Debt can feel overwhelming, especially when creditors won’t stop calling and your financial situation seems impossible to fix. Chapter 13 bankruptcy offers a structured path forward that many Memphis residents don’t realize is available to them.

At Hurst Law Firm, P.A., we help people understand their Memphis Chapter 13 options and find the right solution for their circumstances. This guide walks you through how Chapter 13 works, its real advantages, and how it compares to other debt relief strategies.

How Chapter 13 Bankruptcy Works in Memphis

Chapter 13 is a court-supervised repayment plan that typically lasts three to five years, and it differs fundamentally from simply negotiating with creditors on your own. When you file Chapter 13 in Memphis, the automatic stay takes effect immediately, which stops wage garnishments, foreclosure proceedings, and collection calls the moment your petition is filed. The trustee assigned to your case then oversees your repayment plan and distributes your monthly payments to creditors according to a priority structure: secured debts and priority debts first, followed by unsecured debts like credit cards. U.S. Courts data shows that roughly 40 percent of Chapter 13 cases face dismissal before completion, most often because people fail to maintain consistent monthly payments. This reality underscores why your plan must rest on actual numbers from your bank and credit card statements over three months, not theoretical budgets.

Building Your Plan on Real Numbers

Your monthly payment calculation uses the Tennessee Means Test, which takes your gross income and subtracts allowable living expenses based on IRS Collection Financial Standards. However, Memphis actual costs often exceed those standards significantly. For example, the IRS grocery allowance is roughly $1,200 per month for a family of four, but real Memphis families typically spend $1,600 to $1,800 monthly on groceries. This gap matters because it directly affects your disposable income and what you can realistically afford to pay each month. Your plan must cover your secured debt minimums (like mortgage and car payments), what unsecured creditors would receive if you filed Chapter 7 instead, or your calculated disposable income-whichever is highest. A cushion of at least $200 monthly improves your odds of completing the plan successfully and reduces dismissal risk.

How Plan Length Affects Your Obligations

The plan length depends on whether your household income falls below or above Tennessee’s median income for your family size. A Memphis family of four earning around $52,000 annually may qualify for a three-year plan, while one earning approximately $65,000 would need a five-year plan. Extending a plan from three to five years does not guarantee substantially more for unsecured creditors; the amount they receive depends on your disposable income after covering housing, utilities, food, transportation, and health care. Debts that often survive the plan include most student loans and recent tax obligations, so you should confirm which debts will discharge and which will remain.

Chapter 13 Versus Chapter 7 in Practice

Chapter 7 moves faster, typically discharging most debts in three to six months, while Chapter 13 requires you to commit to a multi-year repayment schedule. With Chapter 7, you must pass the Tennessee means test, and you cannot keep non-exempt assets; with Chapter 13, you keep everything-your home, your car, and all other property-as long as you make your plan payments. Chapter 7 offers no minimum debt requirement, but you must wait eight years before filing another Chapter 7 case. Chapter 13 has debt limits: secured debts cannot exceed $1,257,850 and unsecured debts cannot exceed $419,275 according to current bankruptcy code thresholds. If you fall behind on your mortgage or want to catch up on missed payments while keeping your home, Chapter 13 is the only option because Chapter 7 offers no mechanism to cure arrears. Similarly, if you financed your car more than 910 days before filing, Chapter 13 allows vehicle cramdown, which reduces the loan to your car’s actual market value and can save thousands of dollars. Chapter 13 also protects co-signers from collection actions if your plan pays in full, whereas Chapter 7 leaves co-signers liable unless they file bankruptcy themselves.

Who Can File Chapter 13 in Memphis

To file Chapter 13 in Memphis, you must have a regular source of income-employment, retirement benefits, dividends, or other stable income that can support a repayment plan. You cannot file if you are a stockbroker or commodity broker, as these professions are excluded from Chapter 13 eligibility. You must have filed all required tax returns for the past four years, and credit counseling from an approved agency is mandatory within 180 days before filing. Your secured debts must stay under $1,257,850 and unsecured debts under $419,275. These requirements exist because Chapter 13 is fundamentally about proving you can commit to a structured repayment plan, not about wiping out debts through liquidation. The financial documents you need-typically three months of bank statements, pay stubs, and a detailed breakdown of actual monthly expenses-determine whether Chapter 13 makes sense for your situation and whether you can sustain the plan payments without dismissal. Understanding these eligibility rules helps you assess whether Chapter 13 fits your circumstances before you move forward with filing.

Why Chapter 13 Protects Your Assets While Rebuilding Your Life

Keep Your Home, Car, and Personal Property

Chapter 13 allows you to retain your home, your car, and all other property as long as you make your monthly plan payments. This protection separates Chapter 13 fundamentally from Chapter 7, where you risk losing non-exempt assets to liquidation. In Memphis, where median home values have climbed steadily, keeping your primary residence matters enormously to your financial stability and family security. If you fall behind on your mortgage, Chapter 13 becomes your only bankruptcy option because it permits you to catch up on missed payments through the repayment plan while you continue making regular monthly payments to your lender. The trustee oversees this process, ensuring your arrears decline systematically over your plan period.

Vehicle Cramdown Saves Thousands

Chapter 13 offers vehicle cramdown if your car was financed more than 910 days before filing, which reduces the loan balance to your vehicle’s actual market value. A Memphis resident who owes $15,000 on a car worth $8,000 could reduce that debt obligation significantly through cramdown, saving thousands of dollars over the plan. This protection extends to other property as well: furniture, tools, equipment, and personal possessions that might be vulnerable in Chapter 7 remain yours throughout Chapter 13, provided you maintain your plan payments.

The Automatic Stay Stops Collection Actions Immediately

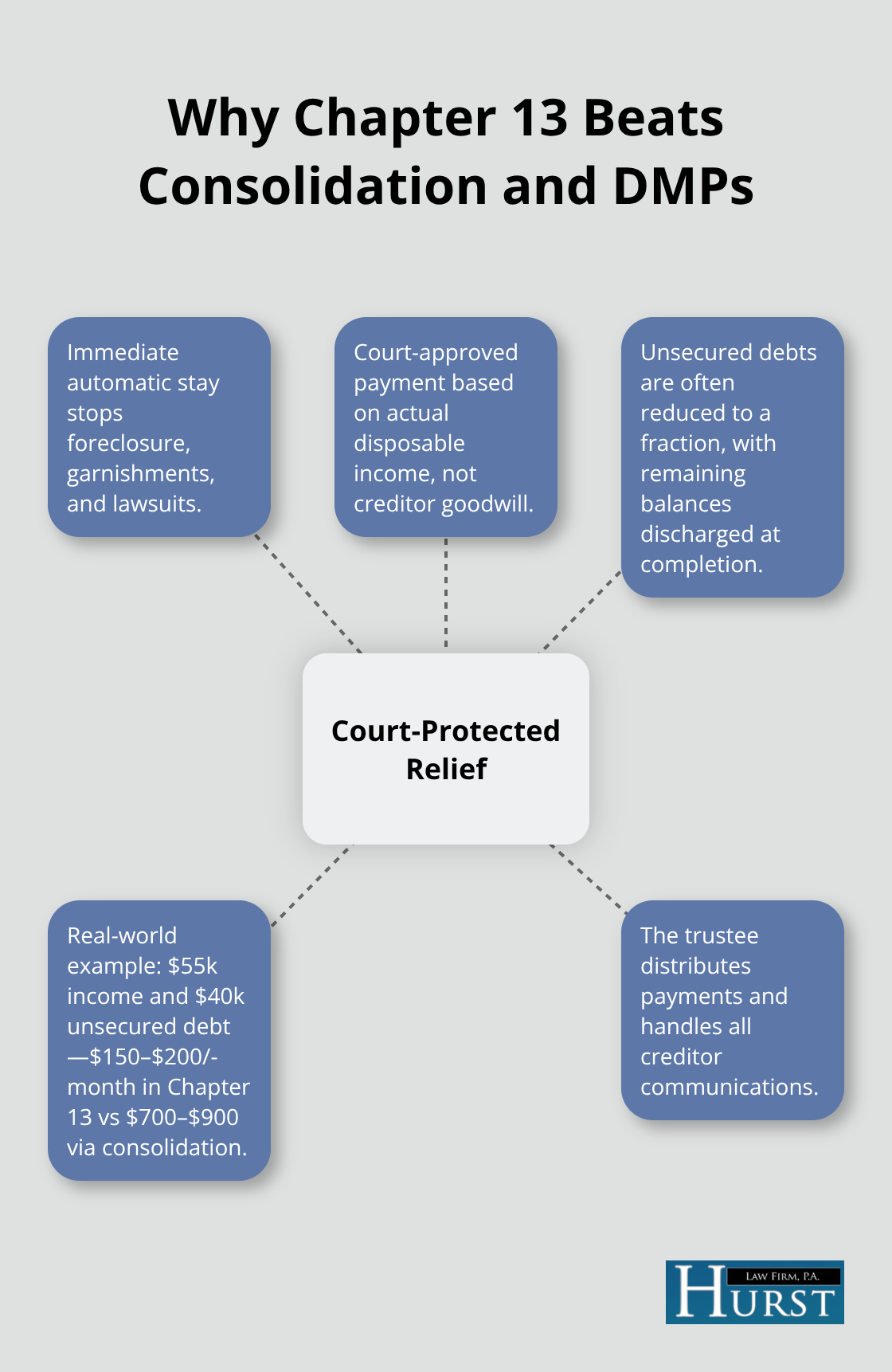

The automatic stay takes effect immediately upon filing your Chapter 13 petition, which halts foreclosure proceedings, repossession actions, and forced sales before they start. This court order gives you breathing room to stabilize your finances. The moment your petition is filed, creditors must stop calling, must cease wage garnishment, and must halt collection lawsuits against you. Wage garnishment in Tennessee can reduce your paycheck by up to 25 percent of your disposable income, which devastates household cash flow and makes it impossible to cover basic expenses. Stopping that garnishment immediately frees up hundreds of dollars monthly that you can redirect toward your plan payments and living expenses.

Rebuild Credit Through Consistent Payments

Collection calls typically increase in frequency and intensity as debts age, with some creditors calling multiple times per day. The automatic stay eliminates these calls entirely, removing the constant stress and anxiety that accompanies financial hardship. Your credit score will decline when you file Chapter 13, but rebuilding begins immediately because you make on-time payments to the trustee every month. After your plan completes and your remaining eligible debts discharge, you emerge with a clean slate and a demonstrated track record of meeting financial obligations for three to five years. That payment history becomes powerful evidence to future lenders that you have stabilized your finances and can be trusted again. Many Memphis residents report that their credit scores recover to the 650 to 700 range within two to three years after discharge, particularly if they address other credit report errors through the Fair Credit Reporting Act and add positive credit accounts like a secured credit card with modest limits. The discharge itself removes the psychological weight of overwhelming debt, which allows you to focus on career advancement, education, and genuine financial health rather than surviving month-to-month under constant creditor pressure.

Understanding how Chapter 13 protects your assets and rebuilds your financial reputation sets the stage for comparing it to other debt relief options available to Memphis residents.

Chapter 13 vs. Other Debt Relief Options in Memphis TN

How Debt Consolidation Falls Short

Debt consolidation and debt management plans flood the Memphis market as heavily advertised alternatives to bankruptcy, yet they solve fundamentally different problems than Chapter 13 and often leave you worse off financially. Debt consolidation shifts your existing debts to a new creditor, often at a lower interest rate initially, but you still owe the full amount borrowed plus ongoing fees that can total thousands of dollars over the life of the loan. A Memphis resident carrying $35,000 in credit card debt might consolidate into a personal loan at 12 percent interest over five years, paying roughly $844 monthly and $15,640 in total interest-money that flows into the lender’s pocket rather than reducing your actual debt burden.

Why Debt Management Plans Fail Most Often

Debt management plans operate through third-party agencies that negotiate with your creditors to lower interest rates or extend payment terms, but these plans require you to remain current on payments, offer no legal protection from creditors, and typically run three to five years while damaging your credit score almost as severely as bankruptcy. The Federal Trade Commission has documented numerous cases where debt settlement companies collected upfront fees without delivering promised results, leaving clients in worse financial positions than before. These plans collapse when income drops or unexpected expenses arise, leaving you vulnerable to collection calls and lawsuits that the plan never prevented.

Chapter 13 Provides Court Protection and Real Debt Reduction

Chapter 13 differs fundamentally because the automatic stay provides immediate court protection, your monthly payment is court-approved and based on actual disposable income rather than creditor goodwill, and unsecured debts like credit cards are typically reduced to 10 to 30 percent of what you owe with the remainder discharged upon plan completion. A Memphis family earning $55,000 annually with $40,000 in unsecured debt might pay only $150 to $200 monthly through Chapter 13 rather than $700 to $900 through consolidation, recovering genuine financial breathing room within weeks instead of years. The trustee collects your payment once monthly, distributes funds according to bankruptcy law, and handles all creditor communication so you never deal with collection calls again.

When Chapter 13 Makes Sense for Your Situation

Chapter 13 makes sense when you have regular income but cannot afford your debts under current terms, when you want to keep your home or car while addressing arrears, or when you carry both secured and unsecured debt that consolidation cannot address. Debt consolidation works only if you have sufficient income to service a new loan and access to favorable interest rates, conditions that rarely exist for people struggling with multiple debts. If your income drops unexpectedly or medical bills surge, you can request a plan modification rather than watching a consolidation loan default or a debt management plan collapse.

The Real Cost of Waiting

People who try consolidation or debt management first often return to bankruptcy months or years later after wasting thousands on fees and interest, whereas those who choose Chapter 13 immediately stabilize their finances and move forward with genuine recovery. The court-supervised structure removes guesswork and provides enforcement that private debt relief companies cannot match.

Final Thoughts

Chapter 13 bankruptcy offers Memphis residents a structured path to financial recovery that protects assets while addressing overwhelming debt. Unlike debt consolidation or management plans that shift obligations without reducing them, Chapter 13 provides court-supervised protection, immediate relief from creditor harassment, and genuine debt reduction through a manageable repayment plan. The automatic stay stops wage garnishment, foreclosure, and collection calls the moment you file, freeing up hundreds of dollars monthly that you can redirect toward rebuilding your financial life.

Your Memphis Chapter 13 options depend on your income, assets, and specific circumstances. If you earn regular income, want to keep your home or car, or need to catch up on missed payments, Chapter 13 becomes the only bankruptcy path that addresses your situation. After completing your plan, remaining eligible debts discharge, and you emerge with a clean financial slate and a demonstrated track record of meeting obligations that rebuilds your credit score within two to three years.

Debt compounds while creditors intensify collection efforts, making the problem worse rather than better if you delay action. We at Hurst Law Firm, P.A. can evaluate your Memphis Chapter 13 options during a free initial consultation and help you move toward genuine financial recovery. Contact us at 901-730-4958 or visit Hurst Law Firm, P.A. at 44 North Second Street, Suite 403, Memphis, TN 38103 to discuss your situation today.