A Chapter 13 repayment plan gives you a structured way to handle debt while keeping your assets. Instead of liquidating everything, you make manageable monthly payments over three to five years.

At Hurst Law Firm, P.A., we help Memphis TN residents understand exactly how these payments work and what to expect. This guide breaks down the calculation, payment priorities, and what happens if your situation changes.

How Your Income and Expenses Determine What You Pay

Your Chapter 13 payment starts with a straightforward calculation: take your average income over the last six months, subtract your actual living expenses, and what remains is your disposable income. This number funds your entire repayment plan. The Tennessee Means Test applies specific expense standards to this calculation, using national averages for food and clothing, regional standards for transportation, and local standards for housing and utilities.

These standards often underestimate real costs in Memphis. Grocery allowances typically run around $1,200 monthly according to IRS expense standards, but families actually spend $1,600 to $1,800 for a household of four. Gasoline costs fall short by about 40%. This gap matters because if your budget assumes lower expenses than you actually face, you’ll struggle to make payments consistently.

Why Underestimating Expenses Leads to Plan Failure

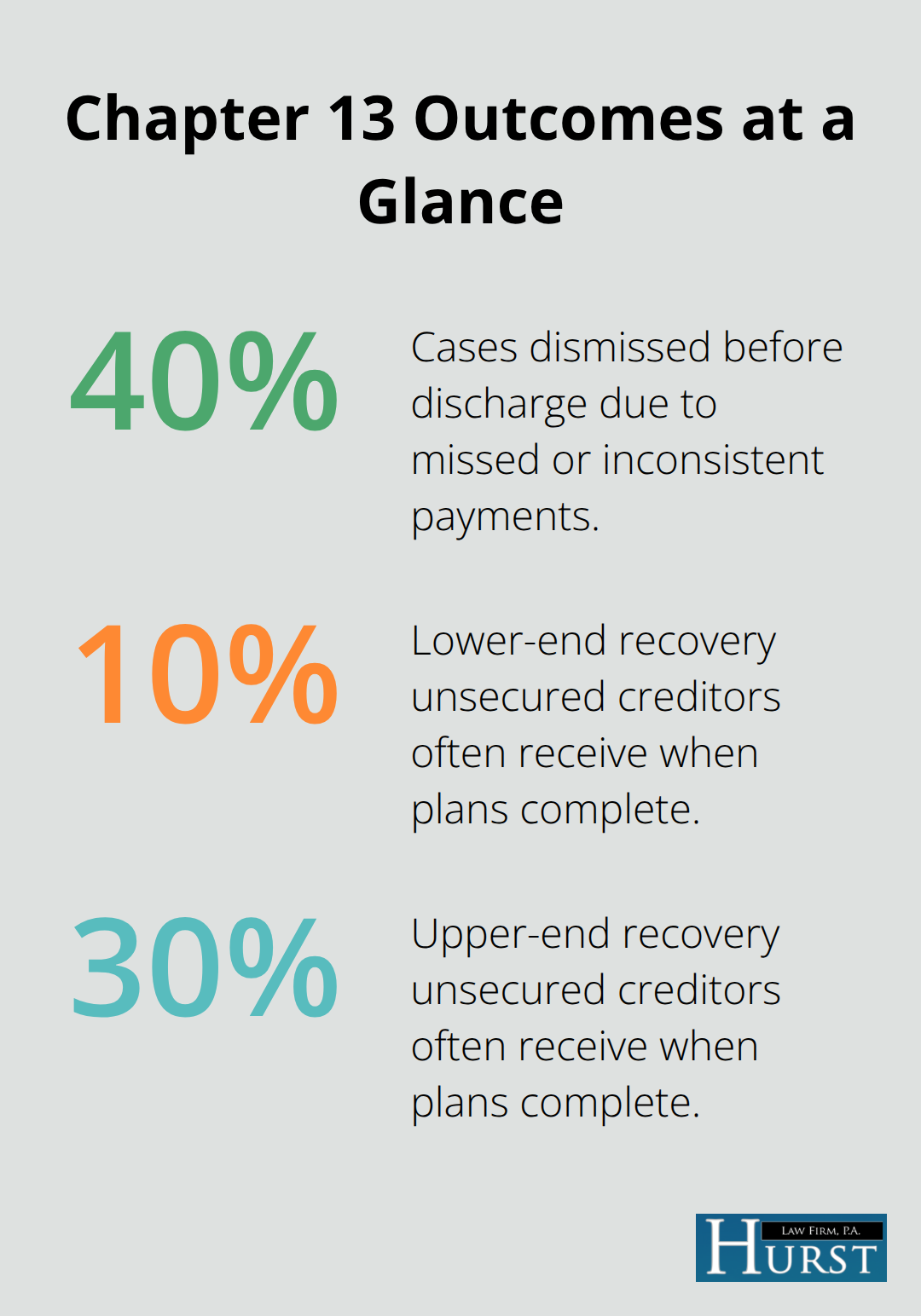

According to U.S. Courts data, roughly 40% of Chapter 13 cases face dismissal before discharge due to failure to maintain consistent monthly payments. The most common reason is that filers underestimate their true living costs during planning. You need to audit three months of real spending before filing to build a budget you can actually sustain.

Standard allowances often understate costs significantly, so your actual expenses should guide your plan, not IRS tables alone.

Your Repayment Timeline Depends on Your Income Level

The length of your plan-three or five years-hinges on whether your average monthly income falls below or above the Tennessee median for your household size. If you earn below the median of $39,759 annually for a single person or $48,053 for two people, your plan runs three years. Above those thresholds, you commit to five years.

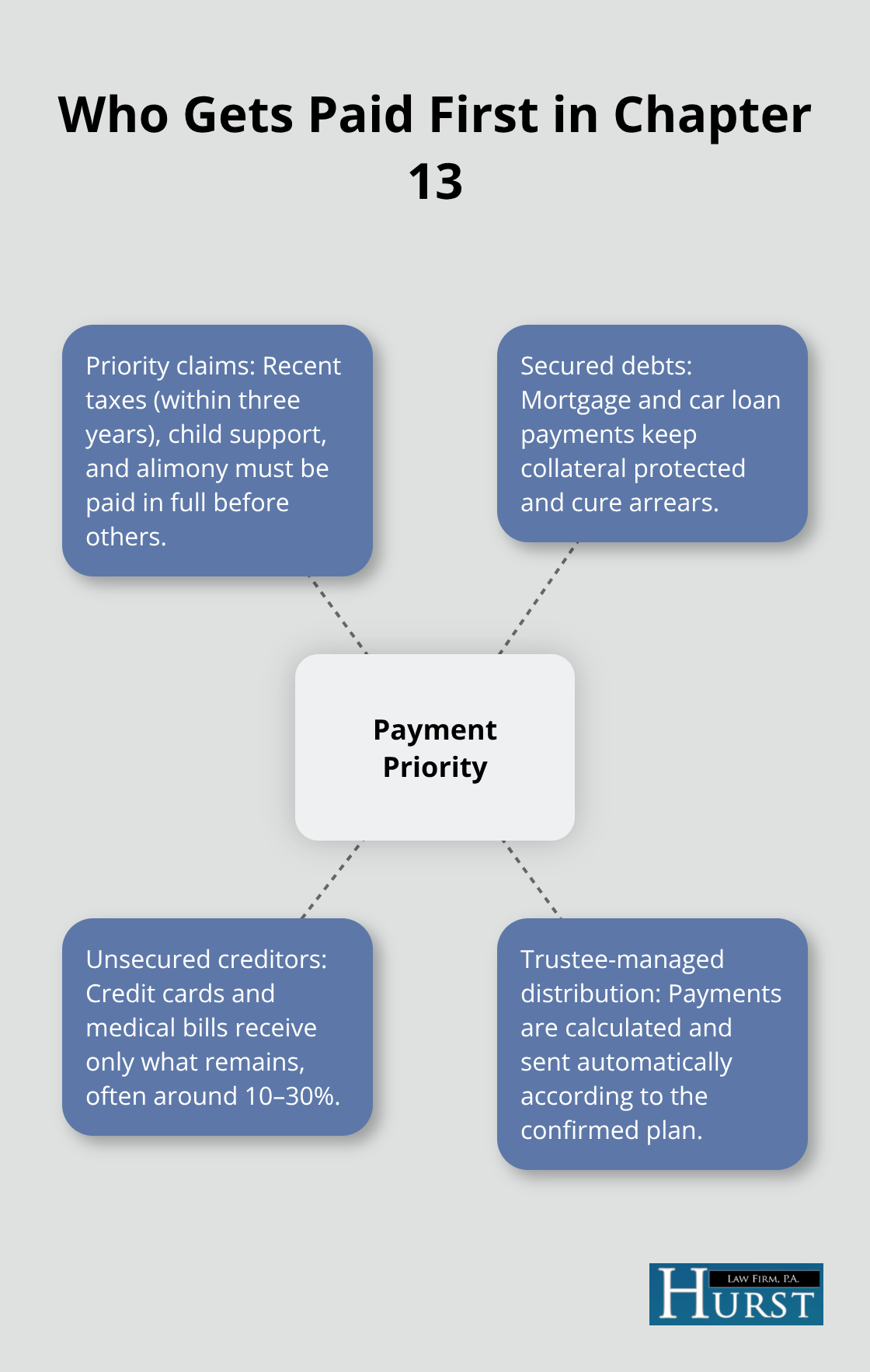

This difference matters significantly because a five-year plan spreads your disposable income thinner across 60 months rather than 36. Your secured debts like mortgages and car loans receive payment first through the plan, followed by priority claims such as recent tax debts and child support arrears. Unsecured creditors-credit card companies and medical providers-receive whatever remains after these obligations.

How Creditors Actually Get Paid Under Your Plan

Research shows unsecured creditors often receive only 10 to 30% of what’s owed, with the remainder discharged when you complete the plan. This structure means your actual monthly payment is determined by dividing your total disposable income over the applicable commitment period, not by what creditors demand. You’re not paying based on original debt amounts; you’re paying based on what you can genuinely afford. Understanding this priority system helps you see why consistent payments matter-your plan protects your home and vehicle while addressing debts in a legal order that the court enforces.

How Your Monthly Payment Gets Calculated and Distributed

The Disposable Income Formula That Funds Your Plan

Your disposable income is the engine that drives your entire Chapter 13 plan, and it’s calculated using a formula the court applies consistently across all cases. You take your average monthly income over the last six months, subtract the expenses the Tennessee Means Test allows, and the remainder becomes your monthly obligation to the trustee. This isn’t negotiable or based on what creditors demand-it’s purely mathematical. For a Memphis family of four, if your average income is $5,000 monthly and allowed expenses total $3,200, your disposable income is $1,800. That $1,800 funds your plan for either 36 or 60 months depending on whether you fall below or above Tennessee’s income median. The trustee receives this payment reliably, typically through payroll deduction, which prevents the payment failures that derail roughly 40% of Chapter 13 cases according to U.S. Courts data.

Priority Claims Must Be Paid in Full First

The order in which your payment gets distributed reveals why some debts disappear while others don’t. Priority claims go first-recent tax debts within three years of filing, child support arrears, and alimony obligations must be paid in full through your plan before unsecured creditors see a dime. Next come secured debts like your mortgage and car loan, which receive enough to keep the collateral protected and bring you current on missed payments. Only what remains flows to unsecured creditors like credit card companies and medical providers, which explains why they typically recover just 10 to 30% of what you owe according to U.S. Courts research.

How Your Payment Splits Across Different Debt Types

If your plan pays $1,800 monthly and $1,500 goes to your mortgage arrears and current payments plus $200 to child support, only $100 reaches credit card companies. This structure means you’re not spreading your money equally across all debts-the law prioritizes keeping your home and meeting family obligations. The distribution happens automatically through the trustee, who handles all calculations and sends payments to creditors on your behalf.

Preventing Payment Failures Through Automation and Communication

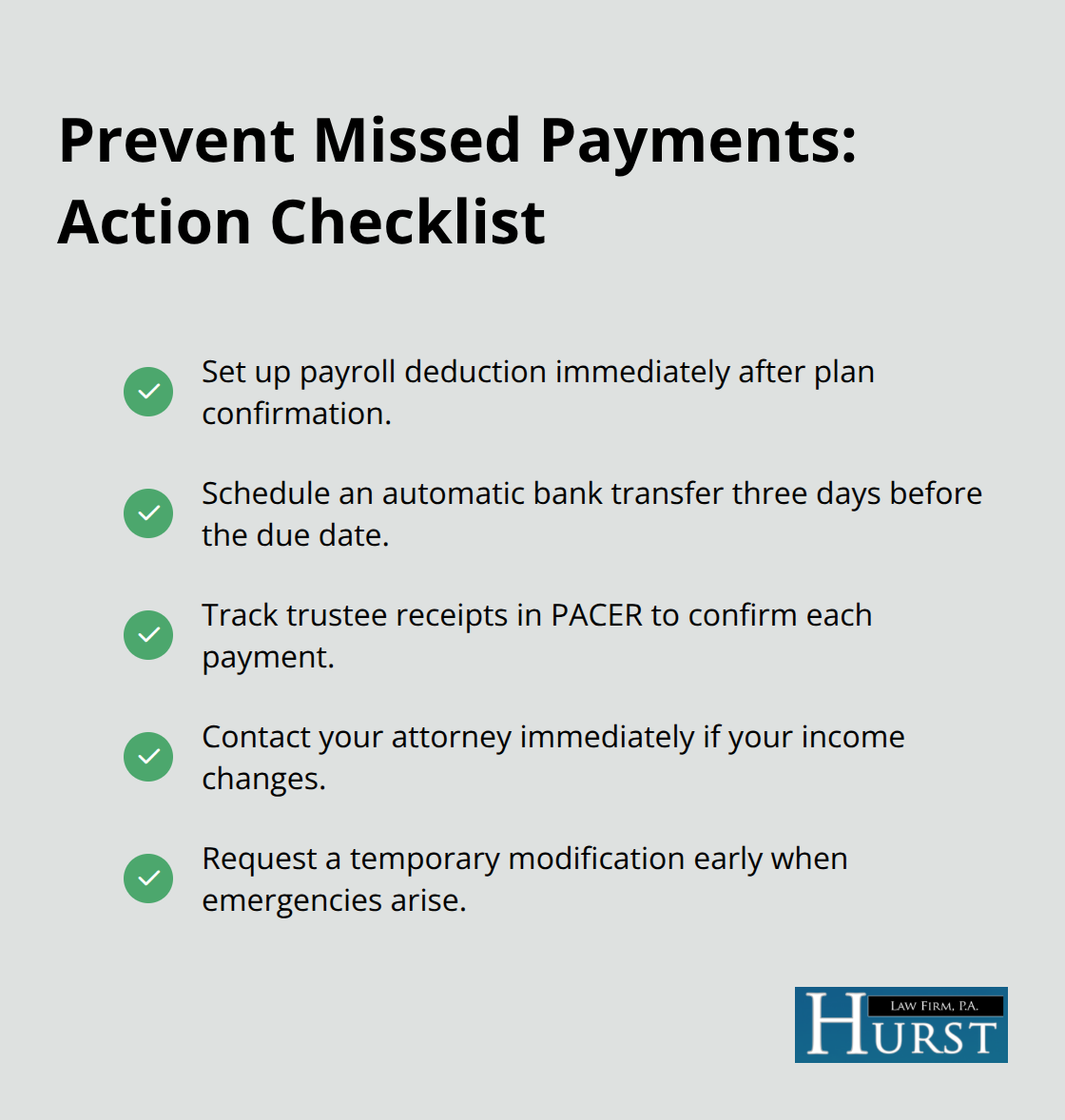

Setting up automatic payroll deduction three days before your payment due date virtually eliminates missed payments, the single biggest threat to plan completion. If your financial situation changes, contact your attorney immediately rather than skipping payments; courts favor proactive modifications over dismissals. When income drops or unexpected expenses arise (medical emergencies, job loss, major repairs), a plan modification keeps you on track instead of triggering dismissal and reopening you to foreclosure and wage garnishment.

Managing Your Chapter 13 Plan Payments in Memphis TN

Set Up Automatic Payments to Prevent Dismissal

Automatic payroll deduction stands as the single most effective tool to prevent plan failure, and you should set it up immediately after your plan receives confirmation. The court-appointed trustee handles the entire process, pulling your payment directly from your paycheck before you see the money. This approach works because it removes the temptation to spend funds intended for the trustee and eliminates the possibility of forgetting a due date. According to U.S. Courts data, roughly 40% of Chapter 13 cases face dismissal before discharge, and the overwhelming majority fail because filers miss payments. Automatic deduction cuts through this problem entirely.

If automatic payroll deduction isn’t possible at your job, set up an automatic bank transfer three days before your payment due date to a separate savings account dedicated solely to trustee payments. This creates a physical barrier between your living money and your plan obligation. Monitor your payment history through PACER (the Public Access to Court Electronic Records system), which shows exactly what the trustee has received and when. Missing even one payment puts your plan at risk, but missing three consecutive payments triggers automatic dismissal and lifts the automatic stay that protects you from foreclosure and wage garnishment.

Contact Your Attorney When Income Changes

When your financial situation changes, contact an attorney immediately rather than skipping payments or hoping things improve on their own. Courts strongly favor proactive plan modifications when income drops due to job loss, illness, or reduced hours. If your income rises during the plan, expect your monthly payment to increase accordingly, which means your attorney will need to file a modification showing the trustee your new income documentation.

One common mistake Memphis filers make is failing to report income changes promptly, which creates a gap between what you’re actually earning and what the trustee believes you earn. The trustee discovers this discrepancy during annual reviews or when creditors challenge your plan, which can result in forced dismissal rather than the modification you could have requested voluntarily. Modifications take time to process, so don’t wait until you’re desperate.

Address Financial Emergencies Proactively

If you anticipate a financial hiccup like a car repair or medical emergency, discuss it with your attorney before it becomes a payment problem. Requesting a temporary modification or payment adjustment early shows the trustee and court that you’re committed to the repayment plan, not trying to escape it. This proactive approach prevents the payment failures that derail most Chapter 13 cases and keeps your home and vehicle protected under the plan’s structure.

Final Thoughts

A Chapter 13 repayment plan provides a structured path forward when debt feels overwhelming. The system works because it rests on realistic numbers, not wishful thinking-your monthly payment reflects what you actually earn minus what you genuinely spend, distributed according to legal priorities that protect your home and vehicle while addressing your debts systematically. Success hinges on two factors: accurate budgeting from the start and consistent communication with your trustee when circumstances change.

Roughly 40% of Chapter 13 cases fail because filers either underestimate their living costs or miss payments without seeking modifications. You can avoid this outcome by auditing your actual spending before filing, setting up automatic payments immediately after confirmation, and contacting your attorney the moment your financial situation shifts. These practical steps keep your plan intact and your assets protected throughout the repayment period.

We at Hurst Law Firm, P.A. have guided Memphis residents through Chapter 13 since 1997, helping families understand their payment obligations and build sustainable repayment strategies. If you’re considering whether a Chapter 13 repayment plan fits your situation, contact us to discuss your specific circumstances and explore your options for a fresh start.