers Memphis residents a structured path to manage debt while keeping assets intact. The process requires careful navigation of court procedures, trustee relationships, and strict payment schedules.

We at Hurst Law Firm, P.A. help clients understand their options and avoid costly mistakes throughout their repayment plan. This guide covers what you need to know about Chapter 13 bankruptcy in Memphis and how local representation makes a real difference.

How Chapter 13 Works in Memphis

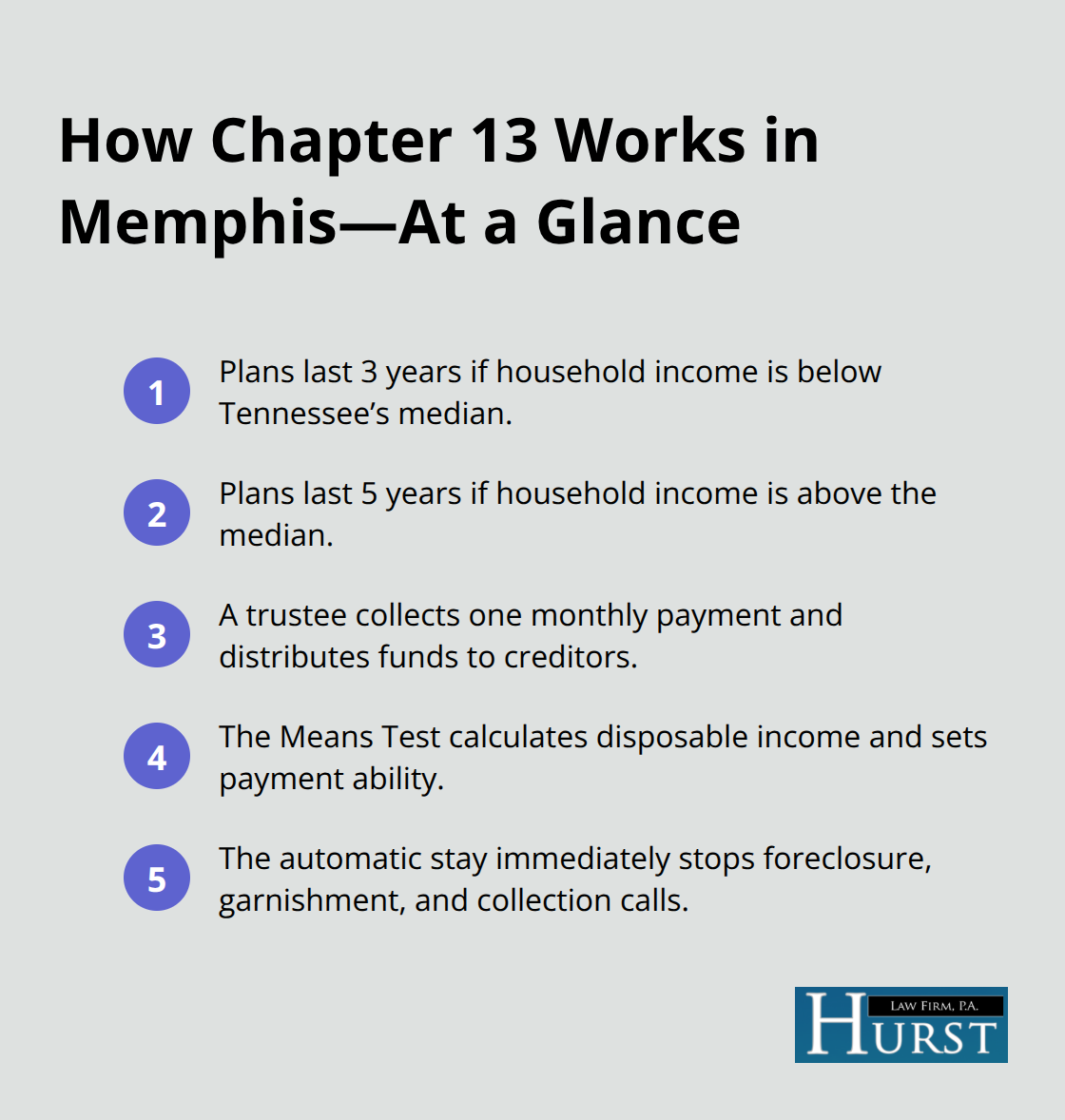

Chapter 13 bankruptcy in Memphis operates on a straightforward principle: you consolidate your debts into a single monthly payment to a court-appointed trustee, who then distributes funds to creditors according to a court-approved plan. The timeline depends on your income. If your household income falls below Tennessee’s median income, your plan lasts three years. If it exceeds the median, you’ll pay for five years. The U.S. Courts determines this income threshold through the Means Test, which calculates your disposable income and becomes the foundation for your monthly payment amount. The trustee manages everything from day one, collecting your payment and distributing funds to creditors as the court orders.

This structure protects you immediately through an automatic stay, which stops wage garnishment, foreclosure, and collection calls the moment you file.

Understanding Your Monthly Payment and Debt Priority

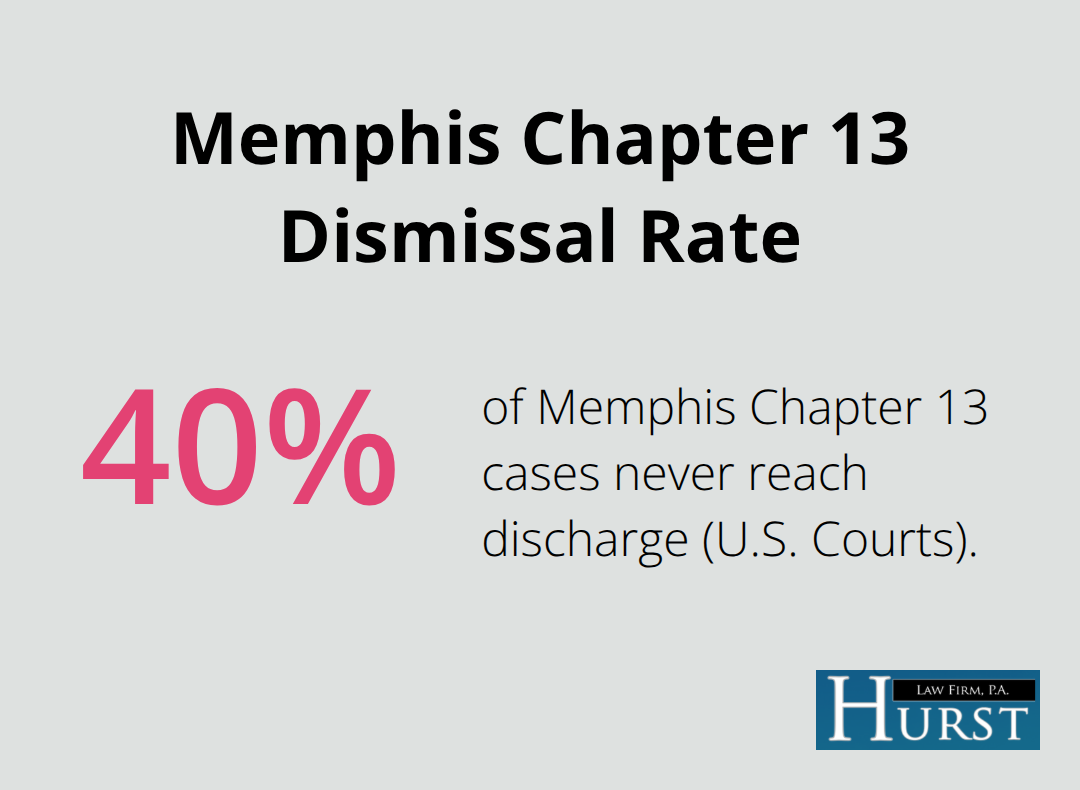

Your monthly payment isn’t arbitrary. The Means Test examines your income against IRS expense standards to determine what you can afford, though here’s where reality matters: actual living expenses often exceed these allowances. Many Memphis filers find that groceries and fuel costs run higher than the standardized amounts. Audit three months of your actual spending before filing to build an accurate picture. Bring pay stubs, mortgage statements, and a detailed expense spreadsheet to your first meeting so the trustee can construct a sustainable plan, not one designed to fail. Debts are organized in priority order. Priority claims like child support and recent tax debts must be paid in full through the plan. Secured debts like mortgages and car loans come next, followed by unsecured debts such as credit cards, which receive whatever remains. This structure means your mortgage arrears can be caught up through the plan while your ongoing monthly mortgage payment continues outside of it. Missing three consecutive payments triggers dismissal, which lifts the automatic stay and exposes you to foreclosure and garnishment again. About 40 percent of Chapter 13 cases are dismissed before discharge, primarily due to payment failures, making payment reliability the difference between success and returning to financial chaos.

Setting Up a Payment System That Works

The Memphis Chapter 13 Trustee’s office strongly encourages electronic payments and does not accept personal checks or cash. Set up automatic payroll deduction if your employer allows it, or arrange automatic bank transfers to a separate savings account earmarked for trustee payments. This removes the temptation to spend money that belongs to creditors. Track your payment history monthly through the trustee’s website or PACER to catch discrepancies early. If your income changes, request a modification promptly rather than skipping payments. Showing good faith through modification requests demonstrates to the court that you’re committed to the plan, not abandoning it when circumstances shift.

What Happens When Life Changes During Your Plan

Income fluctuations are common during a three- to five-year repayment period. A job loss, promotion, or unexpected expense can derail your plan if you don’t act. The court allows you to modify your plan when your financial situation changes materially. Report increases or decreases in income so payments can adjust accordingly. If you face a potential payment shortfall due to emergencies, request a modification rather than skipping payments to show good faith to the court. This proactive approach keeps your case on track and prevents the automatic stay from lifting unexpectedly.

What Derails Chapter 13 Cases in Memphis

The statistics reveal an uncomfortable truth: about 40 percent of Chapter 13 cases filed in Memphis never reach discharge, according to U.S. Courts data. The culprit isn’t complexity or bad luck-it’s preventable mistakes that pile up during the repayment period.

Payment Discipline Separates Success From Failure

Payment discipline matters most. The Memphis Chapter 13 Trustee’s office processes thousands of payments annually, and missing even one triggers consequences. Miss three consecutive payments and the court dismisses your case, lifting the automatic stay that protected you from foreclosure and wage garnishment. You return to the exact financial crisis you filed to escape.

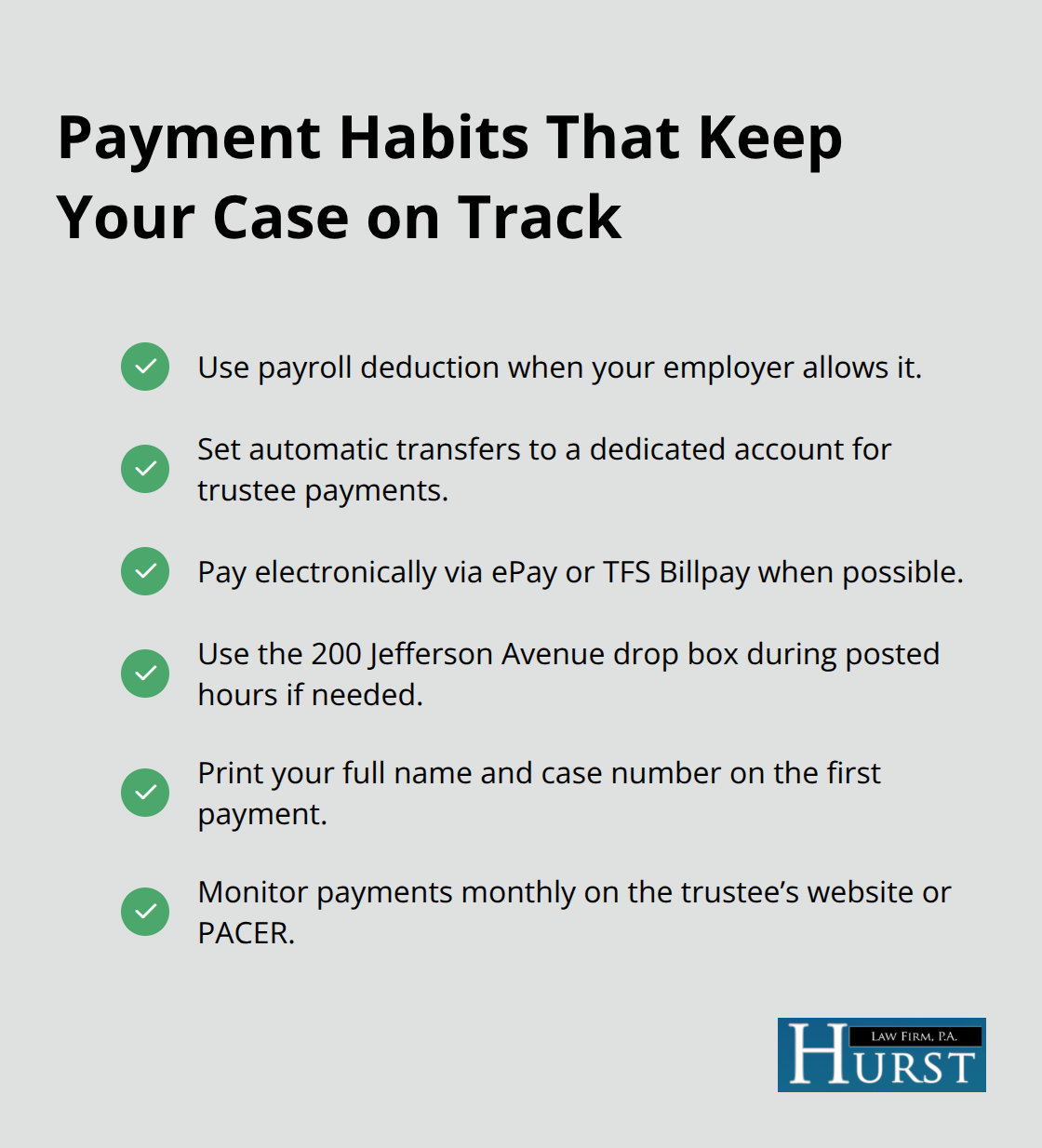

This isn’t theoretical: it happens to people who underestimate the commitment required or who fail to communicate with the trustee when circumstances change. Set up automatic payroll deduction through your employer if possible, or establish automatic bank transfers to a separate savings account earmarked for trustee payments. The Memphis Trustee’s office accepts electronic payments through ePay and TFS Billpay, with a convenient drop box on the 11th floor at 200 Jefferson Avenue open from 7:00 a.m. to 5:00 p.m., Monday through Friday.

Print your full name and case number clearly on your first payment to ensure accurate crediting. Track your payment history monthly through the trustee’s website or PACER to catch processing errors before they compound into missed payment notices.

Disclosure Failures Damage Your Case

Disclosure failures create a second category of dismissals that damages your credibility with the court. You must list every debt and every asset on your filing documents-credit cards you forgot about, medical debts sent to collection, even that old utility bill. Failing to disclose creates grounds for case dismissal and prevents the automatic stay from protecting you against undisclosed creditors. The court expects complete transparency about your financial life.

Unauthorized Debt Signals Bad Faith to Judges

Taking on new debt during your plan requires court permission, and many Memphis filers ignore this requirement entirely. You cannot finance a car, take out a personal loan, or open new credit accounts without filing a Request to Incur Debt form and obtaining court approval. Judges in the Western District of Tennessee, including Hon. Jennie D. Latta, Hon. Jimmy L. Croom, Hon. M. Ruthie Hagan, and Hon. Denise E. Barnett, view unauthorized debt as evidence of bad faith.

If your situation changes materially (job loss, medical emergency, or unexpected expense), request a plan modification immediately rather than skipping payments or taking on debt to cover the shortfall. This demonstrates commitment to the court and keeps your case on track toward discharge. The trustee works with you when you communicate proactively, but silence or avoidance leads directly to case dismissal and financial ruin.

Why Local Representation Makes the Difference

Understanding Memphis Bankruptcy Court Procedures

The Western District of Tennessee bankruptcy courts operate under specific procedural rules that differ from federal courts in other regions. Judges in Memphis apply these rules consistently based on their individual preferences and past rulings. Hon. Jennie D. Latta, Hon. Jimmy L. Croom, Hon. M. Ruthie Hagan, and Hon. Denise E. Barnett each bring distinct approaches to Chapter 13 cases. Knowing how each judge interprets the Means Test, evaluates plan feasibility, and responds to modification requests gives you a concrete advantage. A Memphis attorney familiar with these judges understands which arguments resonate in front of Hon. Latta versus Hon. Croom, how strictly each applies IRS expense standards, and when to push back on trustee objections.

Working With Local Trustees and Their Preferences

The three Chapter 13 Trustees managing Western District cases-Jennifer Cruseturner, Sylvia Brown, and Timothy Ivy-each have documented preferences about plan structure, payment timing, and communication protocols. Local representation navigates these preferences instinctively. When you file Chapter 13 in Memphis, the Memphis Chapter 13 Trustee’s office at 200 Jefferson Avenue processes your payments, schedules your meeting of creditors via virtual §341 meetings (available since September 2023), and handles all administrative tasks that determine whether your case succeeds or fails. Virtual meetings mean you no longer travel downtown for creditor meetings, but the trustee still expects you to answer questions thoroughly and honestly about your finances.

Navigating Electronic Filing and Local Requirements

Local representation ensures your documents are formatted correctly for electronic filing through the Western District’s ECF system. Your plan addresses local lien issues specific to Tennessee property law. This attention to detail avoids the procedural dismissals that plague self-represented filers. The real advantage emerges when complications arise. If your mortgage lender files a claim that conflicts with your plan’s treatment of arrears, a local attorney immediately recognizes the issue and files the proper response before deadlines pass.

Managing Trustee Objections and Plan Modifications

If the trustee objects to your plan’s feasibility-a common occurrence when filers underestimate actual living expenses-your attorney has already built relationships with the trustee and knows exactly what modifications the court will approve. Hurst Law Firm, P.A. has served Memphis since 1997 and understands that Chapter 13 success depends on sustainable plans tailored to your actual income and expenses, not theoretical numbers. When income changes force a modification, when an emergency threatens your payment schedule, or when creditors dispute claims, having representation familiar with the Memphis bankruptcy community prevents the case dismissals that derail 40 percent of Chapter 13 filers before discharge.

Final Thoughts

Chapter 13 bankruptcy in Memphis succeeds when you understand three core principles: your plan must reflect actual living expenses, not theoretical numbers; payment discipline determines whether you reach discharge or face dismissal; and local representation prevents the procedural mistakes that derail 40 percent of cases before completion. The statistics are stark, but the path forward is clear. You consolidate debts into one manageable payment, the automatic stay stops creditors immediately, and three to five years of consistent payments lead to a fresh start.

Memphis chapter thirteen help requires more than filing paperwork. It demands understanding how judges like Hon. Jennie D. Latta and Hon. Jimmy L. Croom evaluate your plan, knowing the preferences of trustees Jennifer Cruseturner, Sylvia Brown, and Timothy Ivy, and recognizing that electronic filing rules and local lien issues affect your outcome. Self-represented filers often miss these details and end up dismissed.

We at Hurst Law Firm, P.A. have guided Memphis residents through Chapter 13 since 1997, helping thousands of individuals and families escape financial distress and build sustainable repayment plans tailored to their actual circumstances. Contact us for a free initial consultation to assess your Chapter 13 eligibility by calling 901-725-1000 or visiting our Memphis office at 2287 Union Avenue.