Chapter 13 bankruptcy offers a structured path to manage debt, but not everyone qualifies. Understanding Chapter 13 eligibility in Tennessee requires knowing specific income thresholds, debt limits, and other requirements that determine whether this option works for your situation.

We at Hurst Law Firm, P.A. help people navigate these eligibility rules every day. This guide walks you through the exact criteria you need to meet.

Income Thresholds That Determine Your Chapter 13 Plan Length

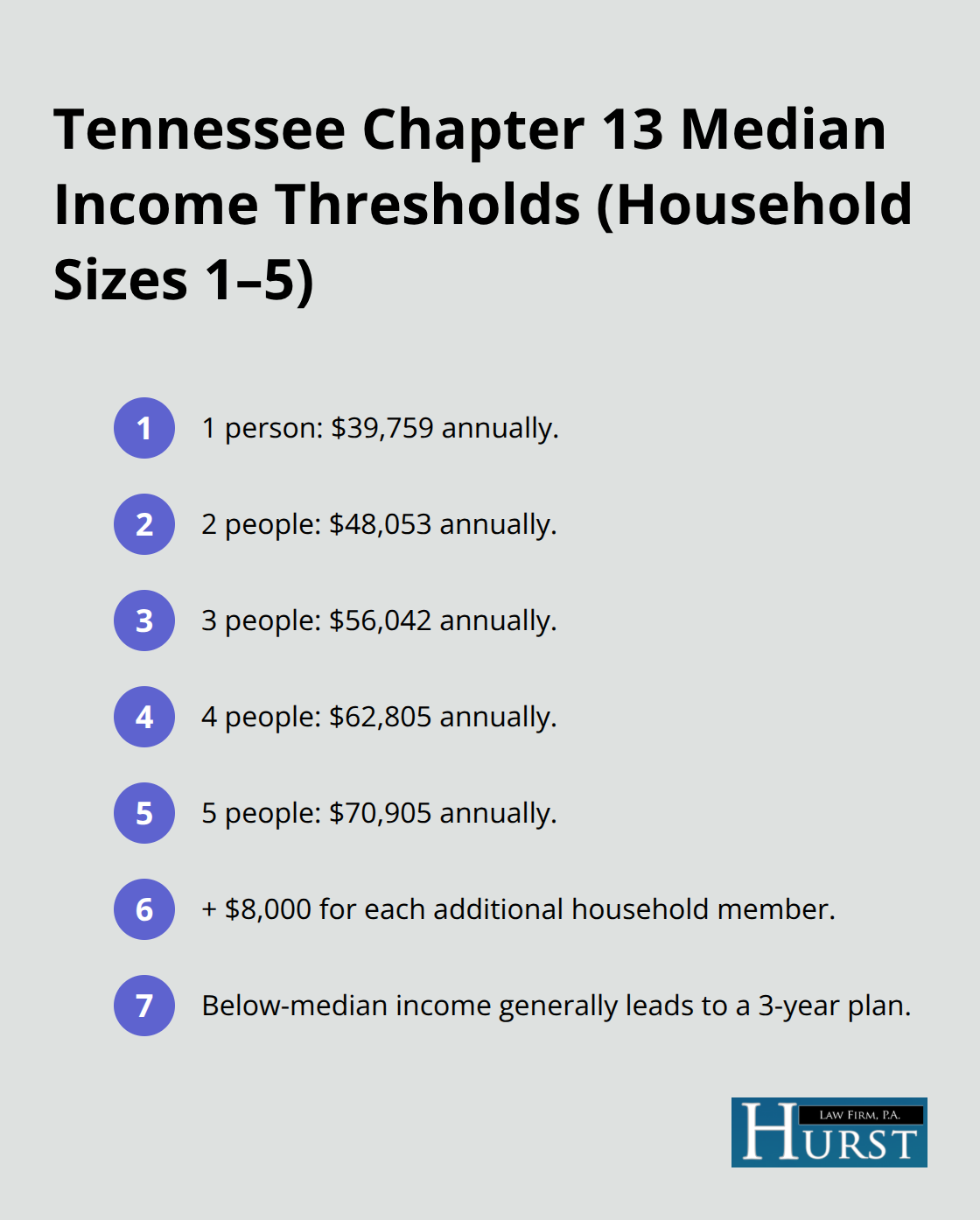

Your income forms the foundation of Chapter 13 eligibility in Tennessee. The means test uses your household income to determine two critical things: whether you qualify at all, and if you do, whether your plan runs three or five years. The U.S. Trustee Program publishes Tennessee median income thresholds for different household sizes. For a single person, the median is $39,759 annually. A two-person household sits at $48,053, three people at $56,042, four at $62,805, and five at $70,905. These numbers climb by roughly $8,000 for each additional household member. If your annual income falls below your household size’s median, you pass the first hurdle and likely qualify for Chapter 13 with a three-year repayment plan.

If your income exceeds the median, you enter a five-year plan instead, and the means test becomes more complex because creditors expect you to repay more of your debt over the longer period.

How the Means Test Calculates Your Actual Income

The means test averages your current monthly income over the last six calendar months, then multiplies that figure by 12 to arrive at your annual income. This matters because if your income recently dropped-say you lost a job or reduced hours-waiting one or two months could push you under the median and dramatically improve your Chapter 13 position. Income includes almost all sources: wages, business income, rental income, interest and dividends, pension and retirement plan distributions, and even amounts others pay for your household expenses. Once you calculate this six-month average, compare it directly to the Tennessee median for your household size. The calculation is straightforward, but accuracy matters because every dollar counts toward whether you land in the three-year or five-year category. If you’re borderline, reviewing your last six months of pay stubs and bank statements gives you the exact picture before filing.

What Happens When Your Income Exceeds the Median

Exceeding the Tennessee median income does not disqualify you from Chapter 13. Instead, it triggers the full means test calculation, which determines how much disposable income you have available for the plan. Disposable income equals your monthly income minus reasonably necessary expenses and minus charitable contributions up to 15 percent of gross income. The IRS and U.S. Trustee Program provide standardized expense allowances for housing, utilities, food, transportation, and other categories. These standards vary by county within Tennessee, so your allowed expenses in Shelby County differ from those in Davidson County. After you subtract these allowed expenses from your income, whatever remains is disposable income that must flow into your five-year repayment plan. If your disposable income is substantial, creditors expect you to repay a larger portion of your debts. The trustee administers your plan and distributes these payments to creditors according to priority rules, with unsecured creditors receiving at least as much as they would under Chapter 7 liquidation.

Debt Limits Shape Your Chapter 13 Eligibility

Beyond income, the law sets strict debt limits for Chapter 13 eligibility. Your unsecured debts (credit cards, medical bills, personal loans) must not exceed $526,700, and your secured debts (mortgages, car loans) must not exceed $1,580,125. These thresholds apply as of your filing date. Most Tennessee filers stay well below these caps, but if you carry significant secured debt from multiple properties or large business loans, you need to verify your totals before filing. The trustee calculates your total debt from the schedules you file with the court, so accuracy in listing every creditor and balance matters. If your debts exceed these limits, Chapter 13 becomes unavailable, and Chapter 7 liquidation or other options become your focus instead.

Debt Limits and Types of Debt Eligible for Chapter 13

Federal Caps on Unsecured and Secured Debt

The federal government sets strict limits on how much debt you can carry and still file Chapter 13 in Tennessee. Your unsecured debts-credit cards, medical bills, personal loans, and payday loans-cannot exceed $419,275 as of your filing date. Your secured debts-mortgages, car loans, and equipment financing-cannot exceed $1,257,850. These limits prevent Chapter 13 from becoming a tool for large commercial debtors. Most Tennessee filers stay comfortably under these thresholds, but if you own multiple properties with mortgages or carry substantial business debt, you need to calculate your exact totals before meeting with an attorney.

The trustee verifies every debt you list on your schedules, so accuracy matters from the start. If your unsecured debts hit $419,276 even by one dollar, you lose Chapter 13 eligibility entirely. Similarly, if secured debts exceed the cap, Chapter 13 becomes unavailable. Pull your credit report and gather statements from every lender to get accurate numbers. This step determines whether Chapter 13 is even an option for your situation.

How the Trustee Treats Different Debt Categories

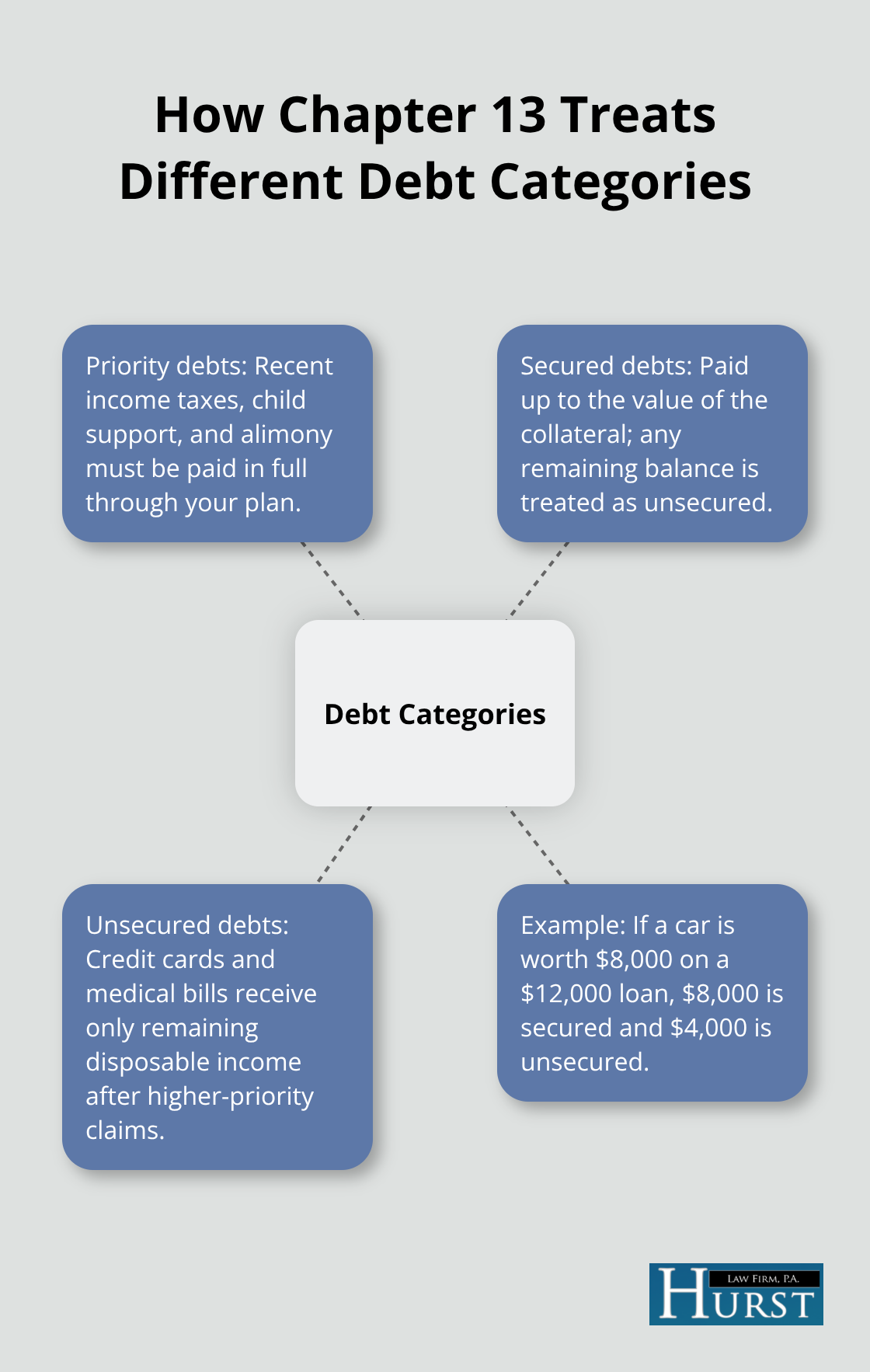

The types of debt you include in your Chapter 13 repayment plan fall into three categories that the trustee treats differently. Priority debts-recent income taxes, child support, and alimony-must be paid in full through your plan regardless of disposable income. Secured debts tied to collateral like your home or car are paid to the extent of the collateral’s value. If your car is worth $8,000 but you owe $12,000, only $8,000 is treated as secured and the remaining $4,000 becomes unsecured debt.

Unsecured debts like credit cards and medical bills receive whatever disposable income remains after priority and secured claims are paid.

Debts That Survive Your Discharge

Some debts cannot be discharged even after you complete your plan: long-term mortgages, student loans (with rare exceptions), criminal fines, and debts incurred through fraud stay with you. However, most consumer debts-credit card balances, medical debt accumulated from hospital bills, personal loans, and certain tax debt-can be consolidated and repaid through your three- or five-year plan. The key is listing every creditor accurately on your filing documents. Missing a creditor can result in that debt surviving your discharge, leaving you liable after the plan ends.

Understanding these debt categories and limits shapes your entire Chapter 13 strategy. Once you confirm your debts fall within the federal caps and you know which debts will be discharged, you can move forward to the other eligibility requirements that determine whether you can actually execute a successful repayment plan.

Key Eligibility Factors Beyond Income and Debt

Regular Income Requirements for Chapter 13 Success

You need a regular source of income to file Chapter 13 in Tennessee, and this requirement excludes you from the option if you lack steady earnings. The U.S. Trustee Program requires that you demonstrate ongoing income from employment, a business, rental property, pension distributions, retirement account withdrawals, or amounts others contribute toward your household expenses. If you lost your job last month and have no income lined up, Chapter 13 will not work for you right now. The trustee needs confidence that you can make monthly plan payments for the next three to five years without interruption.

Self-employed individuals and business owners qualify as long as their income is stable and documented through tax returns and financial records. The trustee will examine your last two years of tax returns to verify your income pattern, so inconsistent or declining earnings may require explanation. If your income is seasonal (you earn most of your money during certain months), the means test calculation accounts for this by averaging your income over the full six-month period, smoothing out the peaks and valleys.

Previous Bankruptcy Filings and Timing Restrictions

Previous bankruptcy filings create timing restrictions that block you from filing Chapter 13 in certain situations. If you filed Chapter 7 and received a discharge within the past eight years, you cannot file Chapter 13. If you filed Chapter 13 and received a discharge within the past six years, you cannot file another Chapter 13. The Bankruptcy Code also prohibits filing if a prior bankruptcy was dismissed within 180 days because you failed to appear in court or refused to comply with court orders, or if creditors obtained relief from the automatic stay.

These restrictions exist to prevent serial filings and abuse of the bankruptcy system. If you fall into one of these categories, waiting out the required period is your only path forward.

Credit Counseling and Financial Management Course Requirements

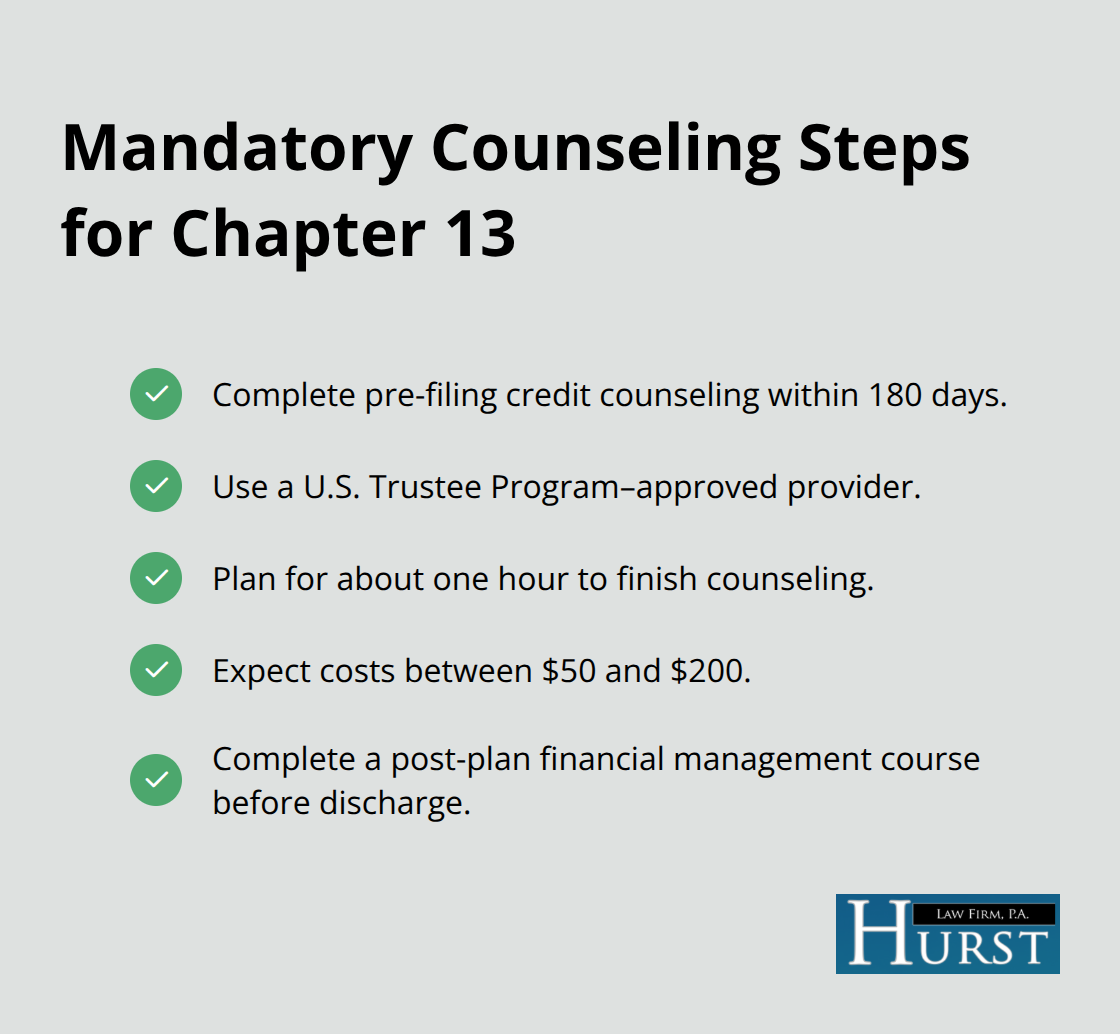

Credit counseling and a financial management course are mandatory, not optional. You must complete credit counseling from an agency approved by the U.S. Trustee Program within 180 days before filing your petition. This counseling costs between $50 and $200 and takes about an hour. After you complete your Chapter 13 plan, you must finish a financial management course through another approved provider before discharge is granted.

These requirements ensure you understand your financial situation and develop better money management habits going forward. The U.S. Trustee Program maintains a searchable list of approved providers in Tennessee, so you can schedule these sessions before meeting with an attorney or after filing, depending on your timeline.

Final Thoughts

Chapter 13 eligibility Tennessee depends on three core requirements: your income must fall within federal thresholds, your debts must stay below the statutory caps, and you must demonstrate the ability to fund a repayment plan. If your household income exceeds the Tennessee median for your size, you enter a five-year plan with disposable income flowing toward creditors. Your unsecured debts cannot exceed $526,700 and secured debts cannot exceed $1,580,125.

Meeting these requirements opens the door to Chapter 13, but qualification is only the first step. Once you confirm you meet the thresholds, you face the practical work of gathering documentation, calculating your exact disposable income, and building a realistic repayment plan that creditors will accept. The trustee will scrutinize your income calculations, expense allowances, and debt listings, so accuracy from the beginning prevents delays and complications later.

We at Hurst Law Firm, P.A. help Memphis residents determine their Chapter 13 eligibility and guide them through the entire filing process. Contact Hurst Law Firm, P.A. at 901-730-4958 or visit our Memphis office at 44 North Second Street, Suite 403 to take the next step toward financial recovery.