Drowning in debt doesn’t mean you have to lose your home. A Memphis Chapter 13 bankruptcy gives you a structured path to reorganize what you owe while keeping the assets that matter most.

We at Hurst Law Firm, P.A. help Memphis residents understand how this process works and whether it fits your situation. The next sections break down the mechanics, who benefits most, and how to build a plan that actually works.

How Chapter 13 Works When You File in Memphis

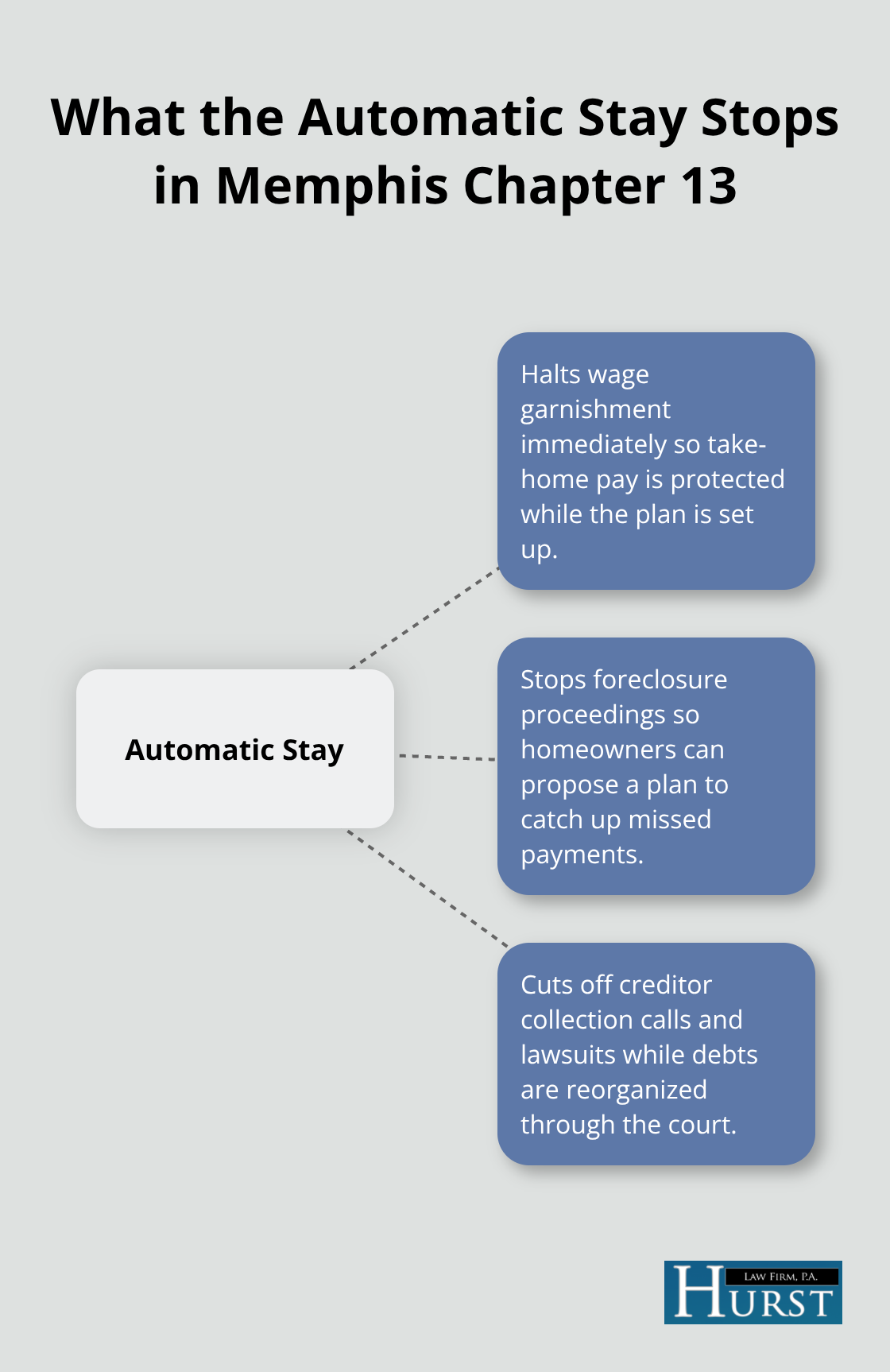

Filing Chapter 13 in Memphis triggers an immediate automatic stay that stops wage garnishment, foreclosure proceedings, and creditor collection calls the moment your petition is filed. This legal shield prevents creditors from taking further action against you while your plan gets set up. The stay doesn’t eliminate your debts-it simply halts the collection machinery so you can reorganize what you owe through the court system.

Jennifer K. Cruseturner, the Chapter 13 Trustee for the Western District of Tennessee, administers your case and manages all plan payments once your repayment schedule is approved.

Your Repayment Plan Typically Runs Three to Five Years

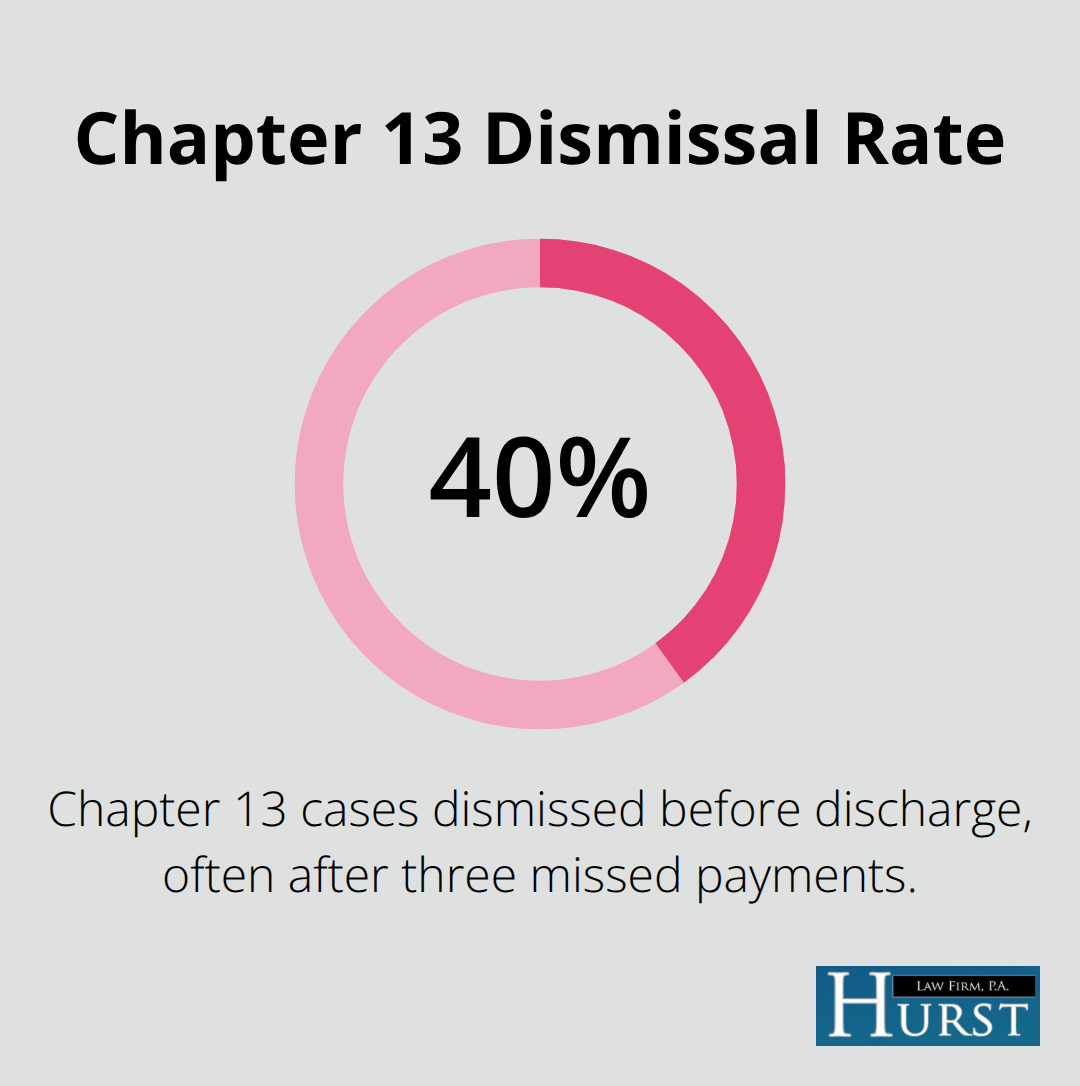

The length of your plan depends directly on your income relative to Tennessee’s median income for your household size. If your income falls below the state median, you’ll likely have a three-year plan. Higher income pushes you toward five years. During this period, you make one monthly payment to the trustee, who distributes those funds to your creditors according to bankruptcy law priorities. Priority debts like recent tax obligations and child support get paid first, secured debts like your mortgage come next, and unsecured creditors receive whatever disposable income remains. Data from the United States Courts shows roughly 40% of Chapter 13 cases are dismissed before discharge, primarily because debtors miss three consecutive payments and the plan collapses. This statistic underscores why building a realistic budget matters far more than simply accepting whatever payment the trustee proposes.

The Trustee Manages Your Case From Start to Finish

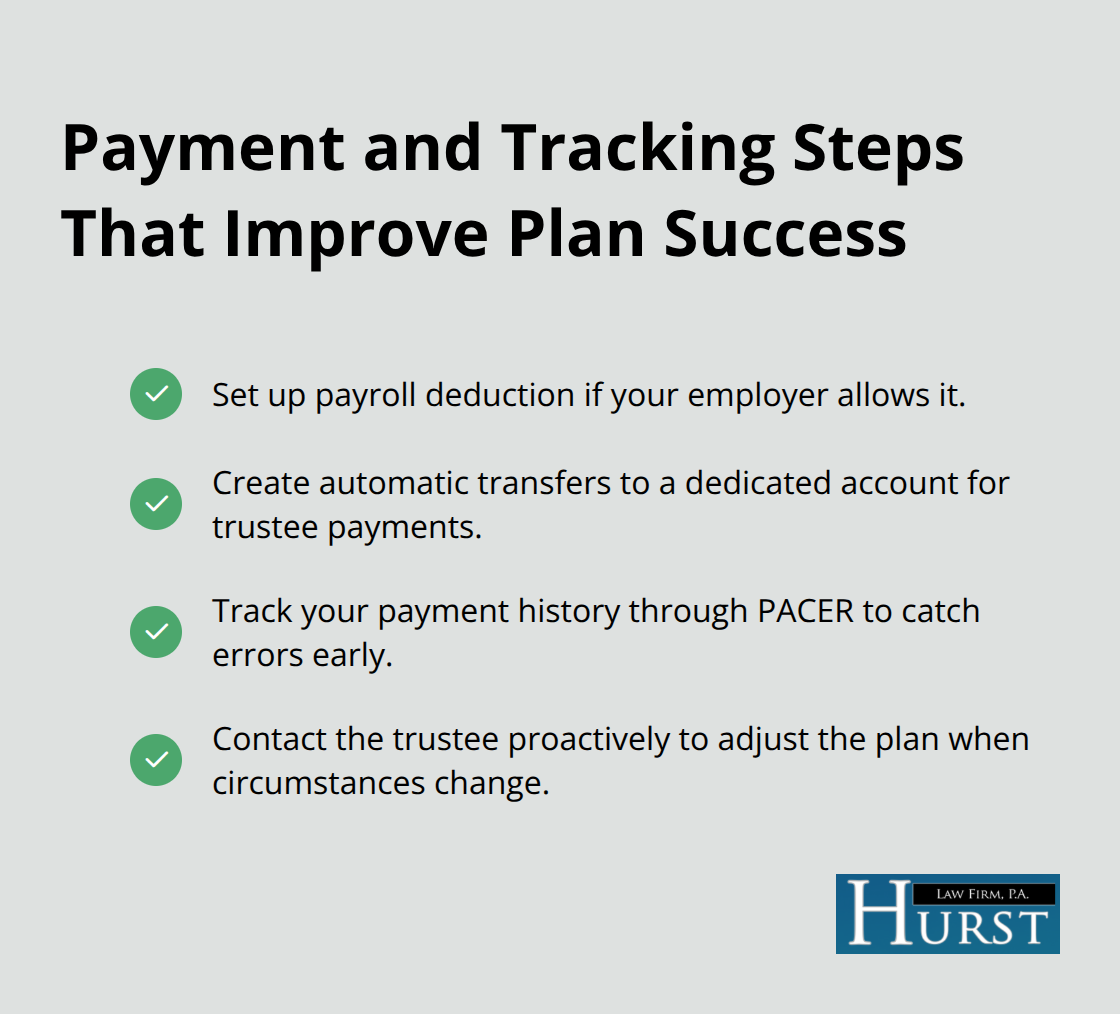

You’ll meet with Jennifer K. Cruseturner’s office at 5350 Poplar Avenue, Suite 500, Memphis, TN 38119 within 21 to 50 days after filing for your 341 creditors’ meeting. The trustee reviews your financial documents, verifies your income and expenses, and confirms whether your plan is feasible. A confirmation hearing follows roughly 45 days later, where the court approves your repayment schedule. Once confirmed, you make monthly payments either through payroll deduction or direct transfer to the trustee’s account using TFS Billpay. Tracking your payment history through PACER keeps you on top of your obligations and helps you catch any missed payments before they trigger dismissal. The trustee’s office operates Monday through Friday from 9:00 am to 3:00 pm, and you can reach the help desk at helpdesk@ch13memphis.com if you have questions about your case status or payment obligations.

Build a Budget That Survives the Full Plan Term

Most debtors who complete Chapter 13 successfully share one trait: they built their plan on actual spending data, not theoretical minimums. Pull three months of bank and credit card statements to identify what you truly spend on groceries, utilities, gas, insurance, and childcare. The Tennessee Means Test allowances (based on IRS expense standards) often underestimate real costs-grocery allowances may run around $1,200 monthly, but actual spending frequently exceeds that due to inflation and local factors. Try for a disposable income cushion of more than about $200 monthly to absorb unexpected expenses without derailing your payments. If your income rises during the plan, your payment will likely rise; if it falls, you can request a modification promptly to avoid dismissal.

What Happens When Your Plan Ends

Unsecured debts get discharged after plan completion if you follow through on all payments. Student loans and recent tax debts typically do not discharge without a rare hardship discharge. Priority claims, especially child support and alimony, must be paid in full through the plan before any distributions to unsecured creditors. Secured debts tied to collateral (your home or car) can be reorganized rather than eliminated, but you must stay current on payments to keep the property. Realistic budgeting and disciplined payment habits are the most common predictors of discharge success; underestimating expenses and failing to maintain payments are the main derailers. In Memphis, consistent action and proactive communication with your trustee are essential to avoid plan disruptions and maximize your chance of discharge. Whether Chapter 13 fits your situation or another path serves you better depends on your specific financial circumstances and goals.

Who Should File Chapter 13 in Memphis

Homeowners Who Want to Keep Their Property

Chapter 13 works best for homeowners facing foreclosure or those who have valuable assets they cannot protect under Tennessee exemptions. If you own a home with equity and want to keep it, Chapter 13 lets you catch up missed mortgage payments through your repayment plan while maintaining ownership. The automatic stay halts foreclosure immediately, giving you breathing room to reorganize. Similarly, if you own a vehicle you need for work or have other valuable property that exceeds Tennessee’s exemption limits, Chapter 13 preserves those assets while you repay debts over three to five years. This contrasts sharply with Chapter 7, which liquidates nonexempt property to pay creditors. Homeowners with significant equity often have no realistic choice but Chapter 13 if they want to keep their home and avoid losing it to creditors.

Individuals With Stable Income

You need stable income to succeed with Chapter 13. The bankruptcy code requires regular income to fund your repayment plan, and the Tennessee Means Test determines how much you can afford to pay monthly. If your income fluctuates wildly or you’re unemployed, Chapter 13 becomes unworkable because you cannot commit to consistent payments.

Stable income does not mean high income. What matters is predictability. If you receive regular paychecks, disability payments, or pension income, you likely qualify. Self-employed individuals with irregular income face steeper challenges and need detailed financial records spanning at least two years to demonstrate stability. The trustee reviews your last two years of tax returns and recent pay stubs to assess feasibility, so transparency about income fluctuations helps you build a realistic plan from the start.

People With Significant Unsecured Debt

People carrying substantial unsecured debt-credit cards, medical bills, personal loans-benefit most from Chapter 13 because unsecured creditors typically receive only 10 to 30 percent of what they are owed before the remaining balance gets discharged. This means if you owe $50,000 in credit card debt, you might repay just $5,000 to $15,000 through your plan, with the rest eliminated at discharge. That outcome becomes impossible under Chapter 7 if you lack sufficient exempt property to liquidate, since Chapter 7 requires you to pay creditors from available nonexempt assets.

Chapter 13 reorganization offers a genuine fresh start for debtors caught between too much unsecured debt and too many assets to lose safely. Whether your situation fits Chapter 13 or another path serves you better depends on your specific financial circumstances. The next section walks through how to build a repayment plan that actually works for your income and expenses.

Building a Chapter 13 Plan You Can Actually Afford

Calculate Your True Disposable Income

Your Chapter 13 plan lives or dies based on one number: disposable income. This is the money left after you pay essential expenses, and it determines your monthly trustee payment for the next three to five years. The Tennessee Means Test calculates this figure using IRS expense standards, but here’s the reality: those standards often underestimate what you actually spend. The IRS grocery allowance sits around $1,200 monthly, yet families frequently spend more due to inflation and local Memphis pricing. If you accept a plan payment based on theoretical minimums rather than real spending, you’ll miss payments within months and your case gets dismissed.

Document Three Months of Actual Spending

Pull three months of actual bank and credit card statements before meeting with the trustee. Categorize every transaction into groceries, utilities, gas, insurance, childcare, phone, internet, and transportation. This exercise reveals the truth about your budget and gives you concrete numbers to present when negotiating your plan. Try for a disposable income cushion of more than about $200 monthly beyond your proposed trustee payment. This buffer absorbs car repairs, medical copays, or other surprises that derail plans built on razor-thin margins. When you walk into the trustee’s office with three months of documented spending, you’re not guessing anymore-you’re proposing something sustainable.

Present Your Numbers to the Trustee

Jennifer K. Cruseturner’s office wants plans that survive to discharge, and that means accepting numbers grounded in your actual life. Bring recent pay stubs, mortgage statements, and your detailed expense spreadsheet to your 341 meeting. If the trustee proposes a payment that leaves you no cushion, propose a lower figure backed by your spending data. Your income may rise during the plan, which automatically increases your payment under most confirmation orders, but if income drops, file a modification request immediately rather than missing payments and triggering dismissal.

Set Up Automatic Payments and Track Progress

Set up automatic payments through payroll deduction if your employer allows it, or create automatic transfers to a dedicated account for trustee payments. Track your payment history through PACER to catch any processing errors before they become missed payments. Communication matters more than perfection-if circumstances change, contact the trustee proactively to adjust the plan rather than hoping the problem resolves itself.

Final Thoughts

Chapter 13 bankruptcy in Memphis offers something Chapter 7 cannot: the ability to reorganize your debts while keeping your home, car, and other valuable assets. Over three to five years, you rebuild financial stability through a court-approved repayment plan funded by your actual disposable income. The automatic stay stops creditors immediately, giving you breathing room to execute a realistic budget and work toward discharge.

Success hinges on one commitment: building a plan based on what you truly spend, not theoretical minimums, and maintaining those payments without exception. The 40% dismissal rate among Chapter 13 filers reflects cases where debtors underestimated expenses or failed to adjust when circumstances changed.

Those who document their spending, communicate proactively with the trustee, and treat plan payments as non-negotiable obligations reach discharge and emerge with a genuine fresh start.

Whether Memphis Chapter 13 bankruptcy fits your situation depends on your specific financial circumstances, assets, and goals. Contact Hurst Law Firm, P.A. to discuss whether Chapter 13 or another approach serves you best and to take the first step toward financial relief.