Filing Chapter 7 bankruptcy without an attorney is possible, but it requires careful attention to detail and strict adherence to federal rules. The process involves multiple steps, from qualifying for Chapter 7 to attending your creditor meeting and receiving your discharge.

At Hurst Law Firm, P.A., we’ve seen countless Memphis TN residents attempt DIY bankruptcy Chapter 7 only to face costly mistakes. This guide walks you through each step so you understand what’s involved before deciding whether to proceed alone.

Step 1: Determine if You Qualify for Chapter 7 Bankruptcy in Memphis TN

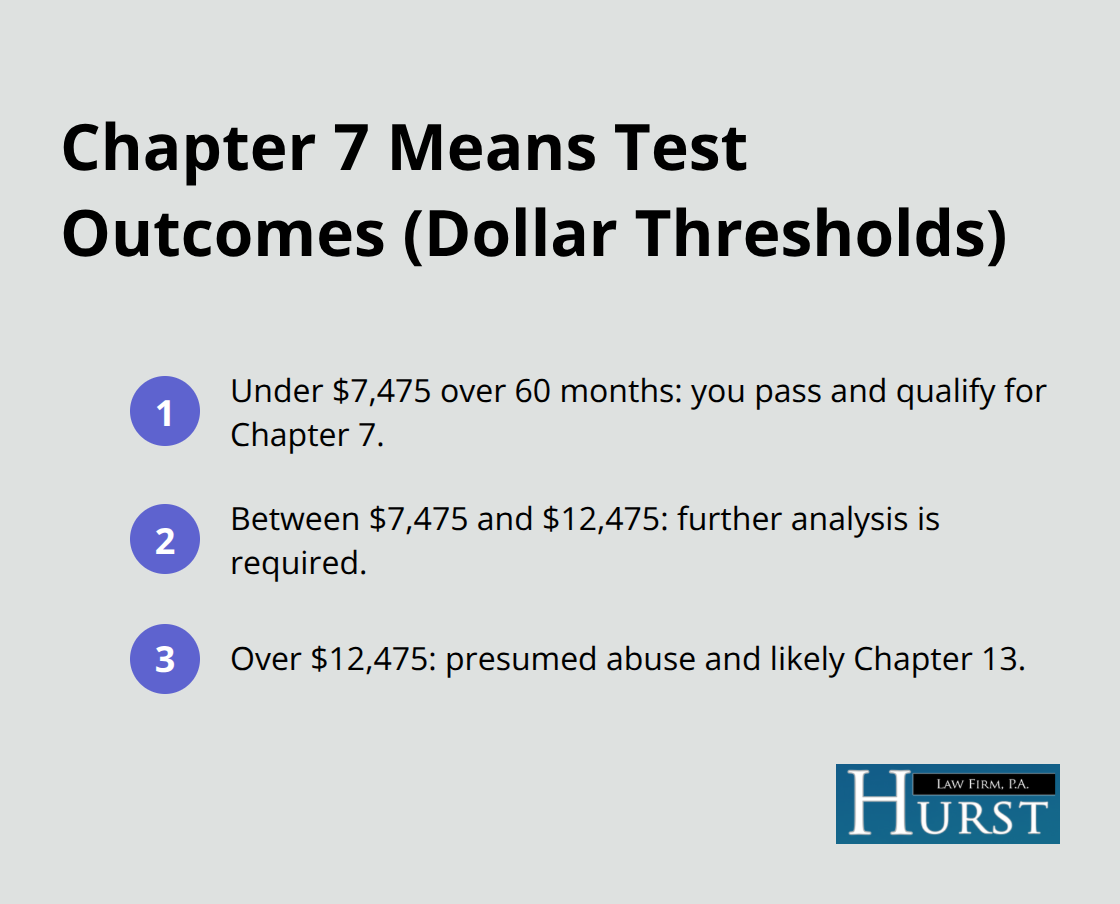

Chapter 7 eligibility hinges on passing the means test, which compares your income to Tennessee’s median thresholds. For a single filer in Tennessee, the median income is $39,759 annually; for a family of four, it reaches $79,045 according to U.S. Census Bureau data. If your household income falls below the state median for your family size, you pass automatically and can proceed with Chapter 7. If your income exceeds the median, the means test calculates your disposable income over 60 months using IRS expense standards. You subtract allowed living expenses from your income to determine whether you have money left over to repay creditors.

The disposable income threshold determines your path forward: if your monthly disposable income totals less than $7,475 over 60 months, you pass the means test and qualify for Chapter 7. If it exceeds $12,475, the court presumes abuse and you’ll likely need to file Chapter 13 instead, which requires a repayment plan. Amounts falling between these figures require more detailed analysis, and this is where many DIY filers make costly errors. Self-employed individuals must use actual average income from the past six months rather than estimates, which often surprises business owners. Gather your last two years of tax returns, recent pay stubs, and document all household expenses from the past three months to calculate accurate figures before you move forward with filing.

Step 2: Complete Credit Counseling Before Filing

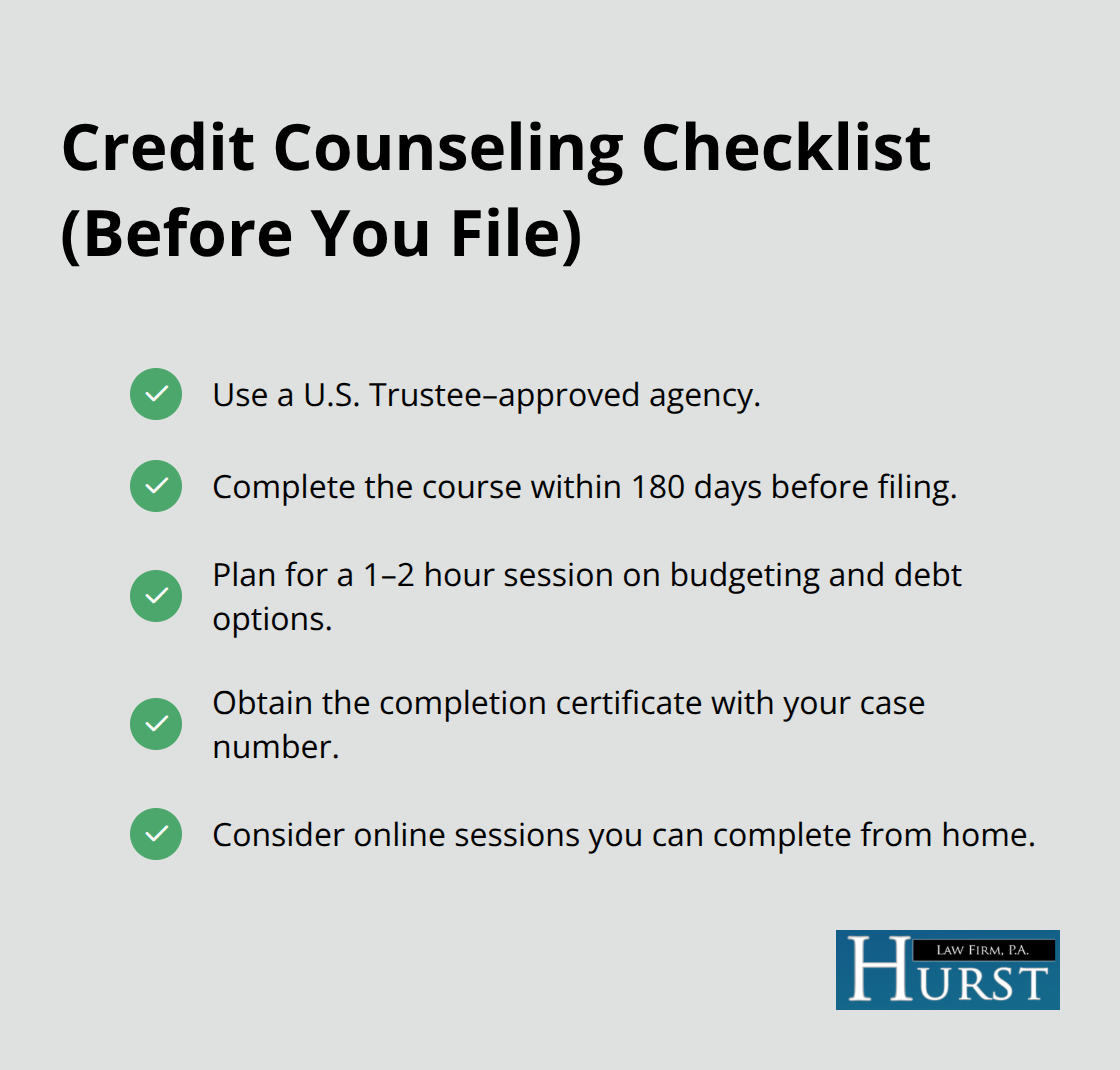

Credit counseling is mandatory before you file Chapter 7, and the U.S. Courts require you to complete it within 180 days of submitting your petition. You must use an agency approved by the U.S. Trustee Program, not just any credit counseling service. Search for approved providers on the U.S. Trustee website and filter by Tennessee to find legitimate agencies near you. Most sessions run 1 to 2 hours and cover budgeting basics, debt management alternatives, and the consequences of bankruptcy. You’ll receive a certificate with a case number upon completion, and this document is non-negotiable-without it, the court will not process your petition.

Schedule your counseling session well before you plan to file so delays don’t push you past the 180-day window. Many approved agencies offer online sessions, which means you can complete the requirement from home without traveling to Memphis. Save your completion certificate in a secure folder with all your other bankruptcy documents because you’ll need to attach it to your official petition. Unapproved agencies or skipped counseling sessions result in case dismissals that waste months and filing fees. With your counseling certificate in hand, you’re ready to move forward to the next critical phase: gathering all the financial documents the court requires.

Step 3: Gather Your Financial Documents

Collecting the right documents before you start filling out forms saves weeks of delays and prevents the court from rejecting your petition. The U.S. Courts require your last two years of tax returns, six months of recent pay stubs, and bank statements from the past three months to verify income and expenses. If you’re self-employed, gather profit-and-loss statements or business tax returns showing actual average income from the past six months, since the means test relies on documented figures, not estimates. Many Memphis DIY filers fail to organize complete financial records, which triggers requests for additional documentation that postpone your case number assignment by 30 to 60 days. Start organizing these documents immediately in a single folder so you have them ready when you begin the petition.

List every debt with the creditor’s name, account number, current balance, and monthly payment amount, including accounts you haven’t paid in years. Document all household expenses by reviewing your bank and credit card statements from the last three months and calculating average spending on groceries, utilities, transportation, insurance, and childcare because the bankruptcy court uses these actual numbers to determine eligibility. Property valuations matter too-research the fair market value of your home using recent comparable sales in your Memphis neighborhood, your vehicle’s current value through NADA Guides or Kelley Blue Book, and any other assets like furniture or jewelry. Accuracy here prevents challenges at your 341 meeting and protects your asset exemptions. Once you’ve compiled these documents with supporting statements, you move forward to completing the official bankruptcy forms that the court requires.

Step 4: Complete the Official Bankruptcy Forms

The U.S. Courts website provides all required forms free of charge, but organizing them correctly takes time most DIY filers underestimate. You’ll need Form 106Sum (case summary), Form 106A/B (property schedule), Form 106I (income and expenses), Form 106D (creditors holding unsecured nonpriority claims), Form 106E/F (creditors holding unsecured priority claims), Form 106H (executory contracts), and Form 106Sum (statement of financial affairs). Your specific Tennessee district may require additional local forms, so check your court’s website before printing anything. Download these forms from the federal judiciary website and print them double-sided to match court requirements, then number every page sequentially across all documents.

Accuracy matters intensely here because inconsistencies between your income statement, asset list, and creditor matrix trigger red flags at your 341 meeting. Fill in each form with exact figures from your financial documents, matching asset values to property valuations you researched and listing debts with precise balances from creditor statements. If your home value is $180,000 according to comparable sales but you owe $150,000 on the mortgage, the equity figure affects exemption calculations and trustee asset evaluation. Self-employed filers must calculate average income from the past six months using actual tax returns rather than current month estimates, which frequently causes means test failures when DIY filers guess. Verify that every debt listed on your creditor matrix appears on Schedule D (secured debts) or Schedule E/F (unsecured debts) to prevent creditors from claiming they received no notice.

Once all forms are complete and cross-verified, attach your credit counseling certificate and prepare your filing fee. The next step involves submitting these documents to the Memphis bankruptcy court and understanding what happens after you file.

Step 5: Submit Your Petition and Receive Your Case Number

The Chapter 7 filing fee totals $338, comprised of a $245 base fee, a $75 administrative fee, and a $15 trustee surcharge according to the U.S. Courts. If your household income falls below 150% of the federal poverty line, you qualify for a fee waiver under 28 U.S.C. § 1930(f), which eliminates the filing cost entirely. You can also request to pay the $338 fee in up to four installments, with the final payment due within 180 days of filing, which helps Memphis residents who lack liquid cash.

Submit your complete petition package to the Memphis bankruptcy court either electronically through eSR (the online filing system for pro se filers in the Western District of Tennessee) or in person at the courthouse located at 200 Jefferson Avenue. eSR operates 24/7 from any internet-enabled device, requires no software download, and costs nothing to use beyond your filing fee.

The court assigns a case number only after all required documents arrive physically, not when you submit them electronically. After you upload your petition through eSR, you must deliver your Declaration form, proof of your Social Security number, the filing fee or waiver request, and your credit counseling certificate in person or by mail within 10 days to prevent rejection. If you miss this 10-day deadline, your filing gets rejected and you must start over, losing weeks of progress. Once the court receives your complete package, you’ll receive a case number within 1 to 3 business days, and the trustee assigned to your case will contact you to schedule your 341 meeting, typically held 21 to 40 days after filing. With your case number in hand, you move forward to the meeting that determines what assets the trustee will liquidate and how your creditors receive notice of your bankruptcy filing.

Step 6: Attend the 341 Meeting of Creditors

The 341 meeting of creditors takes place 21 to 40 days after your case number is assigned, and it represents the single most important appearance you’ll make in your bankruptcy case. Most meetings last only 5 to 10 minutes, but the trustee assigned to your case will ask specific questions about your finances, assets, and the accuracy of your petition. Attend in person at the Memphis courthouse or your assigned location with a government-issued photo ID, your Social Security card, and your most recent tax returns if the trustee requests them beforehand.

Missing this meeting results in immediate case dismissal, which leaves your debts unpaid and allows creditors to resume collection actions. The trustee’s questions focus on whether your asset valuations are accurate, whether you disclosed all debts and income sources, and whether any transfers or unusual transactions occurred in the months before filing.

Answer every question directly and honestly, even if the answer reveals problems with your petition. Many DIY filers panic during the meeting and provide inconsistent answers that contradict their written petition, which triggers deeper investigation and potential fraud allegations. Bring documentation of your asset valuations-screenshots from Kelley Blue Book for vehicles, recent appraisals, or comparable sales data for property-so you can explain your numbers if challenged. If you listed your home’s value at $180,000 on your petition but the trustee discovers recent comparable sales showing $220,000, you’ll face tough questions about why the discrepancy exists.

If you’re uncertain about any question during the meeting, say so rather than guessing; the trustee respects honesty and will give you time to provide accurate information later. With the 341 meeting complete, you move forward to the final requirement before receiving your discharge: completing the debtor education course that the court mandates for all Chapter 7 filers.

Step 7: Complete Debtor Education and Receive Your Discharge

The debtor education course is your final requirement before the court grants your discharge, and it differs significantly from the credit counseling you completed before filing. This course focuses on budgeting, rebuilding credit, and managing money after bankruptcy rather than exploring alternatives to filing. You must complete an approved debtor education course within 60 days after your 341 meeting, though most Memphis filers finish it within two weeks to avoid missing the deadline. The course typically runs 2 to 3 hours and covers topics like creating a realistic budget, understanding credit reports, and avoiding the behaviors that led to your financial crisis. Online courses allow you to complete the requirement from home at your own pace, and you receive a certificate immediately upon finishing the final exam.

File your debtor education certificate with the bankruptcy court before your deadline expires, which the court specifies in your case paperwork after the 341 meeting. Missing this deadline can delay your discharge by 30 to 60 days or trigger case dismissal, so treat this filing as non-negotiable. Most Memphis filers receive their discharge order 60 to 90 days after the 341 meeting, assuming no objections arise and you submit both your debtor education certificate and any required documents. The discharge eliminates most unsecured debts like credit cards, medical bills, and personal loans, though secured debts tied to collateral and non-dischargeable debts like student loans and child support remain. Once your discharge becomes final, you move forward to understanding what happens next with your credit score and long-term financial recovery, which determines whether your fresh start actually leads to sustained financial stability.

Final Thoughts

DIY bankruptcy Chapter 7 filing saves attorney fees upfront, but mistakes often cost more than professional guidance would have. We at Hurst Law Firm, P.A. have watched Memphis residents face case dismissals because they missed the 10-day deadline for submitting documents after eSR filing, miscalculated means test disposable income, or failed to disclose assets that triggered trustee objections. These errors delay your fresh start by months and waste your filing fee entirely.

Inconsistent asset valuations represent the most common pitfall in DIY bankruptcy Chapter 7 cases. A self-represented filer lists their home at $180,000 on the petition but comparable sales show $220,000, or they undervalue a vehicle to reduce trustee interest in liquidation-the trustee catches these discrepancies at your 341 meeting and credibility damage follows you through the rest of your case. Exemption calculations also trip up self-represented filers who don’t understand whether Tennessee state exemptions or federal exemptions protect their property better, and selecting the wrong exemption set can cost you thousands in assets the trustee could have protected.

Professional guidance protects your rights by ensuring accurate means test calculations, proper exemption selection, and complete asset disclosure that prevents post-discharge complications. If your case becomes complex because you own a business, face potential fraud allegations, or have significant assets, attempting DIY filing becomes genuinely risky. We at Hurst Law Firm, P.A. have been helping Memphis residents since 1997, and we understand the local court procedures and trustee expectations that DIY filers often miss.