Bankruptcy stops your financial life in its tracks, but it doesn’t end it. Your credit score takes a hit, yet the damage isn’t permanent-and we at Hurst Law Firm, P.A. know exactly how to help you rebuild credit after bankruptcy.

The path forward requires concrete steps and consistent action. This guide shows you how to recover your financial standing in Memphis TN, starting today.

Understanding Your Credit After Bankruptcy

The Immediate Impact on Your Credit Score

Filing for bankruptcy triggers an immediate and significant credit score drop. A Chapter 7 filing typically causes a decline of 130 to 200 points, according to Experian data. Chapter 13 filers often experience steeper drops, sometimes falling from the high 700s to the mid-500s within weeks of filing. This shock is real and unavoidable, but here’s what matters: the damage peaks at filing and starts recovering almost immediately. You don’t spiral further downward simply because you filed. Your score bottoms out, then climbs as you demonstrate responsible financial behavior post-discharge. The emotional weight of watching your score plummet is significant, but the practical reality is that bankruptcy stops the bleeding from ongoing missed payments, collections, and mounting debt. Once you’re discharged, you’re no longer drowning in accounts marked as delinquent.

Recovery Speed Differs Between Chapter Types

Recovery speed varies between Chapter 7 and Chapter 13. After Chapter 7 discharge, roughly 60 percent of filers see measurable score improvements within 12 months, per Experian data. Your credit reports shift from showing active delinquencies and collections to showing discharged accounts, which lenders view more favorably than ongoing default. Chapter 13 filers face a slower trajectory because the bankruptcy notation remains active on your report throughout the entire repayment plan (typically lasting three to five years). During this period, your trustee restricts new credit, which limits your ability to rebuild payment history. The gap between Chapter 7 and Chapter 13 recovery is substantial: Chapter 7 filers can aggressively rebuild within months of discharge, while Chapter 13 filers must work within the constraints of an active payment plan. This doesn’t mean Chapter 13 filers can’t rebuild, but the process requires more strategic planning and patience.

Why Recent Behavior Outweighs Historical Bankruptcy

A bankruptcy notation on your credit report does fade over time. Chapter 7 bankruptcy drops off after ten years, and Chapter 13 after seven years from the filing date. However, waiting passively for time to pass wastes years of opportunity. Your post-discharge payment history is what rebuilds your creditworthiness, not the passage of time alone. Lenders evaluate your current financial behavior far more heavily than historical bankruptcy. If you discharge in 2026 and spend the next 24 months making every payment on time, maintaining low credit utilization, and avoiding new delinquencies, your score can climb into the 600s or 650s. This is the actionable insight: the bankruptcy itself becomes less relevant as your positive history accumulates. Credit bureaus weight recent payment activity more heavily than older negative marks. Your job is to create a clear pattern of reliability starting now, not waiting for 2036 to arrive.

The path to recovery starts with concrete actions you can take immediately after discharge. Secured credit cards, on-time bill payments, and careful monitoring of your credit report form the foundation of your comeback.

Practical Steps to Rebuild Your Credit

Start with a Secured Credit Card

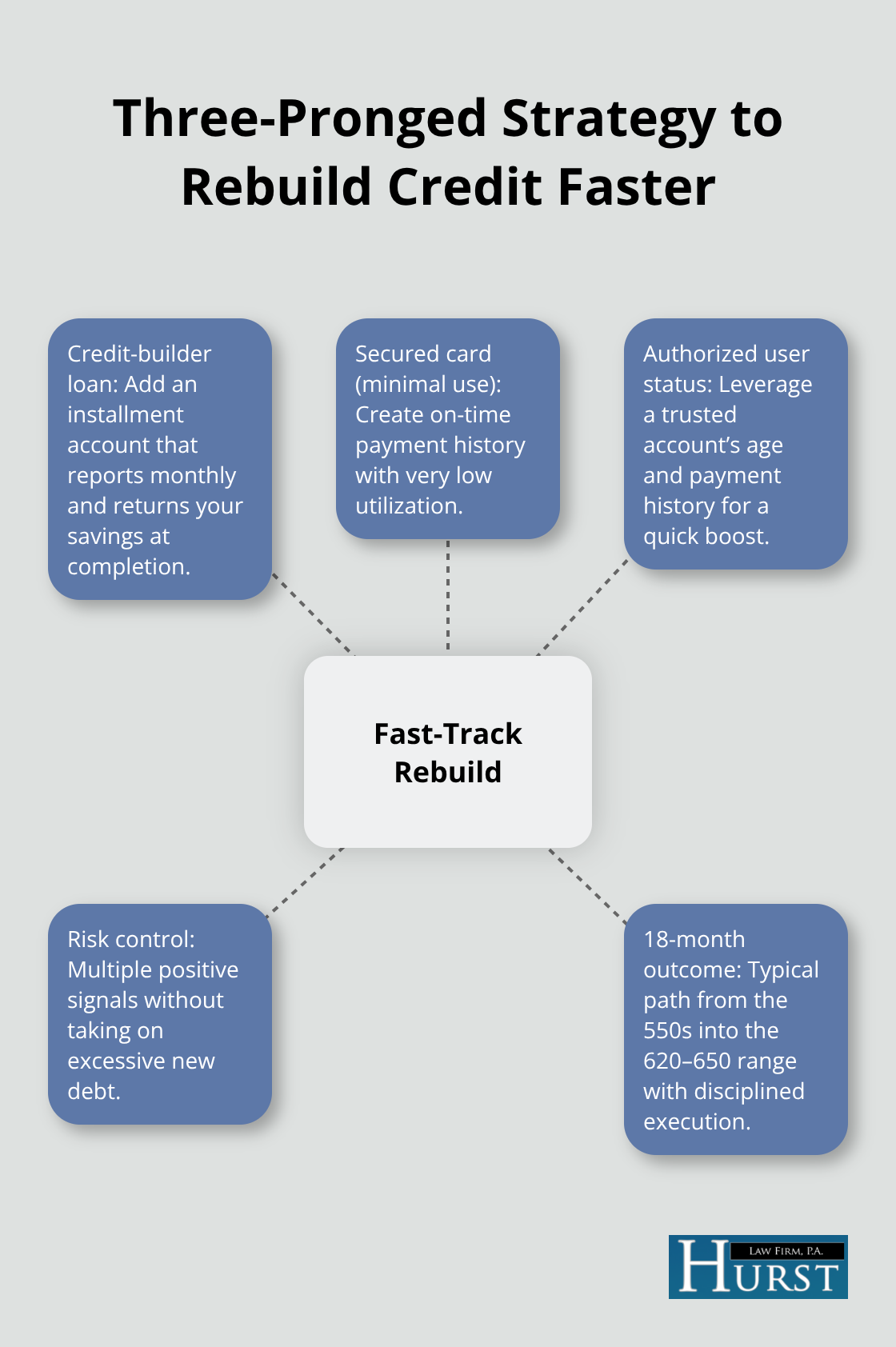

Secured credit cards offer your most direct path to demonstrating financial responsibility after discharge. Capital One and Discover both offer cards with deposits between $200 and $500 that graduate to unsecured status within 12 months if you maintain on-time payments. The deposit becomes your credit limit, which forces you to stay within bounds while establishing a clean payment history. Apply for one secured card, not three or four-multiple applications trigger hard inquiries that temporarily lower your score and signal desperation to lenders. Use the card for small, recurring charges like a monthly subscription, then pay the full balance before the statement closes. This approach keeps your utilization near zero percent while creating visible payment activity on your credit report. Avoid the temptation to max out the card or carry a balance; interest charges work against your recovery timeline and cost you money unnecessarily.

Make Every Payment on Time Without Exception

On-time payments matter more than any other single factor, accounting for 35 percent of your credit score calculation. Set up automatic payments for every bill-utilities, rent, insurance, phone, secured card minimum-so you never miss a due date regardless of circumstances. Missing even one payment after bankruptcy signals that you haven’t learned from the experience and damages your score far more severely than a pre-bankruptcy miss would have. Your credit report is also likely carrying errors that inflate your perceived risk; pull reports from Equifax, Experian, and TransUnion using AnnualCreditReport.com and dispute any inaccuracies within 30 days by submitting specific documentation to each bureau.

Identify and Challenge Reporting Errors

Creditors often report discharged accounts as missed payments even though bankruptcy eliminated the debt, creating phantom delinquencies that lenders see. When you spot these errors on your credit report, submit a dispute letter to the bureau that lists the specific inaccuracy, includes supporting documentation, and requests correction. The bureau must investigate within 30 days and remove the error if the creditor cannot verify it. This step alone can lift your score by 20 to 50 points if multiple phantom delinquencies exist on your report.

Control Your Credit Utilization Strategically

Keep your utilization on any active revolving accounts below 30 percent, though trying for under 10 percent accelerates recovery dramatically. If you have a furniture store account or other non-discharged credit line sitting at zero balance, leave it open and occasionally charge a small amount to demonstrate active credit management without accumulating new debt. This strategy shows lenders that you can access credit responsibly without overextending yourself-a critical signal as you rebuild trust in the lending community.

Strategies to Accelerate Your Financial Recovery

Build an Emergency Fund First

Your post-discharge phase presents a narrow window to rebuild aggressively. The first 12 to 24 months determine whether you’ll reach a 650 credit score within two years or languish in the 550s for five years. This is where intentional strategy separates those who recover quickly from those who stall.

An emergency fund is non-negotiable. Financial emergencies triggered 60 percent of bankruptcy filings according to American Bankruptcy Institute data, and you cannot afford another crisis derailing your progress. Start by setting aside $500 to $1,000 in a separate savings account before you tackle aggressive credit rebuilding. This buffer prevents you from reaching for credit cards when your car breaks down or medical expenses arise.

Many filers skip this step because they’re eager to prove creditworthiness through new credit accounts, but this is backwards thinking. A $1,000 emergency fund costs nothing in interest, builds discipline, and protects your credit score far more effectively than a secured card ever will. Once your fund reaches $2,500, you’ve essentially removed the bankruptcy trigger from your life.

Leverage Credit-Builder Loans Through Local Lenders

Simultaneously, explore credit-builder loans through local Memphis credit unions like Memphis City Employees Credit Union or Orion Federal Credit Union. These loans function as forced savings accounts: you borrow $500 to $1,500, make monthly payments for 12 to 24 months, and receive the full deposit at loan completion.

The payments report to all three credit bureaus, creating positive payment history without the risk of overspending. Credit-builder loans often carry lower rates than secured cards-typically 8 to 15 percent for qualified borrowers-and the psychological benefit of accumulating savings while rebuilding credit accelerates both your financial confidence and your score recovery.

Use Authorized User Status Strategically

Authorized user status on an established account with strong payment history can provide an immediate score boost of 20 to 50 points if the account holder has excellent credit and low utilization. However, this strategy requires extreme caution.

Ask a family member or spouse with a credit score above 700 and consistent on-time payment history to add you to an existing account. You don’t need to use the card-you simply need the account activity to report to your credit file. The account’s positive history transfers to your profile, which lenders perceive as evidence that responsible people trust you financially.

Avoid authorized user status on accounts with high balances or recent late payments, as this amplifies negative signals. Also skip this strategy entirely if the account holder shows signs of financial instability; their missed payment becomes your problem immediately.

Combine Multiple Strategies for Maximum Impact

The strongest combination involves pairing a credit-builder loan, a secured card used minimally, and authorized user status on one strong account. This three-pronged approach creates multiple positive signals across your credit file without exposing you to excessive debt risk.

Within 18 months, this combination typically moves filers from the 550s into the 620s to 650s range, positioning you for better credit opportunities and lower interest rates on future borrowing.

Final Thoughts

Your credit recovery after bankruptcy is measurable and real. Tracking your progress quarterly using free credit reports from AnnualCreditReport.com shows concrete improvement that builds momentum, and when your score climbs from 550 to 600, that milestone proves your strategy works. These wins demonstrate that lenders are beginning to trust you again and that your effort to rebuild credit after bankruptcy produces tangible results.

Progress creates risk, however. Many filers rebuild successfully for 18 months, then slip back into old patterns by opening too many new accounts, carrying high balances, or missing payments when unexpected expenses arise. Avoid applying for multiple credit products simultaneously, resist the urge to max out your secured card, and skip retail store cards that offer immediate discounts but carry 25 percent interest rates-these shortcuts derail your recovery trajectory.

We at Hurst Law Firm, P.A. recommend working with a financial professional as you rebuild credit after bankruptcy. A credit counselor or financial advisor can review your specific situation, identify risks unique to your circumstances, and adjust your strategy as your credit improves, preventing costly mistakes and accelerating your path to financial stability.