Wage garnishment can take a significant chunk out of your paycheck before you ever see it. If creditors are currently garnishing your wages, you have more options than you might realize.

We at Hurst Law Firm, P.A. help Memphis TN residents explore garnishment relief options that can stop or reduce these deductions. This guide walks you through how garnishment works, what strategies can help, and how to rebuild your finances afterward.

How Wage Garnishment Works in Tennessee

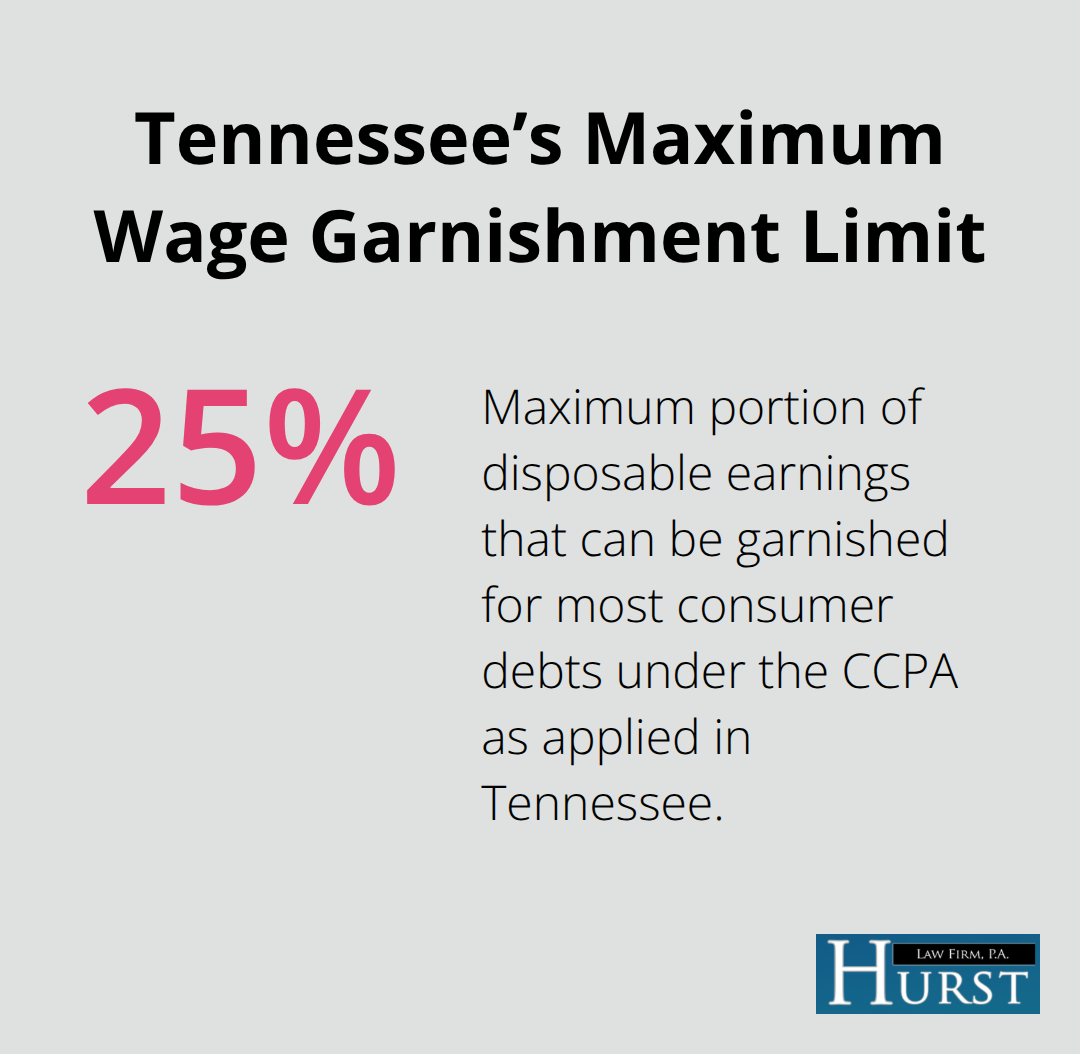

Tennessee follows federal wage garnishment limits set by the Consumer Credit Protection Act, which caps most garnishments at the lesser of 25% of your disposable earnings or the amount by which your weekly disposable income exceeds 30 times the federal minimum wage of $7.25 per hour. This means if you earn $217.50 or less per week in disposable income, creditors cannot garnish your wages at all. Once weekly disposable earnings reach $290 or higher, the maximum garnishment jumps to 25% of that amount. The calculation changes with your pay period-biweekly thresholds are $435, semimonthly thresholds are $471.25, and monthly thresholds are $942.50.

Disposable earnings exclude legally required deductions like taxes and Social Security but include most wages, salaries, commissions, and bonuses.

How Creditors Obtain Garnishment Orders

Creditors typically need a court judgment before they can garnish your wages, which means they must first sue you, win the case, and then file a separate garnishment order with your employer. This process takes time, and many people receive a Summons of Continuing Garnishment notice that specifies the court, case number, plaintiff, defendant, and judgment amount-information you should verify immediately with the court clerk to confirm the judgment is valid and properly served. Acting quickly matters because the longer garnishment continues, the more money flows to creditors instead of your household needs.

Tennessee’s Garnishment Duration and Renewal

Tennessee garnishment orders remain active for 179 days before creditors must file to renew them, meaning a single garnishment can continue for months without your involvement. The state does not provide stronger protections than federal law for most consumer debts, though you may have exemptions if you receive Social Security, veterans benefits, federal student aid, or certain retirement income-these sources remain protected even if garnished by mistake.

The Real Impact on Your Household

Take-home pay shrinks fast under garnishment; losing 25% of disposable earnings over five months averages about 11% of gross pay according to debt collection data. Families dependent on steady paychecks feel this immediately through missed rent, groceries, or utilities. Your employer must comply with the garnishment order and cannot fire you for a single garnishment under federal law, but multiple garnishments can jeopardize your job.

Challenging Invalid Garnishments

If you believe the judgment is invalid, service was improper, or exempt funds are being garnished, you can file a motion to challenge it, but deadlines are strict and often require court filing within days of receiving notice. Understanding these rules positions you to explore relief strategies that can stop the deductions and protect your income.

Strategies to Stop or Reduce Wage Garnishment

Filing for Bankruptcy Protection

Bankruptcy remains the fastest and most effective way to halt wage garnishment. When you file for Chapter 7 or Chapter 13 bankruptcy, an automatic stay takes effect immediately upon filing, and your employer must stop all withholding within days. The U.S. Bankruptcy Code mandates that creditors cease collection actions the moment your case is filed, which means no more garnishment notices and no more money flowing to creditors through your paycheck.

Chapter 7 bankruptcy discharges most unsecured debts like credit cards and medical bills within three to four months. Chapter 13 creates a structured repayment plan over three to five years that stops garnishment while you repay a portion of what you owe. If you earn steady income and have assets you want to protect, Chapter 13 is often preferable because it lets you keep your property while paying back creditors under court supervision.

The Consumer Credit Protection Act protects you from being fired for a single garnishment, but multiple garnishments can threaten your employment. Bankruptcy eliminates this risk entirely and halts creditor harassment at the same time.

Negotiating Directly with Creditors

Creditors often prefer a written payment plan to ongoing court collection costs. Contact the creditor’s attorney listed on your garnishment notice and propose either a lump-sum settlement or a monthly payment plan you can actually afford. A concrete offer (such as paying 40 to 50 percent of the debt over 12 months) shows you are serious, and many creditors will pause garnishment if you sign a written agreement committing to those terms.

Never offer more than you can sustain, and always verify the debt’s age before making payments. A single payment can restart the statute of limitations on time-barred debts, which means you could lose a valuable legal defense. Get any agreement in writing and confirm that the creditor will stop the garnishment once you meet the terms.

Claiming Wage Exemptions

Wage exemptions work best when you apply them immediately after receiving a garnishment notice. Social Security, SSI, veterans benefits, federal student aid, and many retirement accounts remain protected by federal law even if creditors attempt to garnish them. File a Claim of Exemption with the court and provide proof such as bank statements or pay stubs showing where your income originates.

If you are the head of household supporting dependents, Tennessee law may allow you to reduce garnishment further (though state protections are not stronger than federal limits for most consumer debts). Timing matters because courts set strict deadlines for exemption claims, often within days of receiving the garnishment notice. Missing these deadlines can cost you thousands in protected income.

Each of these three strategies offers a different path forward, and the right choice depends on your income, debts, and long-term financial goals. Understanding which option fits your situation positions you to take action and protect your paycheck.

Rebuilding Your Financial Stability After Garnishment Stops

Once garnishment ends, your paycheck finally reflects your actual earnings, but the financial damage from months of reduced income often lingers. The average person loses roughly 11% of gross pay over five months of garnishment according to debt collection data, which translates to thousands of dollars that could have covered essentials. Rebuilding requires a different mindset than simply waiting for the next crisis.

Track Your Spending for 30 Days

Start by tracking exactly where your money goes for 30 days without changing your spending habits. Most Memphis TN residents discover they spend more on subscriptions, food delivery, and impulse purchases than they realize. Once you see the actual numbers, you can cut the obvious waste first-streaming services you do not use, convenience store visits that drain your account, or restaurant meals you could replace with home cooking.

Create a Written Budget

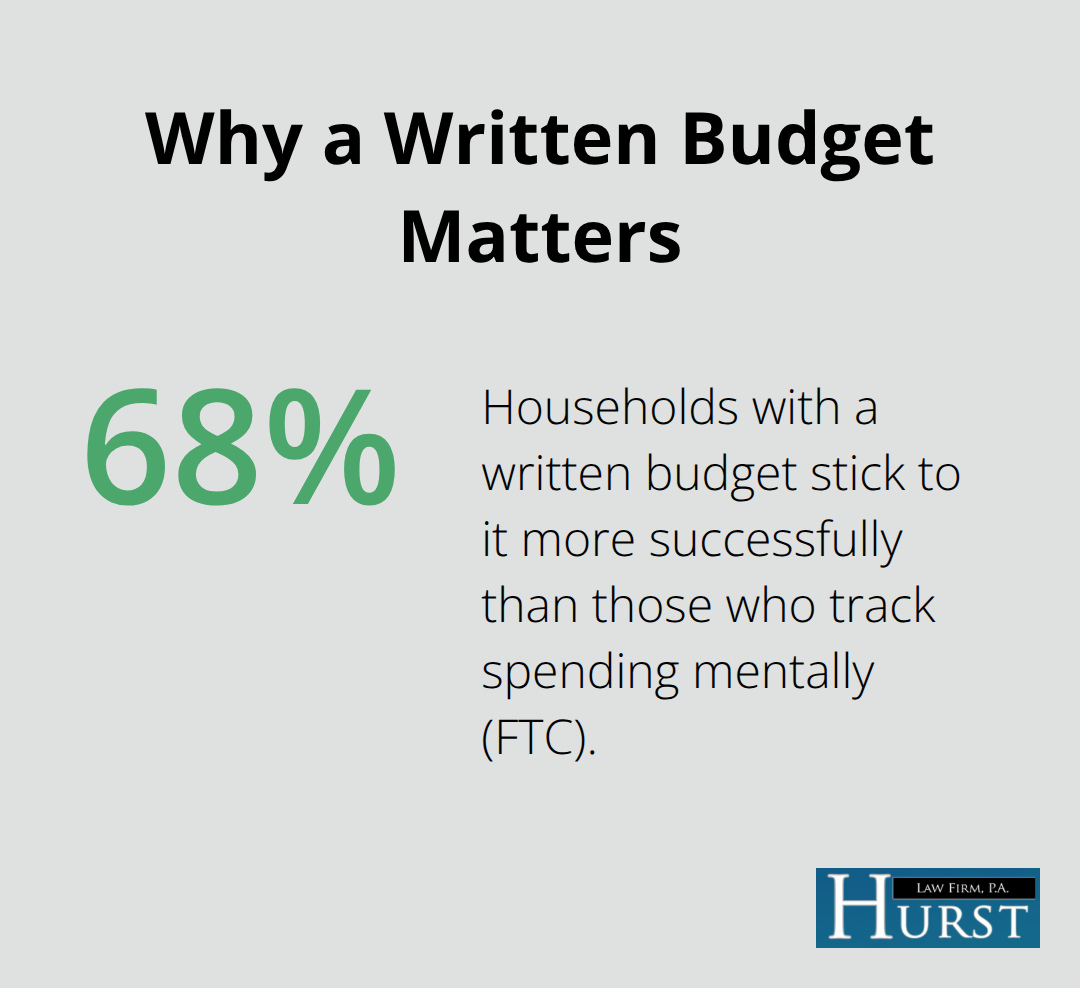

The Federal Trade Commission reports that households creating a written budget stick to it 68% more successfully than those who do not track spending mentally. Write down your income, list every expense category, and assign each dollar a job before the month starts.

This is not about deprivation; it is about control. You earned that money, and you deserve to decide where it goes instead of letting creditors or careless spending habits take it.

Build an Emergency Fund While Paying Debt

Second, prioritize building a small emergency fund even if you still carry debt. Financial counselors recommend starting with $500 to $1,000 to cover unexpected car repairs or medical bills that would otherwise force you back into credit card debt. Set up automatic transfers of even $25 per paycheck into a separate savings account you do not touch. This buffer prevents the cycle that led to garnishment in the first place-one emergency, one missed payment, one lawsuit, one garnishment.

Stop Accumulating New Debt

While you build this fund, stop accumulating new debt immediately. Do not open new credit cards, take personal loans, or finance purchases on payment plans. If you filed for Chapter 7 bankruptcy, your discharged debts are gone and you have a genuine fresh start; use it wisely for at least two years. If you filed for Chapter 13 bankruptcy, you are already on a structured repayment plan that protects you from additional garnishments as long as you make plan payments on time. An attorney at Hurst Law Firm, P.A. can help you understand your specific obligations post-bankruptcy and answer questions about rebuilding credit responsibly.

Final Thoughts

Wage garnishment strips your paycheck month after month, but you hold more power than you realize. Bankruptcy remains the fastest solution-filing Chapter 7 or Chapter 13 triggers an automatic stay that halts garnishment immediately, stops creditor harassment, and gives you breathing room to rebuild. If bankruptcy does not fit your situation, negotiating a written payment plan with creditors can pause garnishment while you repay what you owe, or claiming wage exemptions for Social Security, veterans benefits, or retirement income protects thousands of dollars that creditors cannot touch.

The financial damage from garnishment extends beyond the money lost to creditors. Rebuilding requires you to track your spending, create a written budget, build a small emergency fund, and stop accumulating new debt-these steps prevent the cycle that led to garnishment in the first place and position you for genuine financial stability. Your next step is straightforward: contact Hurst Law Firm, P.A. to discuss which garnishment relief option fits your income, debts, and goals. The sooner you act, the sooner your paycheck reflects what you actually earned.