Wage garnishment can take a significant portion of your paycheck before you ever see it. At Hurst Law Firm, P.A., we’ve helped countless Memphis TN residents navigate the wage garnishment consequences that threaten their financial stability.

The good news is you have options. This guide walks you through how garnishment works, what protections exist, and how to fight back.

How Garnishment Actually Works

Wage garnishment is a court-ordered withholding that takes money directly from your paycheck before you receive it. The process typically begins when a creditor wins a lawsuit against you and obtains a judgment. Once they have that judgment, they file paperwork with your employer instructing them to withhold a specific amount each pay period. Child support, federal student loans, and tax debts bypass this requirement-the government can garnish your wages without a court judgment at all. The IRS can levy your wages for back taxes using a statutory formula based on your standard deduction and dependents, as outlined in IRS Publication 1494. Federal student loans can be garnished at up to 15 percent of your disposable income without court involvement. In Memphis TN, creditors must follow Tennessee’s wage garnishment rules, which mirror federal limits but add extra protections for dependents.

Understanding Disposable Earnings and the Math

Federal law limits most garnishments to the lesser of 25 percent of your disposable earnings or the amount by which your weekly earnings exceed 30 times the federal minimum wage. Disposable earnings means your pay after legally required deductions like income taxes, Social Security, and Medicare-not voluntary deductions or health insurance. With the federal minimum wage at $7.25 per hour, the threshold sits at $217.50 per week. If you earn $400 in weekly disposable income, only $50 can be garnished that week (the amount above $217.50). If you earn $600 weekly, 25 percent applies, meaning $150 gets garnished. Tennessee adds an additional protection: you can keep an extra $2.50 per week for each dependent child under 16 living in Tennessee if you notify your employer. This matters significantly for families-having two dependents adds $5 weekly protection, which compounds over a year to $260 in additional income you retain.

When Garnishment Hits Harder

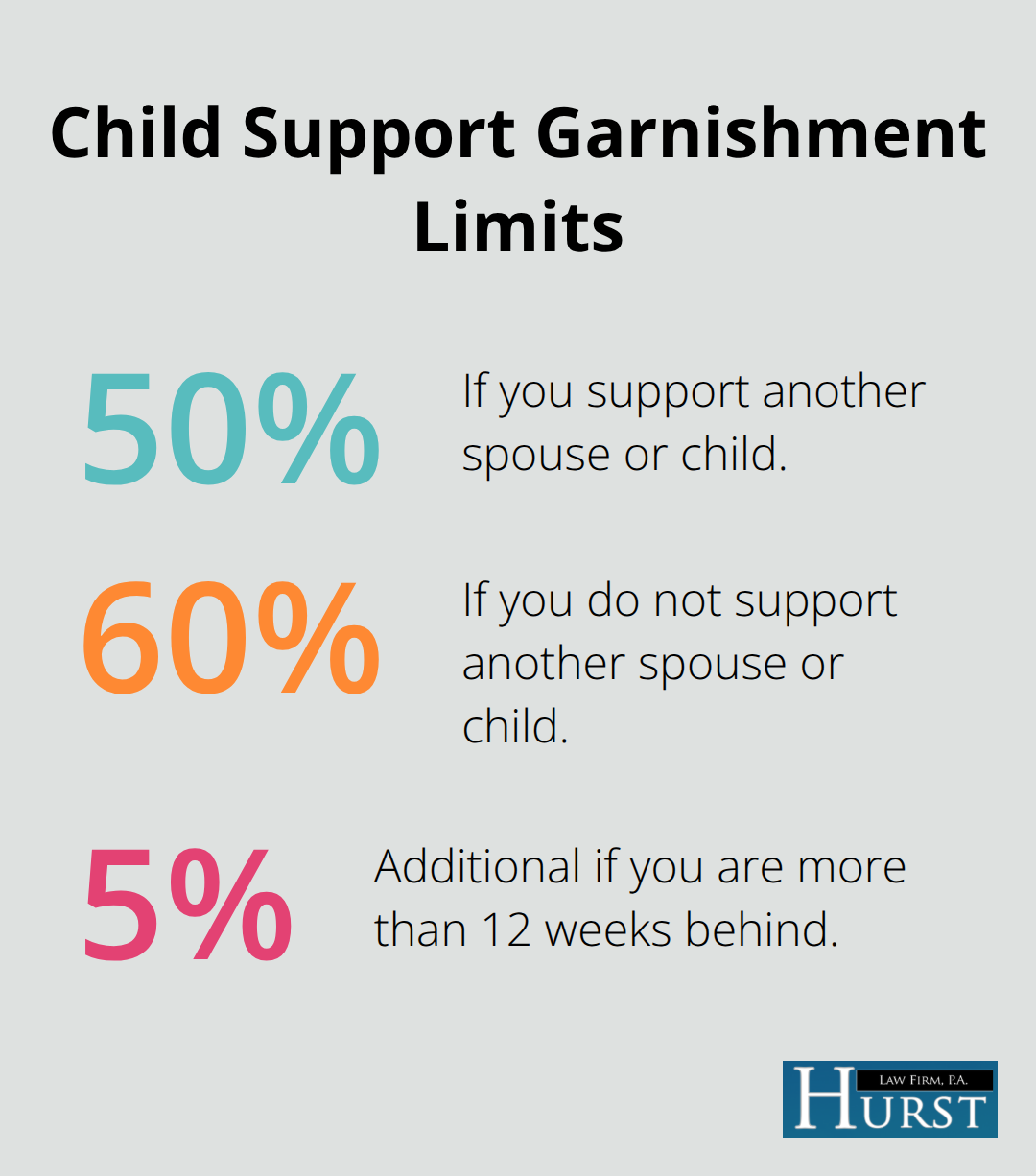

Child support garnishments operate under completely different rules and hit much harder. The government can take up to 50 percent of your disposable earnings if you’re supporting another spouse or child not subject to the order, jumping to 60 percent if you’re not supporting anyone else. An additional 5 percent can be taken if you’re more than 12 weeks behind on payments.

This means a single parent earning $600 weekly could lose $360 to child support garnishment alone. Federal student loan garnishments follow their own calculation under the Higher Education Act. The IRS uses a more complex exemption formula tied to standard deductions and family size rather than the simple 25 percent rule. These distinctions matter because they determine how much breathing room remains in your budget each month.

What Happens Next

Once your employer receives the garnishment order, they must comply within a specific timeframe. Your payroll department withholds the required amount and sends it to the court or creditor. You receive notice of the garnishment, but the withholding continues until the debt is paid in full or a court order stops it. Multiple creditors can garnish your wages simultaneously, though they follow a priority system based on which court order arrived first. The longer garnishment continues, the more your financial situation deteriorates-and that’s when other options become worth exploring.

What Wage Garnishment Actually Costs Your Family

The Immediate Hit to Your Monthly Budget

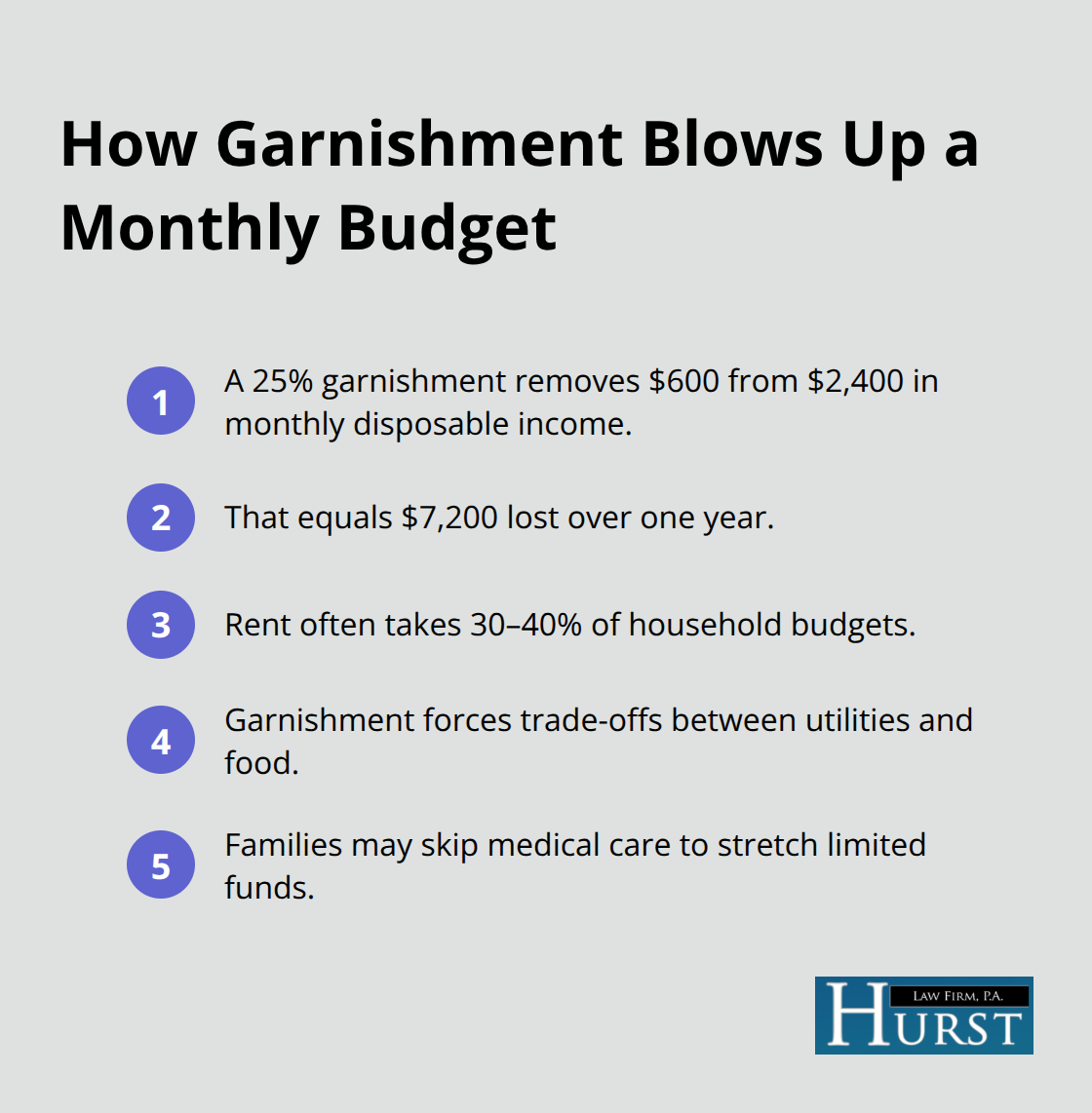

Wage garnishment removes money from your paycheck before you ever see it, creating an immediate crisis in your monthly budget. When a creditor garnishes 25 percent of your disposable earnings, that money vanishes before you can pay rent, utilities, or groceries. For a Memphis TN resident earning $2,400 monthly in disposable income, garnishment removes approximately $600 per month. Over a year, that totals $7,200 gone. If you support a family on this income, the math becomes brutal.

Rent alone consumes 30 to 40 percent of most household budgets, leaving little margin for error. Add garnishment, and you must choose between paying utilities and buying food, or skipping medical appointments to stretch your budget further.

The Federal Reserve’s 2023 survey found that 37 percent of Americans cannot cover a $400 emergency expense without borrowing. Wage garnishment creates constant emergencies. You fall behind on other obligations because the money simply isn’t there. Credit card payments stop. Medical bills pile up. You might miss your car payment, risking repossession. The stress compounds because garnishment is visible-your employer knows you face financial trouble, which affects your workplace relationships and confidence.

Credit Damage That Lasts Years

The credit damage from garnishment extends far beyond the immediate hit to your score. The underlying debt that triggered garnishment already damaged your credit when you first fell behind on payments. Now garnishment itself signals to lenders that you cannot meet obligations, and the collection activity remains on your credit report for up to seven years. A lower credit score means higher interest rates on future loans, higher car insurance premiums, and potential denial of rental applications.

Employers increasingly run credit checks during hiring, so garnishment can cost you job opportunities. This creates a vicious cycle: reduced income from garnishment makes it harder to find better employment, and a damaged credit score blocks access to the jobs that do exist. The financial consequences ripple outward, affecting every aspect of your economic life.

The Hidden Health and Emotional Toll

The emotional toll on families is substantial and often overlooked. Parents feel shame about financial instability. Children sense the tension and anxiety at home. Relationships strain under the pressure of reduced income and constant financial worry. Sleep disruption, anxiety disorders, and depression are common among people experiencing wage garnishment. These aren’t minor inconveniences-they represent serious health consequences that affect your ability to work productively and make sound financial decisions.

When garnishment hits, your entire family enters survival mode. That mode is exhausting and unsustainable. The combination of reduced income, damaged credit, and psychological stress creates a perfect storm that makes escape seem impossible without intervention. Understanding these consequences matters because they reveal why wage garnishment demands immediate action rather than passive acceptance.

Legal Protections Stop Garnishment Before It Drains Your Income

Federal and State Wage Garnishment Limits

Federal law caps what creditors can take from your paycheck, but these limits still allow significant damage. The Consumer Credit Protection Act restricts most garnishments to 25 percent of your disposable earnings or the amount by which your weekly earnings exceed 30 times the federal minimum wage, whichever is lower. In Memphis TN, Tennessee law mirrors these federal caps but adds a $2.50 weekly buffer per dependent child under 16 living in your household. This protection only works if you notify your employer in writing about your dependents. Many people miss this step entirely and lose money they could legally protect.

Higher Limits for Specific Debts

Child support and alimony operate under completely different rules. The government can take up to 50 percent of your disposable earnings if you support another spouse or child, or 60 percent if you do not. An additional 5 percent applies if you fall more than 12 weeks behind on payments. Federal student loan garnishments can reach 15 percent of disposable income without any court judgment required. The IRS uses a completely different formula based on your standard deduction and family size rather than the simple percentage approach. Understanding which rule applies to your specific debt matters enormously because the wrong assumption could cost you hundreds monthly.

Exemptions and Court Challenges

You can file an exemption with the court claiming financial hardship or dependent status, but courts rarely grant full relief unless your income barely covers basic living expenses. The threshold is brutally high: you must prove you cannot afford food, housing, utilities, and transportation after garnishment stops. Most judges deny exemption requests because they view any income above absolute poverty as sufficient.

How Bankruptcy Stops Garnishment Immediately

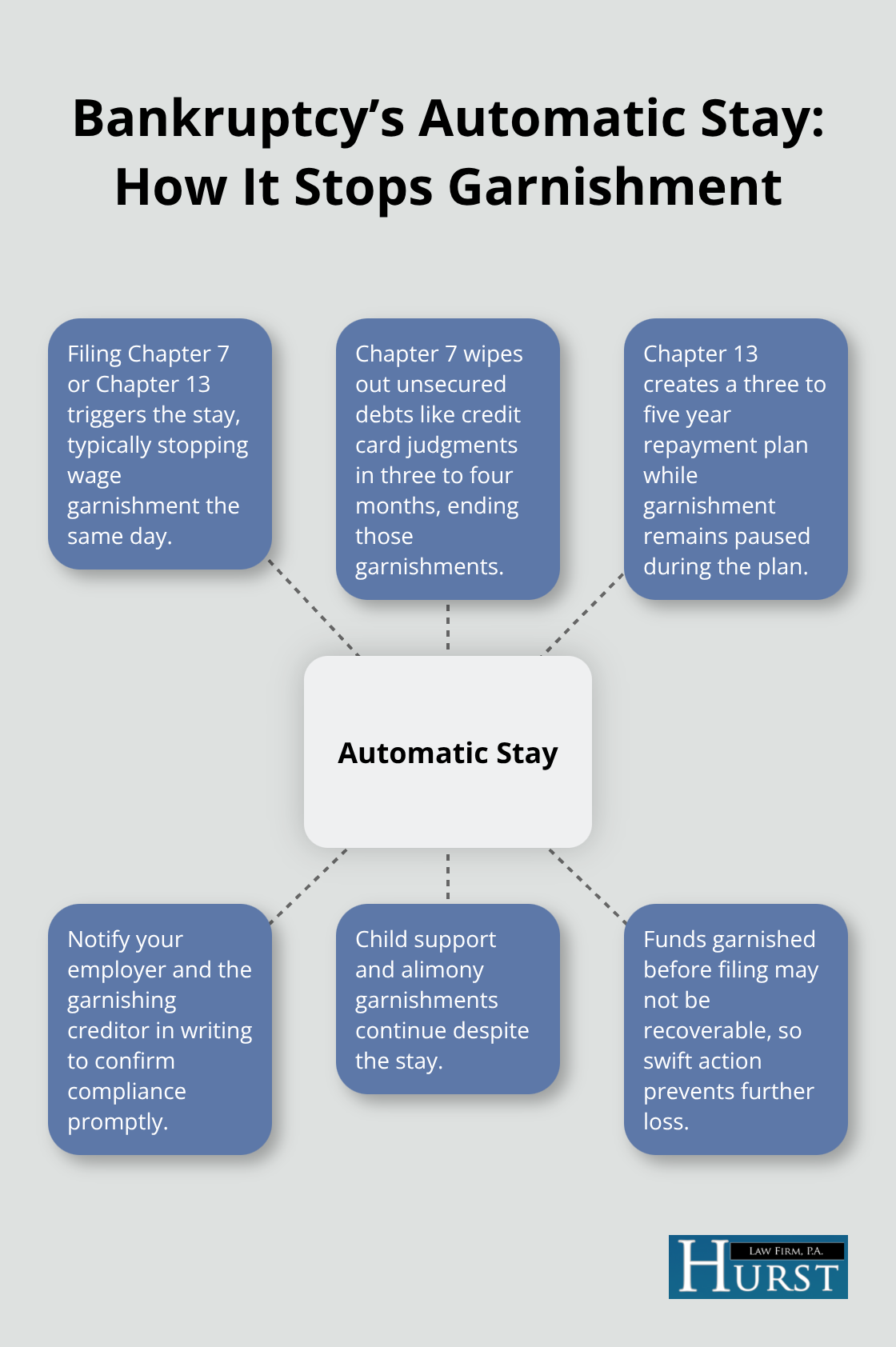

Bankruptcy offers the only reliable way to stop most wage garnishments immediately. When you file Chapter 7 or Chapter 13 bankruptcy in the Western District of Tennessee, the automatic stay takes effect as soon as your petition reaches the court. This federal injunction halts wage garnishment the same day in most cases, though you should notify your employer and the garnishing creditor in writing to confirm compliance. Chapter 7 bankruptcy eliminates unsecured debts like credit card judgments within three to four months, stopping garnishment permanently for those debts. Chapter 13 bankruptcy restructures your debts into a three to five year repayment plan while the automatic stay pauses garnishment throughout the plan period. Chapter 13 works particularly well if you have mortgage arrears or tax obligations because you can cure those defaults within the plan while garnishment remains paused.

The timing of filing matters critically: funds garnished before you file cannot always be recovered, so swift action prevents additional losses. The automatic stay does not protect child support or alimony garnishments, which continue even after bankruptcy filing, but it stops most other creditor garnishments immediately. Non-bankruptcy alternatives like settlement negotiations or payment plans rarely work once garnishment begins because creditors have already won their court judgment and have no incentive to compromise.

Final Thoughts

Wage garnishment consequences extend far beyond the immediate reduction in your paycheck. The financial strain, credit damage, and emotional toll combine to create a crisis that demands action. If you’re facing garnishment right now, act quickly by contacting the court that issued the garnishment order to understand the exact amount being withheld and the underlying debt. Review your pay stubs to confirm your employer is following federal and Tennessee limits, and notify your employer in writing if you have dependent children under 16 living in Tennessee to claim the additional $2.50 weekly protection per child.

Consider whether bankruptcy makes sense for your situation. Chapter 7 eliminates unsecured debts like credit card judgments within three to four months, stopping garnishment permanently for those debts. Chapter 13 restructures your debts into a manageable three to five year plan while the automatic stay pauses garnishment immediately. Both options trigger the automatic stay in the Western District of Tennessee, halting most wage garnishments the same day you file (though funds already garnished before filing may not be recoverable).

We at Hurst Law Firm, P.A. help Memphis residents escape wage garnishment through Chapter 7 and Chapter 13 bankruptcy filings designed to give you the fresh start you need. Contact us for a free consultation to explore whether bankruptcy can stop your garnishment and eliminate the underlying debt. Your financial future depends on taking action today rather than watching garnishment drain your income month after month.