Credit card debt can spiral quickly, trapping you in a cycle of interest payments and growing balances. Most people don’t realize how fast their debt compounds or when they’ve crossed from manageable to unmanageable.

We at Hurst Law Firm, P.A. help Memphis residents manage credit card debt through practical strategies and legal solutions. This guide walks you through proven methods to regain control of your finances, and when bankruptcy might be your best option.

How Credit Card Debt Actually Destroys Your Finances

Credit card interest doesn’t just sit there-it compounds daily, meaning you pay interest on your interest. A balance of $10,000 at 18% APR costs you roughly $1,800 per year if you make no payments, but that calculation assumes simple interest. In reality, card issuers calculate interest daily and add it to your balance, so the next day’s interest calculation applies to a larger number. After six months of inactivity, that $10,000 balance grows to approximately $10,930. After one year, you’re looking at nearly $11,956. This is why people feel trapped so quickly-the debt grows faster than they can pay it down.

Your Debt-to-Income Ratio Reveals the Damage

Your debt-to-income ratio tells the story of how bad things have become. If you earn $4,000 monthly and carry $15,000 in credit card debt, your ratio is 3.75:1, which signals serious financial stress to lenders and limits your ability to borrow for anything else. Banks and creditors view ratios above 2:1 as high risk. This matters because creditors use your ratio to decide whether to approve new credit, increase your limits, or even continue existing agreements. High ratios also drain your monthly cash flow-if minimum payments consume 15% or more of your income, you have virtually no flexibility for emergencies or savings.

The Minimum Payment Trap

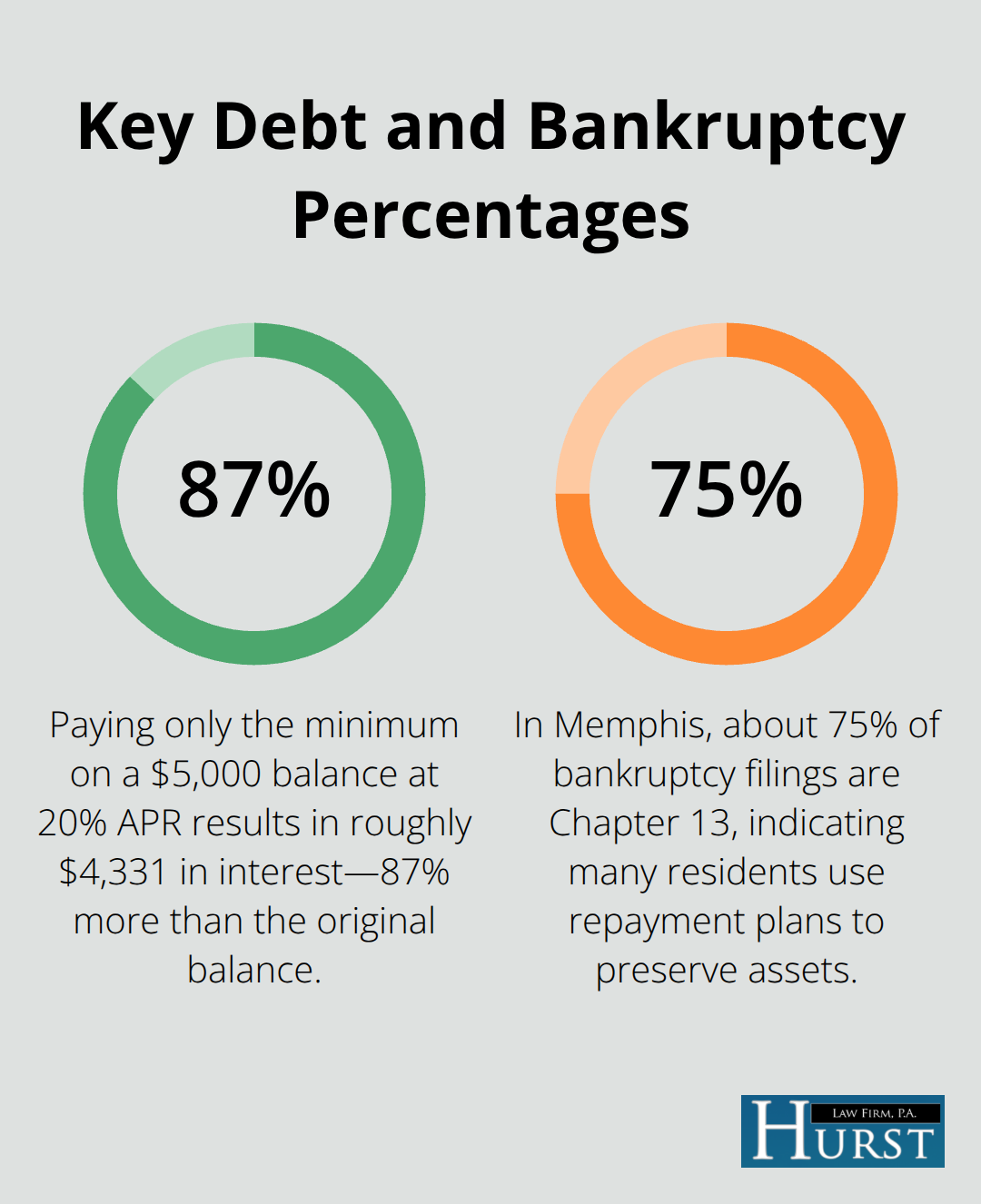

Minimum payments are designed to keep you paying for years while the card issuer collects interest. On a $5,000 balance at 20% APR, the minimum payment might be $125 monthly. Paying only the minimum means you’ll need roughly 75 months-over six years-to clear that debt, and you’ll pay approximately $4,331 in interest alone. That’s 87% more than your original balance.

Memphis residents often don’t realize they can negotiate directly with creditors for lower rates before their situation becomes dire. A simple call explaining your situation and asking for a rate reduction works surprisingly often, especially if you’ve maintained a decent payment history. Even a 2-3% reduction cuts years off your payoff timeline and saves thousands.

Breaking Free From the Minimum Payment Cycle

The reality is that minimum payments trap you through mathematics, not accident. Card companies profit when you stay in debt, so they structure minimums to keep balances alive. Breaking free requires you to pay significantly above the minimum-at least 10% of your balance monthly, or ideally a fixed amount tied to a payoff deadline rather than a percentage of what you owe.

When your own efforts to negotiate rates and accelerate payments fail to move the needle, and your debt-to-income ratio climbs beyond your control, professional intervention becomes necessary. Some Memphis residents find that bankruptcy offers the relief they cannot achieve through standard debt repayment strategies.

How to Actually Pay Down Credit Card Debt

The Avalanche Method Beats the Snowball Every Time

Two debt repayment methods dominate the conversation: the avalanche and the snowball. The avalanche method targets your highest-interest cards first while you make minimum payments on everything else. If you owe $3,000 at 22% APR, $2,000 at 15% APR, and $1,500 at 8% APR, the avalanche method directs your extra payments toward that 22% card. Mathematically, this approach saves the most money because interest compounds fastest on high-rate debt. Research from the Federal Reserve shows that consumers using the avalanche method save approximately 15-20% more in total interest compared to the snowball approach.

The snowball method targets your smallest balance first regardless of interest rate. It feels faster because you eliminate a debt entirely, which triggers a psychological win. However, that psychological boost costs you real money-potentially hundreds or thousands in unnecessary interest. Unless your motivation would collapse without early wins, the avalanche method delivers superior results. Memphis residents carrying multiple cards should organize debts by interest rate, calculate the difference between minimum payments and what they can actually afford to pay, then apply every dollar above the minimum to that highest-rate card.

Negotiate Lower Rates Before Debt Spirals

Negotiating directly with your card issuer before things spiral works far better than most people realize. Call your issuer’s customer service line and ask to speak with someone about your account. Explain that you’re working to pay down your balance but the interest rate is making progress difficult. Request a rate reduction-even 2-3 percentage points makes a dramatic difference. On a $5,000 balance, dropping from 20% to 17% APR saves you roughly $900 in interest over three years of payments.

Card companies often approve these requests, especially if you’ve maintained a decent payment history and haven’t missed recent payments. If they refuse, ask to speak with a supervisor or try again in a few months. Some issuers will also waive annual fees or lower your rate temporarily as retention incentives.

Build a Budget That Forces Action

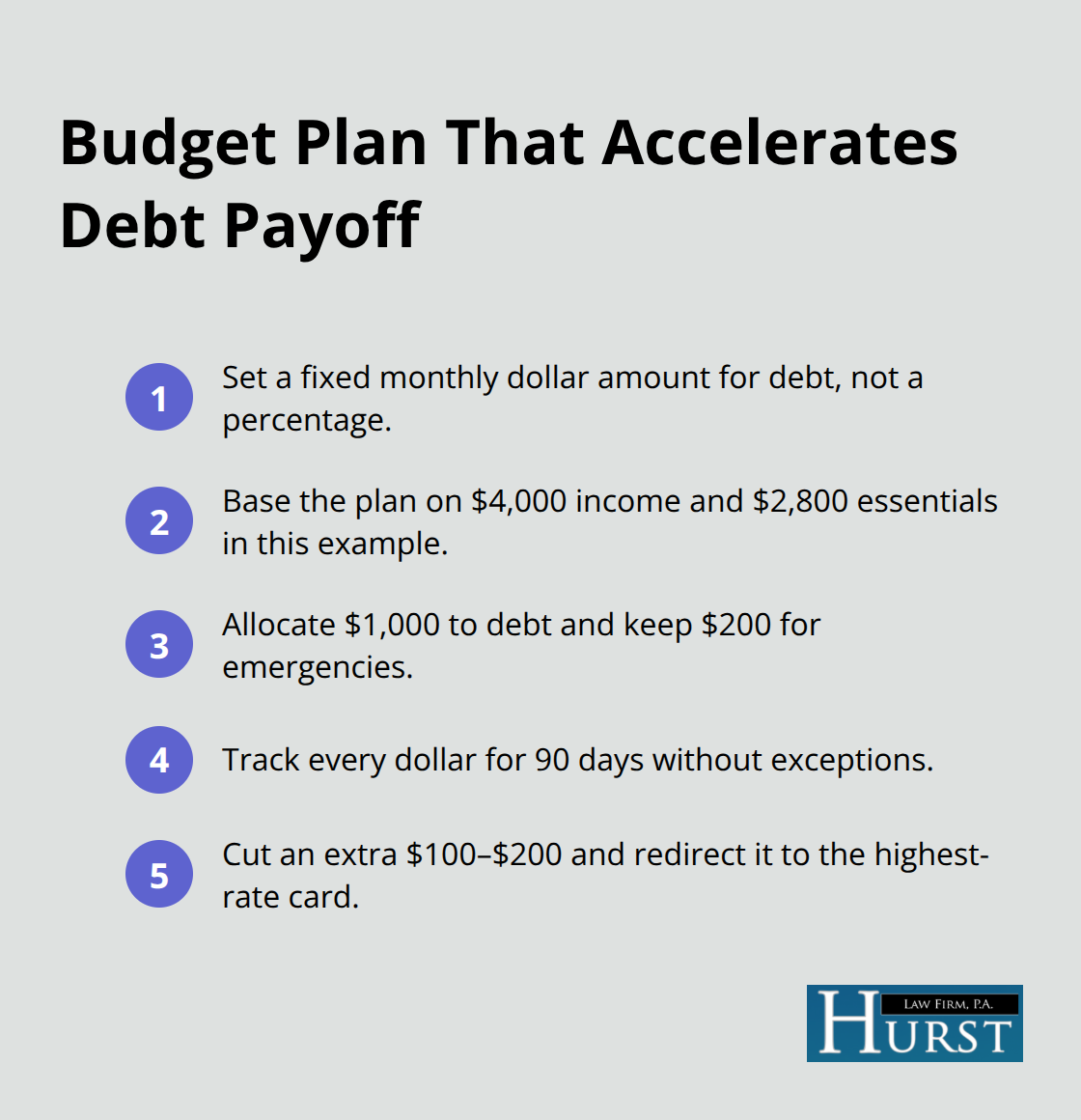

A realistic budget forces you to allocate a specific dollar amount toward debt each month rather than paying percentages of your balance. The Memphis area has a median household income of approximately $48,000 annually according to recent census data. If you earn $4,000 monthly and spend $2,800 on housing, food, utilities, and transportation, you have $1,200 remaining. Allocate $1,000 to debt repayment and protect $200 for emergencies-that $200 prevents you from charging new balances when unexpected expenses hit.

Track this budget for 90 days without exception. Most people discover they can cut another $100-200 monthly once they see where money actually goes. Redirect those savings immediately to your highest-interest card. This combination of rate negotiation and disciplined budgeting creates momentum that minimum payments never achieve.

When Your Own Efforts Fall Short

The reality is that some Memphis residents exhaust these strategies and still find their debt-to-income ratio climbing beyond control. Your card issuer refuses to negotiate, your budget reaches its limit, and the avalanche method shows you’ll need years to break free. At that point, professional intervention becomes necessary. Some situations demand debt relief solutions that standard debt repayment cannot provide, and that’s when bankruptcy enters the conversation as a legitimate path forward.

When Debt Requires Professional Intervention

Warning Signs That Demand Action

Your budget is maxed out, your card issuer won’t negotiate further, and you’re paying $400 monthly just in interest while your principal barely moves. This is the moment most Memphis residents realize that personal discipline alone cannot solve their situation. The warning signs appear gradually at first, then accelerate. You start missing payments or paying late because the money simply isn’t there. Collection calls increase in frequency. You receive notices about lawsuits or wage garnishment. Your debt-to-income ratio has climbed beyond 4:1, meaning your monthly debt obligations consume more than 25% of your gross income. The American Bankruptcy Institute reports that over 130,000 Americans file for bankruptcy annually, and credit card debt drives the majority of these filings. If you experience multiple warning signs simultaneously, bankruptcy often becomes not a last resort but a rational financial decision that stops the bleeding faster than any debt repayment strategy.

How Bankruptcy Stops the Cycle

Bankruptcy provides what negotiation and budgeting cannot: legal protection and a structured path to elimination or reorganization of your debts. An automatic stay takes effect immediately upon filing, which stops creditor calls, wage garnishment, and collection lawsuits. This legal shield gives you breathing room to assess your options without constant pressure from creditors. The filing fee is $338 (with potential waivers for low-income filers), and you must complete credit counseling before filing. Most people report that their financial stress diminishes rapidly once the automatic stay takes effect and they know exactly what comes next.

Chapter 7: Complete Discharge of Unsecured Debt

Chapter 7 bankruptcy discharges most unsecured debts like credit cards entirely. The process takes approximately 3 to 6 months from filing to discharge. According to the American Bankruptcy Institute, over 95% of Chapter 7 cases result in a successful discharge. Chapter 7 requires income below roughly $39,759 for a single person or $93,767 for a family of four, though allowable expenses can push eligibility higher. A court-appointed trustee oversees your case, and you attend a 341 meeting (meeting of creditors) typically 30–45 days after filing. The discharge is usually granted 60–90 days after the 341 meeting.

Chapter 13: Reorganization Through a Repayment Plan

Chapter 13 bankruptcy consolidates your debts into a single repayment plan over 3 to 5 years. This option allows you to catch up on mortgage or car payments while discharging the remainder of your debts. In Memphis, about 75% of bankruptcy filings are Chapter 13, suggesting local residents frequently use this option to preserve assets while reorganizing their obligations. Chapter 13 requires a steady income from employment, trusts, retirement plans, or other viable sources. Upon successful completion of the plan, the remaining dischargeable debts are discharged, providing relief.

Choosing the Right Path for Your Situation

The choice between Chapter 7 and Chapter 13 depends on your income level, asset protection needs, and whether you can sustain a repayment plan. Hurst Law Firm, P.A., a bankruptcy law firm in Memphis led by attorney Herbert Hurst and serving the community since 1997, helps residents evaluate which bankruptcy chapter fits their specific situation and guides them through the filing process.

Final Thoughts

Managing credit card debt in Memphis requires honest assessment of what you can accomplish alone versus when professional help becomes necessary. The strategies outlined here-negotiating lower rates, using the avalanche method, and building a disciplined budget-work for many people and reduce interest costs significantly. However, these approaches have limits, and when your debt-to-income ratio climbs beyond 4:1, personal effort reaches its ceiling.

This is the moment to stop viewing bankruptcy as failure and start viewing it as a financial tool. Chapter 7 eliminates unsecured debts like credit cards entirely, with over 95% of cases resulting in discharge, while Chapter 13 reorganizes your obligations into a manageable repayment plan over 3 to 5 years. Both options trigger an automatic stay that stops collection calls and wage garnishment immediately, giving you the breathing room to move forward.

Credit recovery after bankruptcy is entirely possible through secured credit cards, consistent on-time payments, and disciplined budgeting-many filers rebuild their scores within 2-3 years. Contact Hurst Law Firm, P.A. for a free initial consultation to evaluate your options and take action on your path forward. Call 901-730-4958 or visit 44 North Second Street, Suite 403, Memphis, TN 38103.