Facing foreclosure in Memphis, TN can feel overwhelming, but you have more options than you might realize. We at Hurst Law Firm, P.A. help homeowners understand the foreclosure relief options available to them before it’s too late.

The right strategy can stop the process, modify your loan, or help you move forward with stability. This guide walks you through your legal protections and practical steps to regain control.

What Foreclosure Means and Your Timeline in Tennessee

How Foreclosure Works in Memphis

Foreclosure in Memphis, TN doesn’t happen overnight, and understanding the process is your first defense. In Tennessee, lenders must follow specific legal steps before they can take your home. The process typically begins when you miss mortgage payments, and your lender sends a notice of default. From that point, you generally have several months before a foreclosure sale occurs, though the exact timeline depends on your loan terms and whether your lender pursues judicial or non-judicial foreclosure. Tennessee allows both types, and judicial foreclosure-where the lender files in court-is more common in our state. This court process takes time, usually three to six months minimum, giving you a window to act. Non-judicial foreclosure moves faster but is less common for traditional mortgages.

Why Your Timeline Matters

The moment you receive a default notice, your clock starts ticking, and waiting makes your options disappear. Many homeowners lose their homes simply because they don’t understand they have time to respond. Acting within the first 30 to 60 days after receiving notice opens doors that close later. Your lender may be willing to negotiate, modify your loan, or work out a forbearance agreement during this window. Delay eliminates these possibilities and forces you toward foreclosure sale or bankruptcy as your only remaining options.

Your Legal Right to Stop the Process

Tennessee law gives you specific protections during foreclosure, and knowing them matters. Once a foreclosure lawsuit is filed, you have the right to respond in court and contest the foreclosure if the lender failed to follow proper procedures or if you have a valid defense. You also have the right to request a loan modification from your lender before the sale happens-lenders must consider your request if you meet basic criteria. The U.S. Department of Veterans Affairs offers specific guidance for veterans facing foreclosure, and programs like those offered by the Tennessee Housing Development Agency provide counseling and hardship refinance options designed specifically for Memphis homeowners.

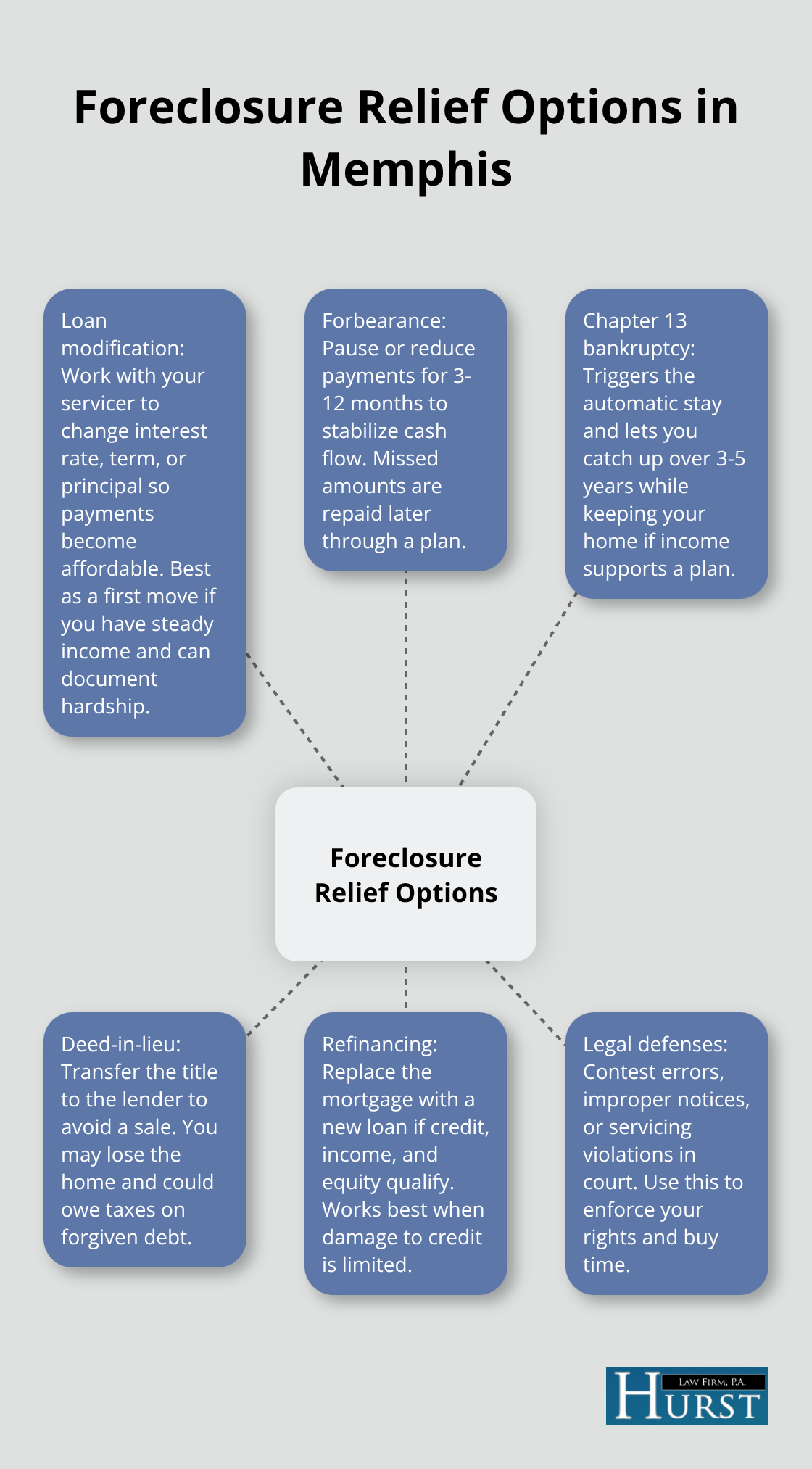

Bankruptcy as a Foreclosure Defense

Filing for bankruptcy triggers an automatic stay that immediately halts foreclosure proceedings. Chapter 13 bankruptcy is particularly powerful for homeowners because it allows you to catch up on missed payments through a repayment plan while keeping your home (provided you have a steady income). This option transforms what feels like a losing battle into a structured path forward. Your missed payments become part of a three- to five-year plan, and your lender cannot proceed with foreclosure as long as you meet the plan terms.

Understanding these protections and timelines puts you in control rather than at the mercy of the foreclosure process. Your next step is to explore which relief option-loan modification, forbearance, bankruptcy, or another strategy-fits your specific situation and financial capacity.

Your Practical Foreclosure Relief Options

Loan Modification: Your Strongest First Move

Loan modification stands as your strongest first move when facing foreclosure in Memphis, TN. This option involves negotiating directly with your lender to change the terms of your existing mortgage, typically by lowering your interest rate, extending the loan term, or in some cases reducing the principal balance. The Tennessee Housing Development Agency offers hardship refinance programs specifically designed for Memphis homeowners in financial distress, and these programs can reduce your monthly payment by hundreds of dollars.

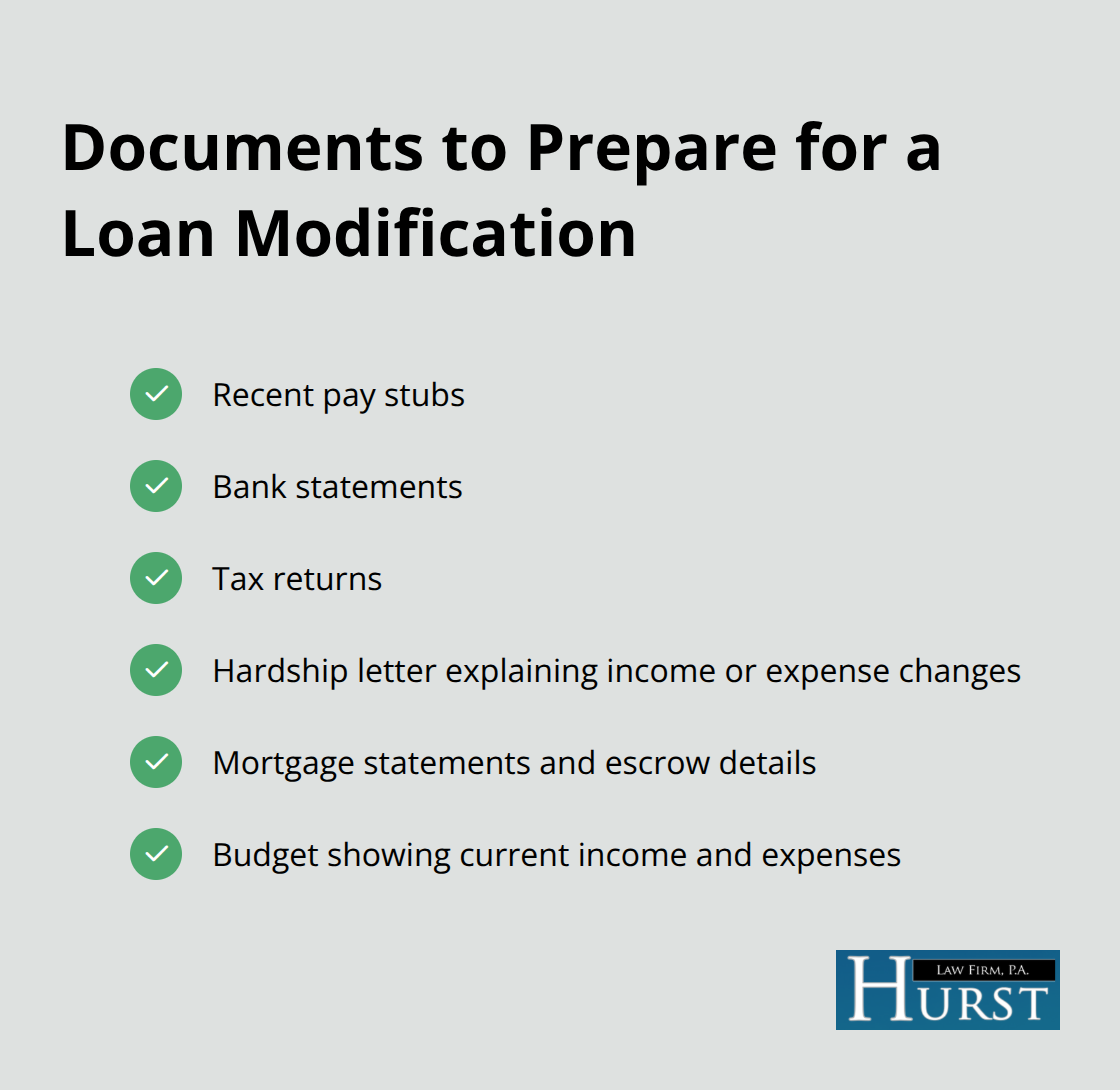

Before you apply, gather your recent pay stubs, bank statements, tax returns, and a written explanation of your hardship. Contact your mortgage servicer first-they often have in-house modification programs and must review your request if you qualify. The application process usually takes two to four weeks, though some cases stretch longer if an appraisal is needed.

Building Your Case While You Wait

While waiting for approval, continue making payments on your current mortgage if possible to demonstrate good faith and strengthen your case. Refinancing works differently and requires you to qualify for a new loan, which means your credit score and income matter more than in a modification. Refinancing typically works best if you still have equity in your home and your credit hasn’t been severely damaged.

If your lender denies modification, don’t accept that as final. Request a written explanation and consider consulting with a foreclosure attorney to review whether the denial was legally justified.

Forbearance and Deed-in-Lieu Alternatives

Forbearance agreements temporarily pause or reduce your monthly payments for a set period, usually three to twelve months, allowing you to stabilize your finances. After the forbearance period ends, you repay the missed amounts through a plan added to your regular mortgage. This works well if your hardship is temporary, such as job loss followed by reemployment.

Deed-in-lieu of foreclosure lets you transfer your home’s title directly to your lender in exchange for release from the mortgage obligation, avoiding a foreclosure sale that damages your credit more severely. However, this option means losing your home, and you may still owe taxes on forgiven debt. The Office of the Comptroller of the Currency warns homeowners to avoid upfront-fee foreclosure rescue scams, so never pay money to third parties claiming they can negotiate with your lender.

Comparing Your Options Against Bankruptcy

Chapter 13 bankruptcy often provides better protection and more time to resolve your situation while keeping your home. Compare all three options-modification, forbearance, and deed-in-lieu-against bankruptcy before you decide, since your choice determines whether you stay in your home or lose it. The path you select now shapes your financial future for years to come, making it worth the effort to understand each option fully before moving forward.

Rebuilding Credit and Stability After Foreclosure

How Foreclosure Impacts Your Credit Score

Foreclosure damages your credit score immediately, typically dropping it 130 to 200 points depending on your starting score. However, the damage isn’t permanent, and your score starts recovering the moment you stop missing payments. The first actionable step is obtaining your credit reports from all three bureaus-Equifax, Experian, and TransUnion-through annualcreditreport.com, which provides free reports yearly. Dispute any inaccuracies immediately, as errors suppress your score further.

Rebuilding Your Credit Through Consistent Payments

Establish a pattern of on-time payments starting now. Open a secured credit card if traditional cards reject you, deposit $300 to $500, and use it for small monthly purchases you pay off completely. This demonstrates reliability to lenders tracking your behavior. Within 12 to 24 months of consistent payments, your score typically climbs 100 to 150 points. Avoid the temptation to apply for multiple new credit accounts simultaneously-each application triggers a hard inquiry that temporarily lowers your score. Focus instead on becoming creditworthy through steady, predictable behavior rather than aggressive credit seeking. Rebuilding begins immediately when you demonstrate financial responsibility.

Finding Housing After Foreclosure

Most landlords now run credit checks, and a foreclosure appears on your report for seven years, but its impact weakens significantly after two years. Start your housing search at month 18 or 24 post-foreclosure rather than immediately, when your credit has started recovering and your story becomes less damaging. When applying for rentals, provide a written explanation of your foreclosure circumstances and emphasize what changed financially-whether you regained employment, reduced debt, or stabilized your income.

Offer a larger security deposit or first and last month’s rent upfront to demonstrate financial commitment. Some landlords prioritize stability over perfect credit history. Consider renting from smaller property owners rather than large management companies, as they often evaluate applications more flexibly.

Saving for Future Homeownership

Simultaneously, start saving for a future down payment by setting aside 10 to 15 percent of monthly income into a dedicated savings account. The Tennessee Housing Development Agency and similar programs offer down payment assistance for qualified buyers typically three to five years after foreclosure, so establishing savings discipline now positions you for homeownership again when you’re financially ready.

Creating Long-Term Financial Stability

Plan long-term financial stability by addressing the root cause of your foreclosure-whether insufficient income, unexpected medical expenses, job loss, or poor financial habits. If income was the problem, invest in skills training or education that increases earning potential. If expenses caused the crisis, create a written budget tracking every dollar and identify spending patterns to eliminate. Build an emergency fund containing three to six months of expenses, which prevents future financial emergencies from becoming foreclosure crises. This discipline matters more than any credit score in preventing another foreclosure.

Final Thoughts

Foreclosure relief options exist at every stage of the process, and you must identify which one matches your situation and financial capacity. Loan modification offers the fastest path if your lender cooperates and you can afford modified payments, while forbearance buys time if your hardship is temporary. Chapter 13 bankruptcy provides the strongest protection if you have steady income and want to stay in your home while catching up on missed payments through a manageable repayment plan.

Acting within the first 30 to 60 days after receiving a default notice opens doors that slam shut later. Delay eliminates negotiation possibilities and forces you toward foreclosure sale as your only remaining path. The Tennessee Housing Development Agency, HUD housing counselors, and local legal resources stand ready to guide you through these decisions.

We at Hurst Law Firm, P.A. help Memphis families navigate foreclosure and financial distress. Contact us to discuss which foreclosure relief option fits your circumstances, and take action today to determine whether you lose your home or regain control of your financial future.