Debt spirals fast for Memphis TN families. Medical bills, job loss, or credit card balances can pile up until monthly payments feel impossible and creditors won’t stop calling.

Bankruptcy relief for families exists, and it’s not the financial death sentence many believe it to be. We at Hurst Law Firm, P.A. help families understand their options and find the path forward.

When Debt Becomes Unmanageable

Debt accumulates faster than most Memphis TN families realize. A single medical emergency triggers a cascade of bills that insurance doesn’t cover. The Consumer Financial Protection Bureau reports that 43 million Americans carry medical debt averaging $2,424 each, and many families in Memphis face similar burdens. Job loss compounds the problem immediately, leaving families unable to cover basic monthly expenses around $4,200. Credit card debt worsens the situation because APRs commonly range from 18 to 24 percent, meaning minimum payments often cover only interest while the balance grows. When debt payments exceed 40 percent of monthly income, the financial pressure becomes severe and nearly impossible to manage without intervention.

Recognizing the Warning Signs

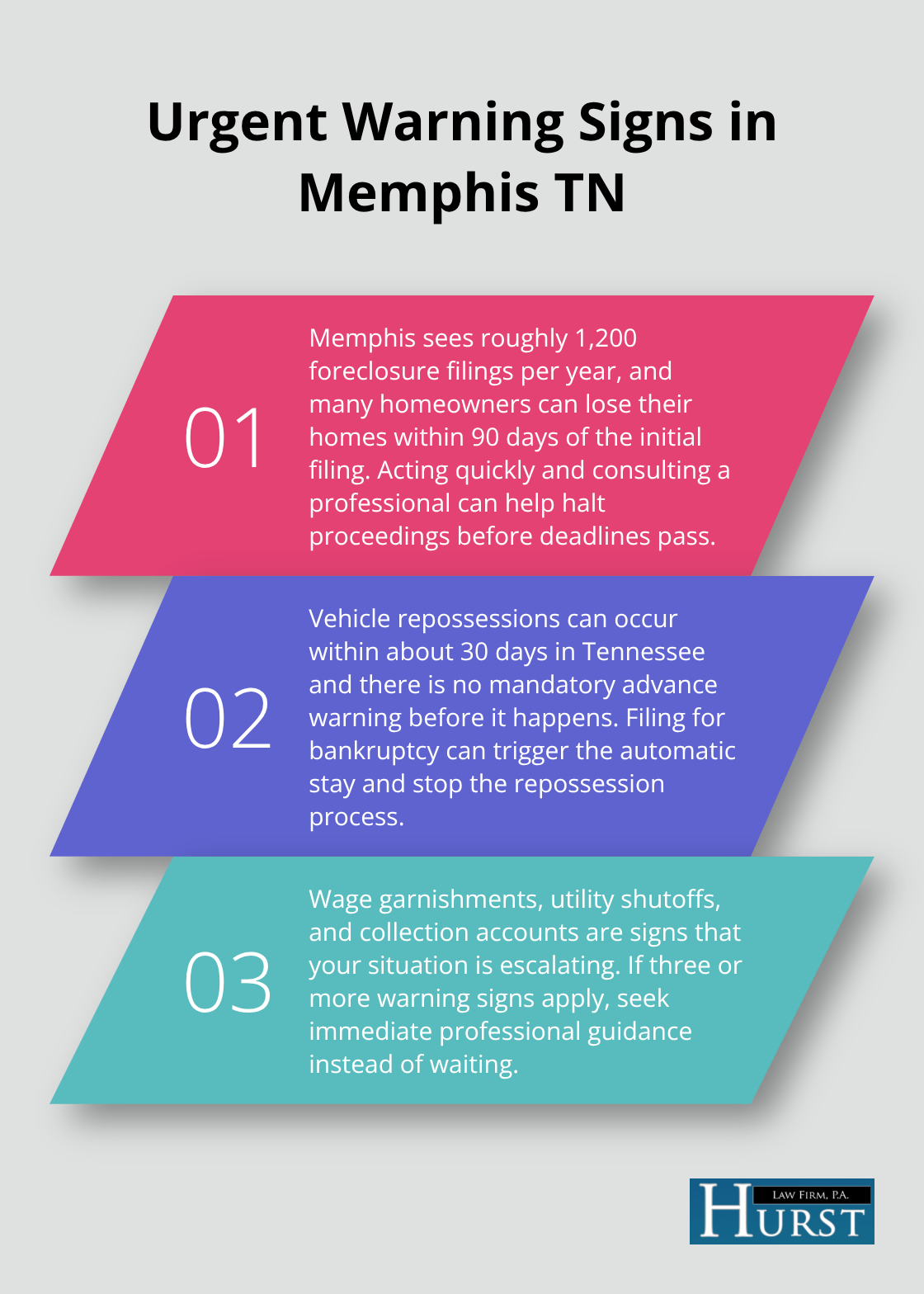

Specific red flags indicate bankruptcy may be necessary. If you use credit cards to pay for groceries, utilities, or other essentials, your income no longer covers basic needs. When creditors call repeatedly despite your efforts to pay, or when you receive foreclosure or repossession notices, time runs short. Memphis sees roughly 1,200 foreclosure filings per year, and many homeowners lose their homes within 90 days of the initial filing. Vehicle repossessions can occur within about 30 days, and Tennessee law imposes no mandatory advance warning before repossession happens.

Wage garnishment notices, utility shutoffs, or collection accounts on your credit report all signal that bankruptcy warrants serious consideration. If three or more of these situations apply to your family, bankruptcy deserves immediate professional attention rather than continued struggle with creditors.

The Financial and Emotional Toll

The stress of overwhelming debt affects every aspect of family life. Financial instability creates constant anxiety about which bills to pay first and how to keep the lights on. This pressure damages relationships, impacts sleep quality, and affects work performance. Shelby County residents filed bankruptcy at the highest rate among the 100 largest counties in 2023, averaging six filings per 1,000 residents. This statistic reveals that financial crisis doesn’t discriminate and affects many otherwise responsible families. The automatic stay that comes with a bankruptcy filing provides immediate relief by stopping creditor calls, lawsuits, and collection actions the moment your petition is filed. For families drowning in debt, this protection alone restores enough mental clarity to plan the next steps forward.

Understanding Your Path Forward

The weight of financial crisis can feel permanent, but relief exists through structured bankruptcy options. Chapter 7 and Chapter 13 bankruptcy both offer legitimate paths to stop creditor harassment and regain control of your finances. Each option works differently depending on your income, assets, and specific debt situation. Understanding how these two approaches differ helps you determine which one fits your family’s circumstances and goals.

Chapter 7 vs. Chapter 13 Bankruptcy in Memphis TN

How Chapter 7 Liquidation Works

Chapter 7 bankruptcy moves quickly and discharges most unsecured debts within three to six months. This option works best for families with limited income and few assets to protect. In Chapter 7, a trustee may liquidate non-exempt property to pay creditors, but Tennessee exemptions shield most family assets. The homestead exemption protects up to $35,000 for individuals and $52,500 for married couples. A $10,000 wildcard covers personal property, and retirement accounts receive unlimited protection up to $1,512,350 per person. About 95 percent of Chapter 7 filers keep all their property because these state exemptions cover nearly everything families actually own.

The discharge rate reaches about 99 percent, meaning debts disappear within four to six months according to the American Bankruptcy Institute. Income matters significantly: if your household income falls below Tennessee’s 2025 means test median of $39,759 for single filers or $93,767 for families of four, Chapter 7 eligibility is straightforward. Above these thresholds, the means test calculates whether you have disposable income after essential expenses. Monthly disposable income between $7,475 and $12,475 triggers closer examination, while above $12,475 often leads to disqualification.

Chapter 7 discharges credit cards, medical bills, personal loans, and tax debts older than three years. However, this option cannot touch student loans, child support, alimony, or recent tax obligations. For families overwhelmed by credit card and medical debt, Chapter 7 offers genuine relief when other debts remain manageable.

How Chapter 13 Reorganization Works

Chapter 13 works differently and suits families with steady income who want to keep their homes or vehicles. This option consolidates debts into a court-approved repayment plan lasting three to five years, with remaining eligible debts discharged after completion. Chapter 13 stops foreclosure or repossession immediately through the automatic stay, giving you time to catch up on mortgage or car payments within the plan structure. You can file Chapter 13 even while pursuing a loan modification, providing flexibility that Chapter 7 cannot offer.

The plan includes mortgage debt, medical debt, credit card debt, and tax debt, reorganizing everything into one affordable monthly payment. Income requirements differ from Chapter 7: you simply need steady income from employment, retirement, dividends, or other viable sources. The U.S. Trustee Program reports that Memphis trustees handle 200 to 300 cases monthly, so filing with proper documentation and professional guidance matters tremendously.

Choosing Between Chapter 7 and Chapter 13

Families earning $50,000 to $80,000 annually often find Chapter 13 more suitable because they have enough income to fund a repayment plan but still struggle with debt ratios. Unlike Chapter 7, which eliminates debts quickly, Chapter 13 requires discipline to complete the full plan term, but protects assets and stops creditor harassment immediately upon filing. Chapter 7 works best if you need fast debt elimination and have minimal assets or income. Chapter 13 works best if you want to preserve your home or vehicle while reorganizing debts into manageable payments.

The right choice depends on your specific financial situation, income level, and whether you have property you want to protect. Understanding these differences helps you move forward with confidence toward the bankruptcy process itself.

The Bankruptcy Process and What to Expect

Gather Your Documentation Before Filing

Filing for Chapter 7 or Chapter 13 requires substantial documentation that the bankruptcy court demands before your case can proceed. You must collect four years of tax returns, six months of pay stubs, and six months of bank statements to prove your income and spending patterns. Asset and debt lists need to be complete and accurate, including mortgage statements, vehicle titles, insurance policies, and any recent property transfers. The court also requires proof that you completed credit counseling within 180 days before filing. Many Memphis families underestimate how thorough this preparation must be, but disorganized filings delay your discharge and frustrate the trustee handling your case. Memphis trustees process 200 to 300 cases monthly according to the U.S. Trustee Program, which means they move quickly through organized files and slow considerably with incomplete paperwork. Thorough preparation prevents unnecessary delays and keeps your timeline on track toward financial relief.

The Automatic Stay Stops Collection Actions Immediately

The moment you file your bankruptcy petition, an automatic stay takes effect that halts nearly all creditor actions. Foreclosure proceedings stop, wage garnishments cease, and collection calls end. This protection applies whether you file Chapter 7 or Chapter 13, giving your family immediate breathing room to organize your finances without constant harassment. Creditors cannot pursue lawsuits, repossession, or utility shutoffs once the automatic stay is in place. The court sends notice to all creditors within days of your filing, and violations of the stay carry serious penalties. For families facing imminent foreclosure or repossession, this immediate protection often determines whether you keep your home or vehicle. The stay lasts throughout your bankruptcy case, providing continuous protection while you work toward either liquidation or reorganization depending on which chapter you filed.

The 341 Meeting of Creditors

Your Chapter 7 case includes a 341 Meeting of Creditors that occurs 20 to 40 days after filing and typically lasts only 5 to 10 minutes. The trustee asks questions about your income, assets, and debts while creditors rarely attend. Creditors have 60 days to object to your discharge, but objections are uncommon when you have properly listed all assets and debts. Your discharge arrives 90 to 120 days after filing if no complications arise, officially eliminating most unsecured debts. Chapter 13 cases take longer because you enter a repayment plan lasting three to five years, but the automatic stay protects you throughout the entire process.

Timeline From Filing to Discharge

Your Chapter 7 case typically moves from petition to discharge in three to six months if your documentation is complete and you finish the required credit counseling courses. The upfront costs remain minimal at $338 for the filing fee plus the cost of mandatory credit counseling, making bankruptcy accessible even for families with tight budgets. Acting quickly matters because filing before your financial situation deteriorates further protects more home equity and personal property through exemptions. Chapter 13 requires discipline to complete the full plan term, but the timeline provides structure that helps families rebuild their finances systematically over three to five years.

Final Thoughts

Bankruptcy relief for families stops creditor harassment immediately and provides a structured path to rebuild your financial foundation. Whether you select Chapter 7 or Chapter 13, the automatic stay protects your home and vehicle while you work through either liquidation or reorganization based on your income and assets. Memphis families file bankruptcy at rates higher than most communities, which means financial crisis affects many otherwise responsible households and removes the stigma surrounding this practical decision.

Taking action now matters more than waiting for your situation to worsen. The longer you delay, the more equity you lose in your home and the closer you move toward foreclosure or repossession. Filing before deterioration accelerates your path to discharge and protects more of your assets through state exemptions.

We at Hurst Law Firm, P.A. help Memphis families navigate consumer bankruptcy and achieve fresh starts from financial distress. Contact us at 901-730-4958 or visit our office at 44 North Second Street, Suite 403, Memphis, TN 38103 to schedule your free initial consultation where we discuss your specific situation and answer your questions about the process ahead.