Wage garnishment takes money directly from your paycheck before you ever see it. If you’re facing this situation in Memphis, you have options to fight back.

We at Hurst Law Firm, P.A. help people stop wage garnishment through bankruptcy and other legal strategies. This guide shows you exactly how to protect your income and regain control of your finances.

How Wage Garnishment Freezes Your Paycheck

Wage garnishment begins the moment a creditor wins a court judgment against you. The creditor files paperwork with the court, which then issues an order to your employer directing them to withhold money from your paycheck. Your employer becomes legally responsible for sending that withheld amount to the court, typically within 30 days. This process happens automatically once the order lands in your employer’s payroll department-you don’t get a choice, and your employer can’t refuse to comply. In Tennessee, the garnishment order lasts six months and can be renewed indefinitely until the debt is paid, meaning your paycheck can be frozen for years if you don’t act. Most people don’t realize they can challenge a garnishment until weeks after it starts, and by then they’ve already lost hundreds of dollars.

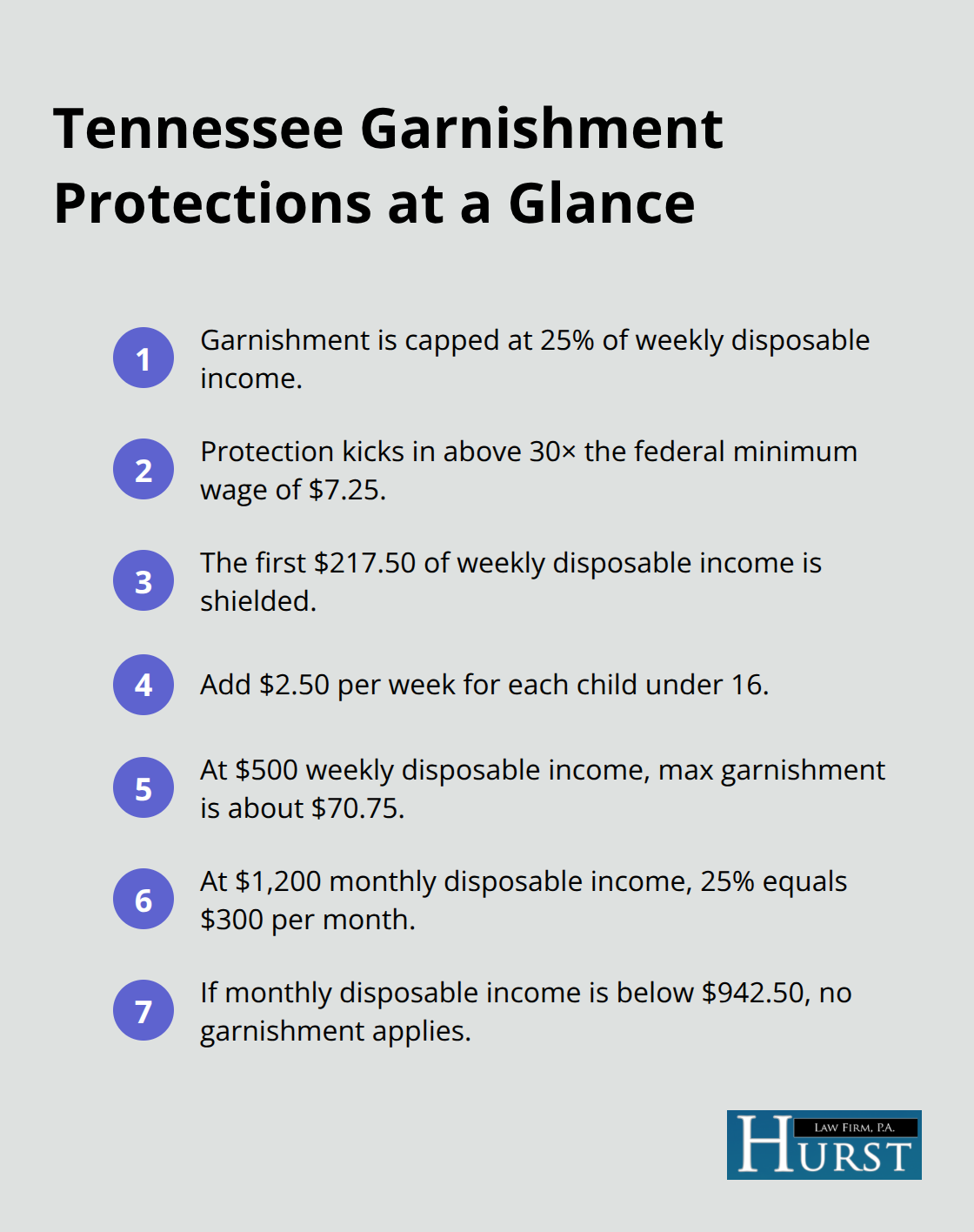

The Tennessee Limits That Actually Protect You

Tennessee law caps garnishment at 25 percent of your weekly disposable income or the amount by which your weekly earnings exceed 30 times the federal minimum wage of $7.25 per hour, whichever is smaller. This means the first $217.50 of your weekly disposable income is automatically protected by federal law. If you support children under 16, Tennessee adds another $2.50 per week for each child, which further reduces what creditors can take. The practical math shows the difference: if you earn $500 weekly in disposable income, the maximum garnishment is roughly $70.75, not the full 25 percent. If you earn $1,200 monthly in disposable income, a 25 percent garnishment equals $300 withheld monthly.

Creditors don’t always calculate this correctly, and many people don’t know they qualify for exemptions that could stop the garnishment entirely. If your monthly disposable income falls below $942.50, you shouldn’t face any garnishment whatsoever.

Which Debts Land You in Garnishment

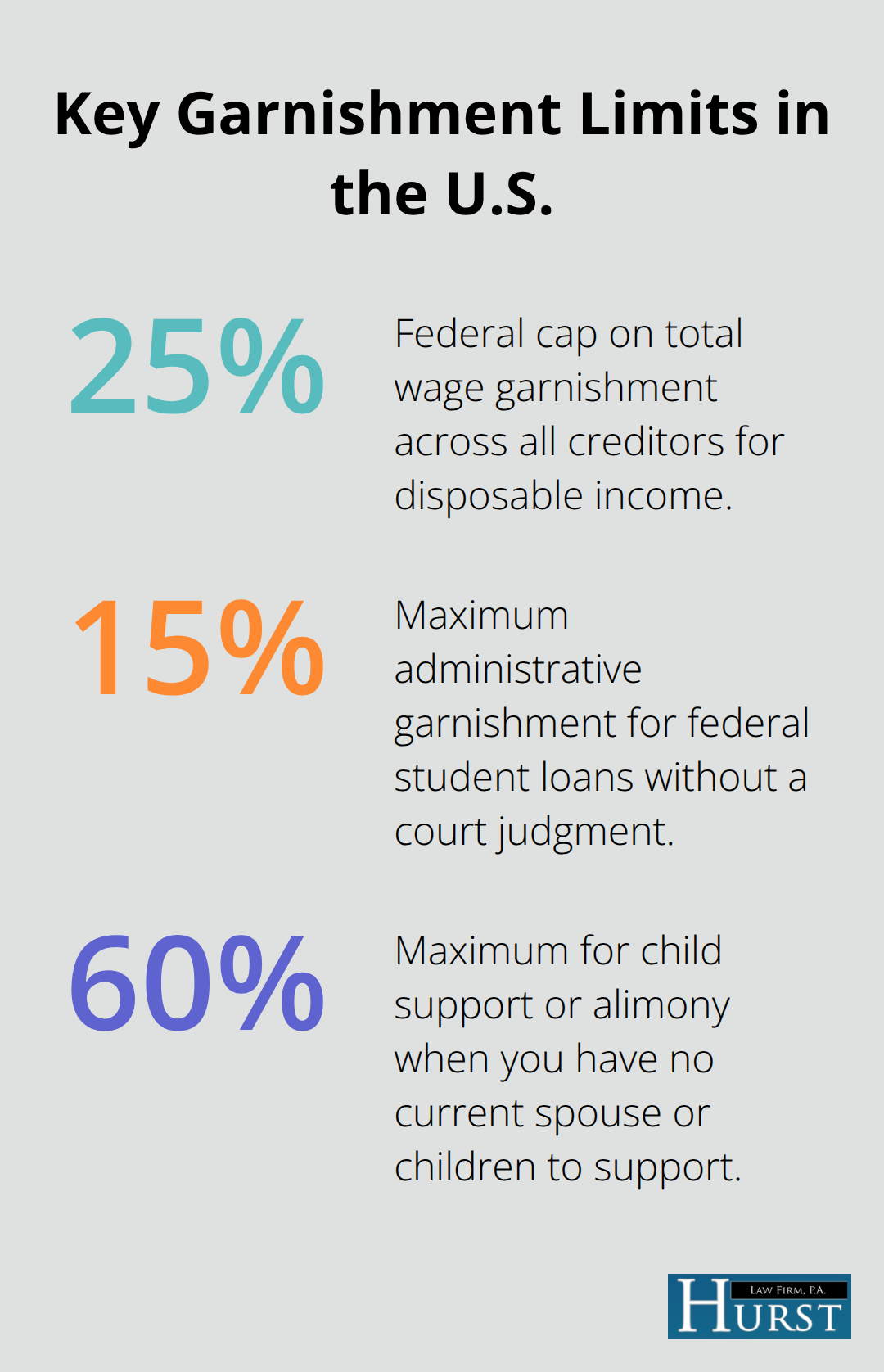

Credit card debt, medical bills, and personal loans require creditors to win a court judgment before they can garnish your wages, which means you have time to respond to a lawsuit. Federal student loans bypass the normal process entirely-the Department of Education can garnish up to 15 percent of your disposable income without obtaining a judgment first. The IRS and Tennessee Department of Revenue also garnish administratively without court involvement, making tax debt especially aggressive. Child support and alimony are the most severe: they can reach up to 60 percent of your pay if you have no current spouse or children to support, or 50 percent if you do. Back taxes from the state or federal government follow their own rules and can be paired with other garnishments. Most people facing garnishment in Memphis have multiple debts stacked on top of each other, but federal law caps total garnishment across all creditors at 25 percent of disposable income-a protection many people don’t enforce because they don’t know it exists.

Understanding how garnishment works and what protections you have under Tennessee law gives you the foundation to fight back. The next section shows you how bankruptcy stops wage garnishment immediately and provides a path forward.

Stop Wage Garnishment Through Bankruptcy

The Automatic Stay Halts Garnishment Within 24 Hours

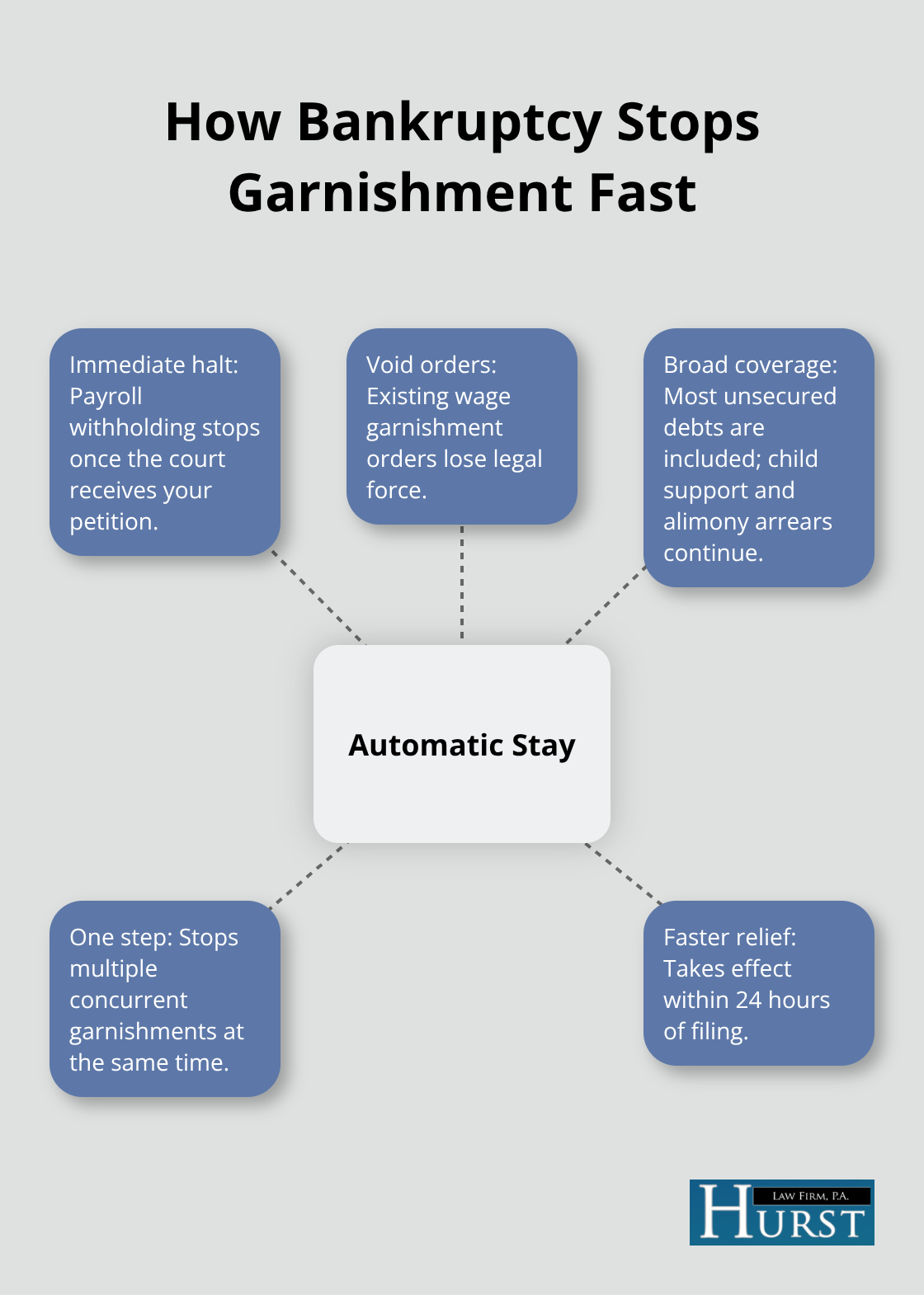

Filing for bankruptcy triggers an automatic stay within 24 hours that halts wage garnishment across nearly all debts. Your employer must stop withholding money from your paycheck instantly once the court receives your petition, and any garnishment orders become void. This automatic stay covers credit card debt, medical debt, personal loans, and most other unsecured debts, with the exception of child support and alimony arrears, which continue through the bankruptcy process. The speed matters significantly: if you face multiple garnishments that stack to 25 percent of your disposable income, filing bankruptcy stops all of them simultaneously rather than negotiating with each creditor individually.

Chapter 7 Eliminates the Underlying Debt

Chapter 7 bankruptcy eliminates most unsecured debts within three to six months, meaning the underlying judgment that sparked the garnishment disappears entirely and cannot be renewed. Once the court discharges your debts, creditors lose the legal foundation to garnish your wages again. The creditor cannot restart garnishment orders on a debt that no longer exists, which provides permanent relief rather than temporary breathing room. This path works best if you have limited income and few assets to protect.

Chapter 13 Reorganizes Debts Into Affordable Payments

Chapter 13 bankruptcy reorganizes your debts into a repayment plan over three to five years based on what you can actually afford, stopping garnishment while you make manageable monthly payments instead of having your paycheck frozen. You control the payment amount within the plan structure, which means your take-home pay stabilizes immediately. The court approves the plan based on your actual budget, not what creditors demand.

Timing Your Filing Matters for Renewal Cycles

Garnishment orders renew every six months if the debt remains unpaid. If you file Chapter 7 or Chapter 13 before a renewal date arrives, you avoid another round of garnishment orders and the accompanying court fees and creditor interest that accumulate during each six-month cycle. When multiple garnishments exist, bankruptcy becomes far more practical than fighting each one separately through objections or creditor negotiations, since the automatic stay eliminates all collection actions at once and gives you breathing room to stabilize your finances. The choice between Chapter 7 and Chapter 13 depends on your income level, assets, and ability to fund a repayment plan-factors that determine which path stops garnishment fastest while protecting what matters most to you.

Alternatives to Bankruptcy That Rarely Work

Negotiating Payment Plans With Creditors

Creditors prefer negotiated payment plans over court battles because collection costs money and time. If you contact a creditor or collection agency within the first week of garnishment, you may convince them to halt the withholding in exchange for a structured repayment agreement. The creditor’s account handler will typically discuss settlement amounts or monthly payment terms that fit your budget, and you should obtain written confirmation of any deal before sending payment. Establish a consistent payment history for three to six months using certified mail or bank drafts so you have proof of on-time payments, which strengthens your position if the creditor later threatens to restart garnishment.

However, creditor negotiations fail frequently in Memphis because people agree to payment terms they cannot sustain. Missed payments restart garnishment immediately, and you face additional court costs and attorney fees stacked on top of the original debt. The creditor holds all the leverage in these conversations because they already won the judgment, and they know most people will eventually miss a payment under pressure. Negotiation works only if your income genuinely covers the agreed amount every single month without exception, and most people facing garnishment lack that stability.

Filing Objections and Hardship Claims

Filing an objection or hardship claim within ten days of receiving the garnishment notice can pause withholding while you prepare your case, but only if you can document that the garnishment exceeds Tennessee’s legal limits or that withholding would prevent you from covering essential expenses like rent, utilities, groceries, and transportation. Gather your last three months of pay stubs, bank statements, and a detailed monthly budget showing rent, utilities, groceries, and transportation costs to demonstrate genuine hardship at the garnishment hearing.

Calculate your disposable income using the U.S. Department of Labor thresholds to prove whether you qualify for exemptions, and verify that the creditor calculated the garnishment percentage correctly. If your monthly disposable income falls below $942.50, you have a strong legal argument that garnishment violates Tennessee law. Many people win exemption hearings but creditors simply renew the garnishment order six months later, which means you fight the same battle repeatedly without permanent relief. Objections and hardship claims work best as temporary measures to buy time while you pursue a longer-term solution, not as a standalone strategy to stop garnishment permanently.

Why These Alternatives Fall Short

Both negotiation and objections offer temporary relief at best. Creditors can restart collection efforts after six months, and you remain trapped in a cycle of temporary fixes rather than permanent solutions. Bankruptcy provides the permanent relief that these alternatives cannot deliver, stopping garnishment immediately through the automatic stay and eliminating the underlying debts that fuel collection efforts. If you face multiple garnishments or unstable income, these alternatives will likely fail, leaving you vulnerable to continued wage loss and accumulating fees.

Final Thoughts

Bankruptcy stands out as the most effective solution to stop wage garnishment in Memphis because it addresses the root problem rather than treating symptoms. Chapter 7 eliminates the underlying debts entirely, preventing creditors from ever renewing garnishment orders on those accounts, while Chapter 13 stops garnishment immediately and reorganizes your debts into payments you can actually afford over three to five years. Both paths trigger an automatic stay within 24 hours that halts wage withholding across nearly all debts simultaneously, which matters enormously when multiple garnishments stack up and consume 25 percent of your paycheck.

Most people facing garnishment in Memphis have already tried negotiating or ignoring the problem, and neither approach works long-term. Your paycheck will continue freezing every six months unless you take decisive action, and the sooner you file for bankruptcy, the sooner the automatic stay stops the withholding and gives you breathing room to stabilize your finances. Temporary fixes like objections or creditor negotiations only delay the inevitable renewal cycle that keeps you trapped in financial strain.

We at Hurst Law Firm, P.A. offer a free initial consultation to determine whether Chapter 7 or Chapter 13 fits your situation best, and we can arrange evening or weekend appointments if your work schedule makes daytime meetings difficult. Contact us today to discuss your options and take the first step toward protecting your income and rebuilding your financial future.