Chapter 13 bankruptcy offers a structured path to manage your debts while keeping your assets. If you’re considering this option, understanding how a Chapter 13 plan works is the first step toward financial stability.

We at Hurst Law Firm, P.A. created this guide to help you learn the Chapter 13 plan process from start to finish. You’ll find practical information about repayment timelines, income calculations, and how to handle plan modifications.

What Chapter 13 Actually Is

A Chapter 13 plan is a court-approved repayment structure that lets you reorganize your debts over three to five years while keeping your property. Unlike Chapter 7 bankruptcy, which liquidates assets to pay creditors, Chapter 13 keeps you in control of your belongings and gives you a realistic path to catch up on missed payments. The court appoints a trustee who collects one monthly payment from you and distributes it to your creditors according to the plan. This single payment replaces the stress of juggling multiple creditors and collection calls. Chapter 13 works best when you have steady income and want to preserve assets like your home or vehicle.

Income Requirements and Debt Limits

You qualify for Chapter 13 if your unsecured debts do not exceed $526,700 and your secured debts stay under $1,580,125 as of your filing date. These limits adjust periodically for inflation, so your situation might qualify even if you initially thought you couldn’t file. More importantly, you must have regular income from employment, self-employment, or another reliable source to fund a repayment plan. The court evaluates your current monthly income against your state’s median income for a family of your size. If your income falls below the state median, your plan typically runs three years; if above, the plan extends to five years. Most people disqualify themselves mentally before consulting an attorney, but the actual eligibility rules are more flexible than they assume.

Chapter 13 Versus Chapter 7

Chapter 7 bankruptcy erases most unsecured debts but requires you to surrender non-exempt assets, and it stays on your credit report for ten years. Chapter 13 keeps your assets intact and shortens your credit reporting period to seven years, making it the stronger choice if you own a home, car, or have significant personal property. With Chapter 13, you control the repayment process and can modify your plan if your income changes or unexpected expenses arise. Chapter 7 offers faster relief-typically four to six months-but Chapter 13 gives you the advantage of catching up on mortgage arrears, stopping foreclosure, and restructuring car loans into manageable payments. If you have a steady income and want to keep your property, Chapter 13 is almost always the better option than Chapter 7.

How Your Plan Takes Shape

Once you determine that Chapter 13 fits your situation, the next step involves understanding how the court structures your actual repayment plan. Your trustee calculates what you can realistically pay each month based on your income and necessary living expenses. The plan then allocates your monthly payment across priority debts (like recent taxes and child support), secured debts (like mortgages and car loans), and unsecured debts (like credit cards and medical bills). This structured approach means you know exactly where your money goes and creditors receive payments in a predictable order. Understanding these mechanics helps you prepare for what comes next in your Chapter 13 journey.

How Your Chapter 13 Plan Works

Your Chapter 13 plan runs for either three or five years, and this duration hinges on one critical factor: whether your current monthly income exceeds your state’s median income for a family of your size. If you earn below the median, your plan typically lasts 36 months. If you exceed the median, the court requires a five-year commitment unless you can pay all your debts faster. This income threshold matters because the law assumes higher earners have more disposable income available for creditors. The court calculates your current monthly income by averaging your gross income from the past six months, not your actual take-home pay. This means someone earning $4,500 per month qualifies for a three-year plan in most states, while someone earning $5,200 monthly faces the five-year requirement. The timing affects your total monthly payment-shorter plans demand higher payments, while longer plans reduce the monthly burden but extend your commitment period. Neither option is inherently better; the right choice depends on your cash flow and how quickly you want to finish your repayment obligation.

Calculating What You Actually Owe Each Month

Disposable income is the number that determines your monthly payment, and it’s calculated by subtracting your reasonable living expenses from your gross monthly income. The court uses standardized expense figures from the IRS for categories like housing, food, transportation, and utilities, though you can justify higher amounts if you provide documentation. If you spend $2,000 monthly on necessary expenses and earn $3,500, your disposable income is $1,500-that’s what goes toward your plan payment. This calculation is not negotiable; the trustee and court will scrutinize your budget line by line. Claiming $400 monthly for groceries when you live alone will face objections, while documenting actual childcare costs or medical expenses strengthens your case. The difference between a realistic budget and an inflated one can mean the difference between a feasible plan and one the court rejects. Start gathering receipts, bank statements, and expense records now to build an accurate picture of your spending. Overestimating expenses leads to plan failure; underestimating them wastes money you could keep.

What Actually Goes Into Your Repayment Plan

Your monthly payment flows to the trustee, who distributes it according to a strict priority order established by bankruptcy law. Priority debts receive payment first-these include recent income taxes, child support, alimony, and trustee fees. Secured debts come next, which means your mortgage arrears, car loans, and any other debts backed by collateral. Unsecured debts like credit cards and medical bills receive whatever remains after priority and secured claims are addressed. This structure protects your home and vehicle because the plan prioritizes catching up on those payments while also satisfying creditors. If you owe $8,000 in mortgage arrears and $15,000 in credit card debt, your plan spreads the mortgage arrears across the full three or five years while creditors receive partial payments on the credit cards. The amount unsecured creditors receive depends entirely on your disposable income and plan length. Someone with $500 monthly disposable income over five years pays $30,000 total, which might satisfy all priority and secured claims while paying unsecured creditors 30 cents on the dollar. The court confirms your plan only if it meets the best interests test, meaning unsecured creditors receive at least what they would receive if you filed Chapter 7 instead. Understanding this priority system helps you anticipate what your creditors will actually receive and whether your plan is realistic.

How the Court Confirms Your Plan

The court will not approve your plan unless it satisfies specific legal requirements. Your plan must show that you can feasibly complete it based on your projected income and expenses over the full three or five years. The trustee and any creditors can object to your plan if they believe your budget is unrealistic or your proposed payments are too low. You must also file all required tax returns for the past four years and complete a credit counseling course within 180 days before you file. The confirmation hearing typically occurs within 45 days after your meeting with the trustee, and the court will ask you questions about your finances and your ability to make the proposed payments. If the court confirms your plan, you and your creditors are bound by its terms, and you cannot incur new debt without trustee or court permission. This confirmation process ensures that your plan is both legally sound and financially achievable, setting you up for success over the next three to five years.

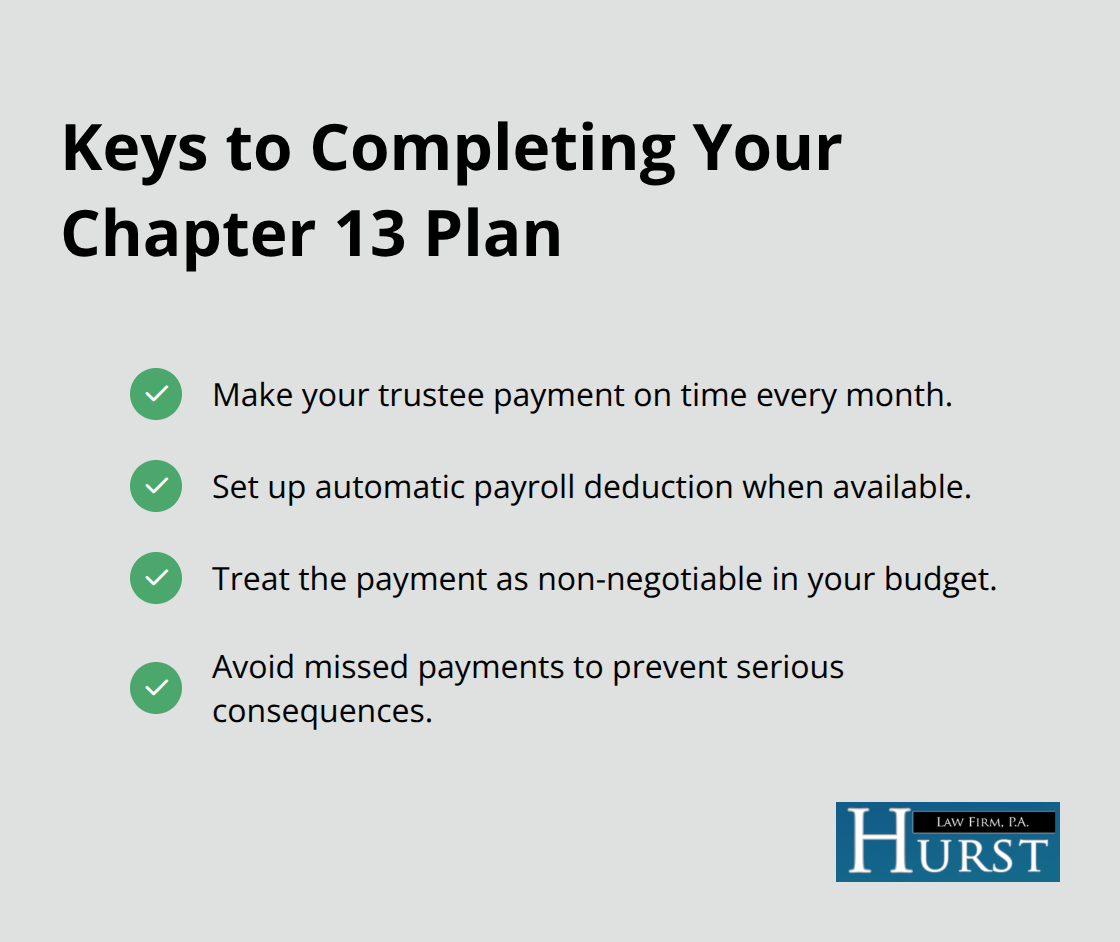

Managing Your Chapter 13 Plan Successfully

Your Chapter 13 plan succeeds or fails based on one simple reality: you must make your monthly payment to the trustee on time, every single month, for the entire three to five years. The trustee does not care about your excuses or circumstances; the payment is non-negotiable. Set up automatic payroll deduction if your employer allows it, because the Federal Judiciary reports that debtors who use payroll deduction have significantly higher completion rates than those who pay manually. Missing even one payment creates serious consequences, so treat this obligation with the same priority you would give to keeping the lights on or feeding your family.

Making Consistent Monthly Payments

The payment amount remains fixed unless you petition the court for a modification, so your budget must account for this expense before you allocate money to anything else. Many debtors fail their plans not because they cannot afford the payment, but because they deprioritize it in favor of discretionary spending. Your Chapter 13 payment is a legal obligation backed by the full authority of the federal court, and the trustee will move to dismiss your case if payments fall behind. Automatic payroll deduction eliminates the risk of accidental late payments and removes the temptation to spend money earmarked for your plan.

What Happens If You Miss a Payment

If your income drops unexpectedly or your expenses spike beyond what you anticipated during plan confirmation, the law allows you to modify your plan rather than abandon it entirely. You cannot simply stop paying and hope the trustee forgets; instead, you must file a formal modification request with the court explaining the changed circumstances. The court will hold a hearing to examine your new budget and determine whether your modified payment is still feasible. A job loss, medical emergency, or significant increase in childcare costs all qualify as legitimate grounds for modification, but the court will require documentation to verify your claims.

Modifying Your Plan When Circumstances Change

Modifying your plan takes time and costs money in attorney fees, so many debtors struggle through temporary hardship rather than pursue formal relief. If your situation improves later (you receive a raise or an unexpected inheritance), the court can increase your payment accordingly, though creditors rarely push for this modification. The critical point is that modification exists as a safety valve, not an escape hatch; you cannot modify your plan down to near-zero and expect the court to accept it. Your plan must still satisfy the best interests test and commit your disposable income to creditors. If modification proves impossible because your circumstances have deteriorated beyond recovery, the court may dismiss your case entirely, leaving you without bankruptcy protection and exposed to collection actions once again.

Final Thoughts

Chapter 13 bankruptcy is not a quick fix, but it is a realistic path forward when you have steady income and want to keep your assets. The three to five year commitment requires discipline and consistency, but thousands of people complete their plans every year and emerge with their homes, vehicles, and financial dignity intact. When you learn Chapter 13 plan mechanics, you understand that your monthly payment is non-negotiable, your budget must be honest, and modification exists only when genuine hardship strikes.

If you are facing foreclosure, repossession, or overwhelming collection calls, waiting another month only narrows your options. If you have steady income and want to reorganize your debts rather than liquidate your assets, Chapter 13 deserves serious consideration. The sooner you consult with a bankruptcy attorney, the sooner you can evaluate whether this path makes sense for your specific situation.

We at Hurst Law Firm, P.A. understand the financial stress that leads people to consider Chapter 13, and we know how to structure a plan that actually works for your life. We offer a free consultation to discuss your debts, income, and goals without pressure or judgment. Contact us today to learn whether Chapter 13 is the right choice for your financial recovery.