Chapter 13 bankruptcy offers a structured way to repay your debts while keeping your assets. The right plan depends entirely on your income, expenses, and financial goals.

We at Hurst Law Firm, P.A. help Memphis TN residents understand which Chapter 13 bankruptcy options work best for their specific budget. This guide walks you through the key factors that shape your repayment path.

How Chapter 13 Bankruptcy Works in Memphis TN

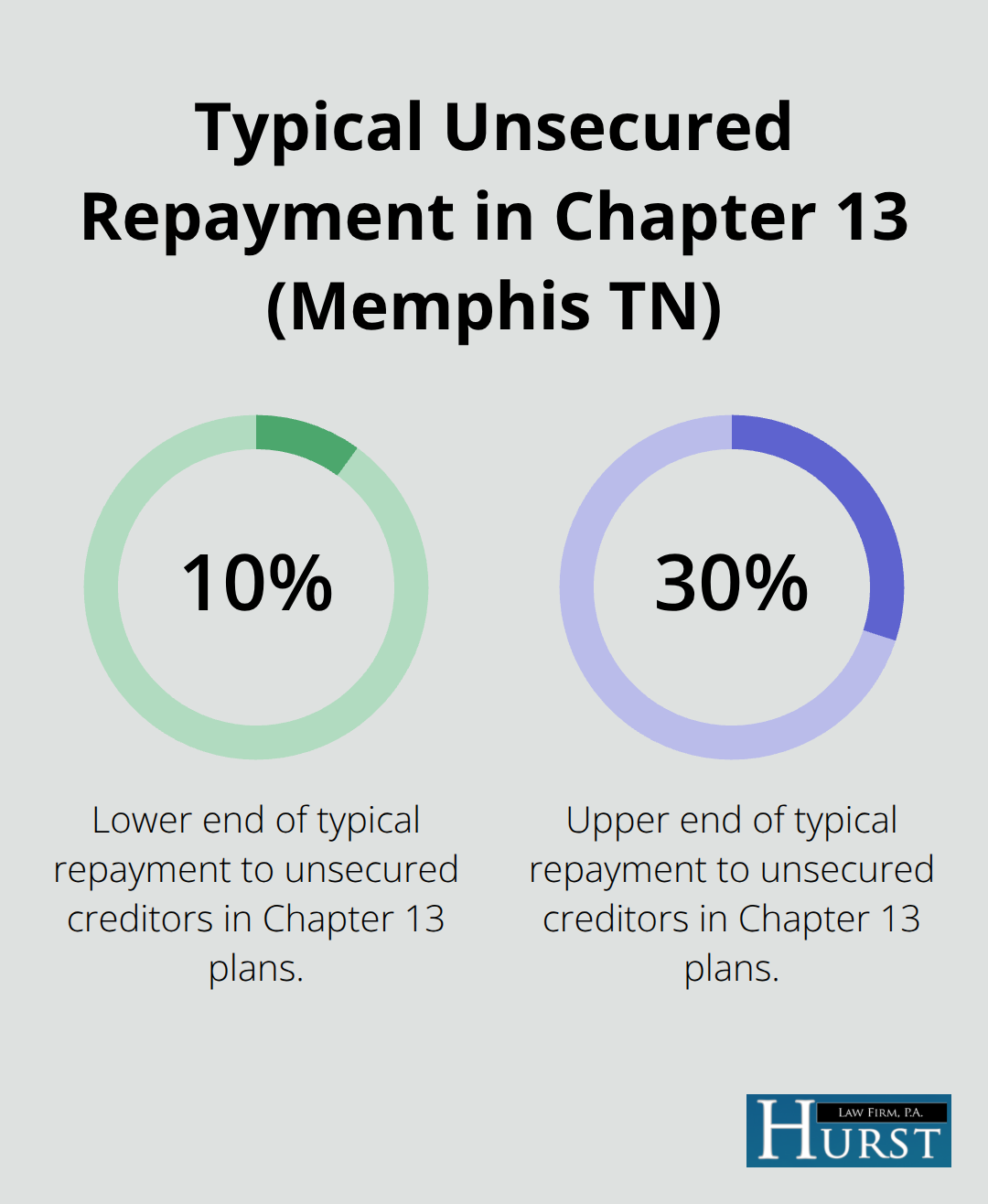

Chapter 13 bankruptcy in Memphis TN operates through a court-supervised repayment plan that typically runs three to five years. The length depends on whether your household income falls above or below Tennessee’s median income for your family size. You make one monthly payment to a court-appointed trustee, who distributes the funds to your creditors according to a plan the court approves. The trustee follows strict priority rules: first paying priority claims like recent tax debts and child support, then secured debts, and finally unsecured debts like credit cards. This structure means unsecured creditors often receive only 10 to 30 percent of what you owe, with the remainder discharged when you complete the plan. The automatic stay takes effect immediately upon filing, stopping wage garnishment, foreclosures, and collection calls while you work through your repayment period.

What determines your monthly payment amount

The Tennessee Means Test calculates your disposable income, which directly determines how much you pay monthly. This test compares your gross household income against the state’s median for your family size, then subtracts allowable living expenses based on IRS Collection Financial Standards. The IRS standards for food, housing, utilities, transportation, and health care often underestimate real costs in Memphis; a family of four might have a grocery allowance of $1,200 monthly according to IRS standards, but actual grocery costs frequently reach $1,600 to $1,800. Pull three months of bank and credit card statements to audit your actual spending and create a realistic budget. Your plan payment equals whichever is highest: your minimum secured debt payments, what unsecured creditors would receive in a Chapter 7 liquidation, or your calculated disposable income. Plan payments should leave at least $200 monthly as a cushion; anything less makes the plan fragile and more likely to fail.

Building reliable payment systems

The trustee supervises your entire repayment plan, verifying that you have sufficient income to fund payments and that you filed in good faith. You must attend a meeting of creditors within 21 to 50 days after filing, then attend a confirmation hearing within about 45 days after that meeting where the court approves your plan. Missing three consecutive payments can trigger dismissal, which lifts the automatic stay and reopens you to foreclosure and wage garnishment. U.S. Courts data show roughly 40 percent of Chapter 13 cases are dismissed before completion, primarily due to failure to maintain consistent monthly payments. Use automatic payroll deductions or automatic bank transfers to the trustee if possible to build reliable payment systems. Track all payments through PACER, the federal court’s public database, to verify your trustee received each payment. If your income or expenses change significantly (job loss or medical issues), contact an attorney early to request a plan modification; this window often closes after confirmation, leaving you vulnerable to dismissal.

Handling plan modifications and income changes

Life circumstances shift, and your Chapter 13 plan can shift with them. Income reductions or unexpected expenses may require you to modify your plan before the court finalizes it. The modification window closes after confirmation, so addressing changes early prevents dismissal and protects your assets. An attorney can help you file a modification request that adjusts your monthly payment to reflect your current financial reality. This proactive approach keeps your plan sustainable and reduces the risk of joining the 40 percent of cases that fail before completion.

Does Your Income Determine Your Plan Length?

Income thresholds and plan duration

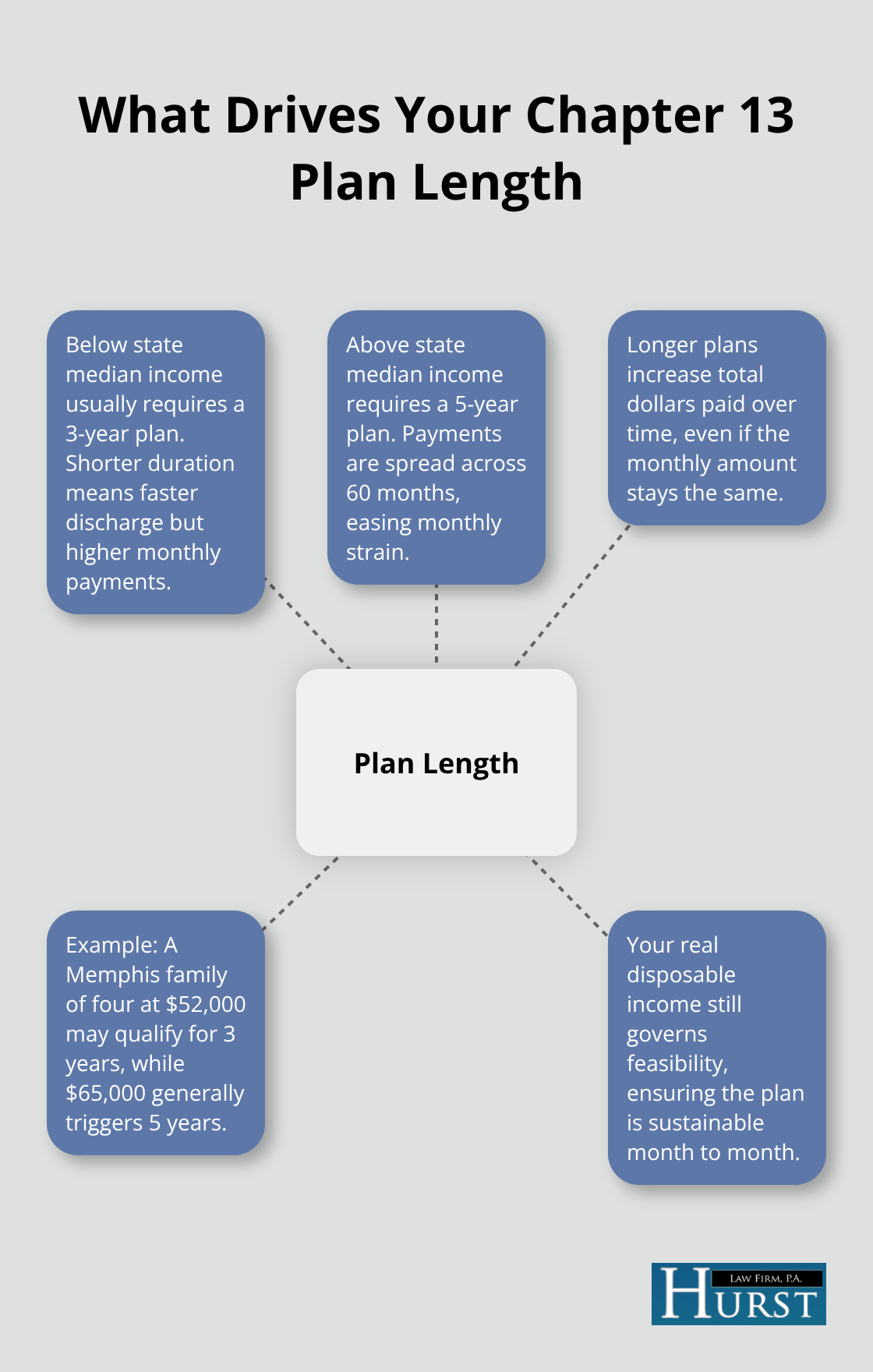

Your household income and how it compares to Tennessee’s median directly controls whether you pay for three or five years. If your income falls below the state median for your family size, your plan runs three years, which means higher monthly payments but faster debt relief. If your income exceeds the median, you must propose a five-year plan, stretching payments across 60 months instead of 36. This distinction matters because the longer your plan runs, the more total money you send the trustee, even if monthly payments stay identical.

A family of four in Memphis earning $52,000 annually might qualify for three years, while one earning $65,000 faces the five-year requirement.

How the means test calculates your threshold

The Tennessee Means Test calculates this threshold by taking your gross household income and subtracting allowable expenses using IRS Collection Financial Standards. However, those standards often underestimate real Memphis living costs. Food allowances sit around $1,200 monthly per the IRS, yet actual grocery expenses for a family of four typically run $1,600 to $1,800. This gap means your true disposable income may be lower than the calculation suggests, giving you stronger grounds to propose lower payments.

Secured versus unsecured debt priorities

Your secured and unsecured debt split also reshapes which plan length works for your situation. Secured debts like mortgages and car loans have priority in the repayment hierarchy, so you must commit enough monthly income to cover these payments first, then whatever remains goes to unsecured creditors like credit cards and medical bills. If you owe $18,000 on a car purchased more than 910 days before filing, Chapter 13 lets you cramdown that loan to the vehicle’s actual market value, potentially saving thousands. That reduced amount becomes your secured debt obligation within the plan.

Calculating what unsecured creditors actually receive

Unsecured creditors typically recover only 10 to 30 percent of what you owe across either plan length, so extending to five years doesn’t necessarily mean they receive significantly more. What matters is your disposable income after covering housing, utilities, food, transportation, and health care. Pull three months of bank and credit card statements to calculate your actual monthly expenses, not the IRS estimate. If your real spending leaves only $150 monthly after secured debts, a three-year plan becomes mathematically impossible because the payments would be too high to sustain. Conversely, if you have $400 monthly available, both plan lengths become feasible, and you should choose three years to finish faster and recover your financial footing sooner.

Moving forward with plan selection

The choice between three and five years ultimately rests on your actual monthly surplus after all legitimate expenses. Your income level sets the initial framework, but your real spending patterns determine whether that plan stays sustainable throughout the repayment period. Understanding this relationship helps you propose a realistic plan that the court will approve and that you can actually maintain without dismissal.

Evaluating Your Chapter 13 Options

Gather Your Financial Documents

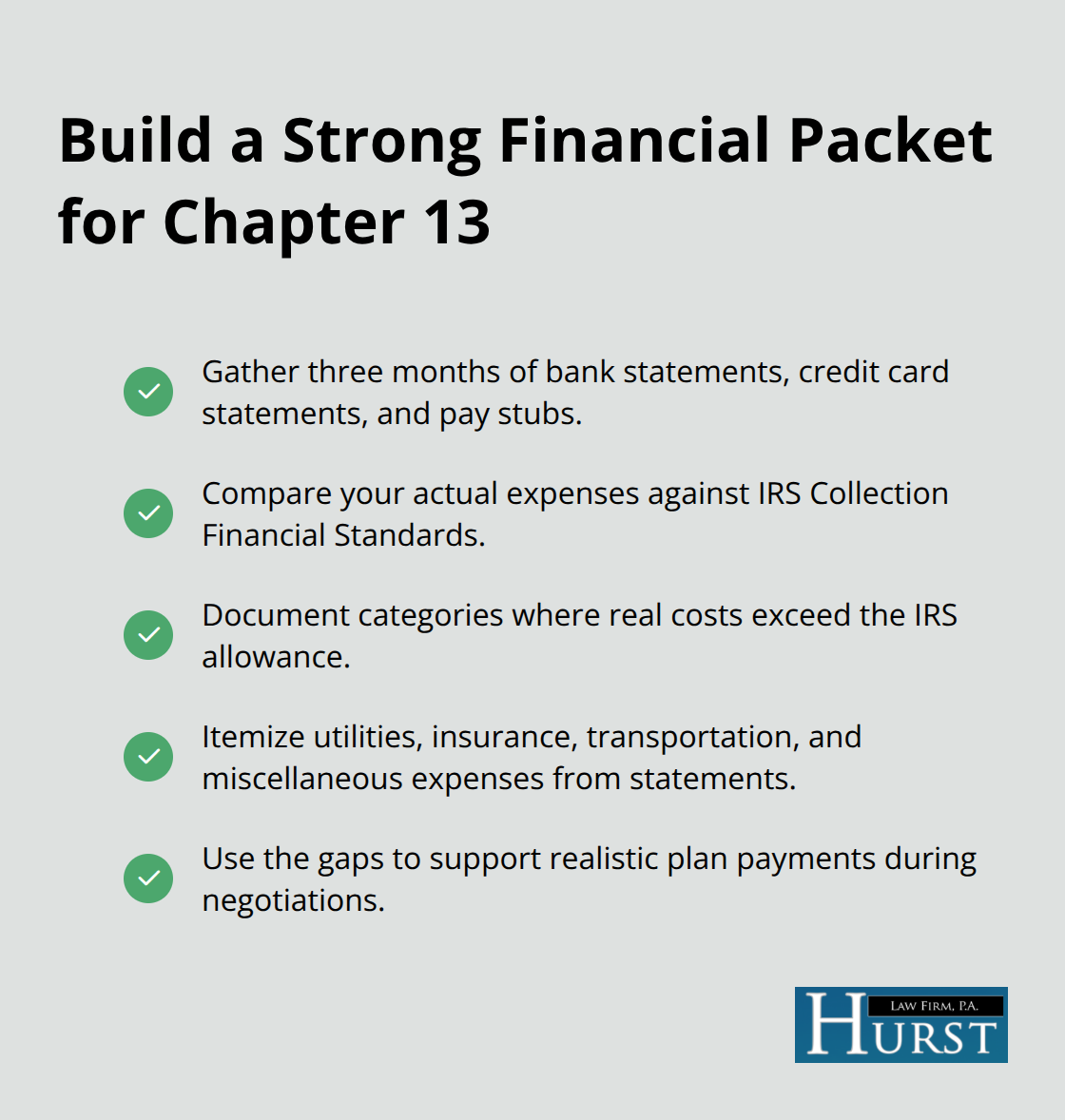

Start with three months of recent bank statements, credit card statements, and pay stubs. This foundation reveals your actual spending patterns, not theoretical estimates. The IRS Collection Financial Standards underestimate real costs in Memphis-food allowances sit around $1,200 monthly, but families of four typically spend $1,600 to $1,800 on groceries.

Your credit card statements show exactly where money flows each month for utilities, insurance, transportation, and miscellaneous expenses. Compare these real numbers against the IRS standards to identify where your actual costs exceed the allowance. This gap strengthens your position during plan negotiations because courts recognize that Memphis living costs outpace national averages.

Calculate Your Disposable Income

Calculate your total monthly income from all sources, then subtract your legitimate living expenses using your documented statements, not estimates. The remainder is your disposable income, and this number determines whether a three-year or five-year plan becomes feasible. If you have $250 monthly after all expenses, a three-year plan requires payments of approximately $7 per dollar of unsecured debt you propose to repay. A five-year plan stretches this to roughly $4.20 per dollar, making it more manageable if your surplus is tight. Many Memphis residents discover their actual disposable income falls below what the means test calculation suggests, which means you can propose lower monthly payments than the initial framework indicates.

Organize Your Debt Categories

Organize your debt list by category: secured debts like mortgages and car loans, priority debts like recent tax obligations and child support, and unsecured debts like credit cards and medical bills. For vehicles financed more than 910 days before filing, calculate the current market value and note the loan balance-this gap represents your cramdown savings. A vehicle worth $12,000 with a $21,000 loan balance means you could potentially pay only $12,000 through the plan and own the vehicle free and clear at completion. Mortgage arrears also matter; if you fall behind on your home payment, the plan allows you to catch up those past-due amounts over the repayment period while continuing regular monthly payments to your lender.

Identify Debts That Survive the Plan

Contact an attorney to review whether cramdowns apply to your specific debts and to calculate realistic plan payments based on your actual financial documents. An attorney can identify which debts discharge at plan completion and which ones survive, particularly student loans and recent tax obligations that almost never discharge. This clarity prevents surprises after you invest years in repayment and discover that certain debts remain. Understanding your debt structure upfront allows you to make informed decisions about plan length and monthly payment amounts that fit your actual financial situation.

Final Thoughts

Chapter 13 bankruptcy offers flexible repayment options for different budgets because the plan structure adapts to your actual income and expenses rather than forcing you into a one-size-fits-all approach. Whether you qualify for a three-year or five-year plan, whether you can cramdown a vehicle loan or catch up mortgage arrears, the framework adjusts to match your financial reality. The key is honest budgeting from the start, using your real bank statements instead of theoretical expense estimates, and building reliable payment systems that keep you current with the trustee month after month.

We at Hurst Law Firm, P.A. help Memphis TN residents navigate Chapter 13 bankruptcy options by examining your specific financial documents and calculating which plan structure actually works for your situation. Our role is to translate the means test calculations and IRS standards into real numbers based on your actual spending patterns, helping you understand whether three years or five years makes sense and how to structure payments that you can sustain without triggering dismissal.

The 40 percent dismissal rate for Chapter 13 cases reflects what happens when plans are built on estimates rather than documented reality. You avoid that outcome by taking action now, gathering your financial statements, and working with an attorney who understands Memphis bankruptcy law. Contact us to review your specific situation and determine which Chapter 13 bankruptcy options fit your budget and financial goals.