Losing your car during bankruptcy feels inevitable, but it doesn’t have to happen. Chapter 13 bankruptcy offers concrete tools to keep your vehicle while you reorganize your debts.

We at Hurst Law Firm, P.A. help Memphis TN residents navigate car loans during bankruptcy and protect their transportation. This guide shows you exactly how Chapter 13 works in your favor.

How Chapter 13 Bankruptcy Protects Your Vehicle

Chapter 13 bankruptcy stops repossession immediately through the automatic stay, a court order that activates the moment you file. Lenders must halt collection efforts, including repossession proceedings, giving you breathing room to catch up on missed payments. This protection lasts throughout your entire repayment plan, which typically runs three to five years. If a lender has already repossessed your vehicle, filing Chapter 13 promptly opens the door to recover it and restart payments within your plan. The automatic stay applies to all creditors simultaneously, so your car lender cannot continue collection activities while you reorganize your finances.

Reducing What You Actually Owe

A cramdown under Chapter 13 addresses the painful reality of owing more than your car is worth. If your vehicle’s current market value falls below your loan balance and you have owned the car for more than 2.5 years, the court can reduce your secured debt to match the car’s actual value. This means if you owe $12,000 on a vehicle worth $9,000, a cramdown restructures your plan so you pay only $9,000 as secured debt. The remaining $3,000 becomes unsecured debt, treated like credit card obligations and often discharged at the end of your plan. Lower secured debt directly translates to lower monthly payments, making vehicle retention financially realistic for many filers.

Structuring Payments That Work for Your Budget

Your Chapter 13 plan treats your car loan as a priority secured debt, meaning the court ensures you can stay current on payments while addressing other obligations. The trustee works with you to create a realistic budget that covers the vehicle loan alongside other debts, rather than forcing you to choose between the car and survival expenses. You continue making regular monthly payments on the car while catching up on any past-due amounts through your plan, typically over the full three to five year period. Court oversight prevents aggressive creditor tactics and ensures your plan remains affordable based on your actual income and expenses. This structured approach gives you legal protection that informal negotiations with lenders simply cannot provide.

Moving Past Financial Obstacles

The real challenge emerges when you face obstacles that threaten your ability to keep the vehicle. Underwater loans, lender objections, and multiple vehicle obligations can complicate your Chapter 13 plan, but each presents solutions that work within the bankruptcy framework. Understanding these obstacles before they arise helps you prepare your plan and communicate effectively with your trustee about what you need to protect your transportation.

How to Keep Making Payments During Chapter 13

Your Chapter 13 plan does not eliminate your car payment. Instead, it integrates your vehicle loan into a court-approved structure that lets you stay current while catching up on past-due amounts. The trustee calculates what you can afford each month based on your actual income and necessary expenses, then divides that amount among your creditors according to priority. Your car payment remains a secured debt, meaning it gets paid before unsecured debts like credit cards. You continue making regular monthly payments to your lender throughout the entire three to five year plan, and these payments are reported to credit bureaus, helping rebuild your credit history during bankruptcy. Staying current on your vehicle payment is non-negotiable if you want to keep the car, so your budget must accommodate this obligation before the court approves your plan.

Understanding Your Payment Structure

If your income fluctuates or your circumstances change, you can file a plan modification to adjust payments, but lenders will scrutinize any request that reduces their payment amount. The court will not approve a plan that leaves you unable to cover your car loan alongside essential living expenses. Your trustee collects one monthly payment from you that covers all your debts, then distributes the funds according to your plan. This means you do not send separate payments to your car lender during bankruptcy-the trustee handles the distribution on your behalf.

Securing Court Approval for Modified Terms

Cramdowns and plan modifications require court approval, which means your trustee and the lender both get a say in whether your proposal is reasonable. If you pursue a cramdown, the lender typically objects because they lose money when the secured debt drops to the vehicle’s actual value. You must prove the car’s fair market value through documentation like Kelley Blue Book or NADA Guides, and the lender will often present their own valuation to dispute your figure. The court weighs both sides and makes the final decision, but having solid documentation of your car’s value strengthens your position considerably.

Plan modifications face similar scrutiny, particularly if you request to reduce car-related expenses or extend your payment timeline. Lenders challenge modifications claiming the expenses are unreasonable, so you must demonstrate that your car costs are necessary for work and family needs, not luxuries. If you own an expensive vehicle or a second car, expect stronger objections unless you can prove both are essential for employment or childcare. The timing of your modification request also matters-filing it early in your plan, before you have missed payments, carries more weight than requesting changes after falling behind. Working with your trustee to present a realistic, well-documented proposal gives you the best chance of approval.

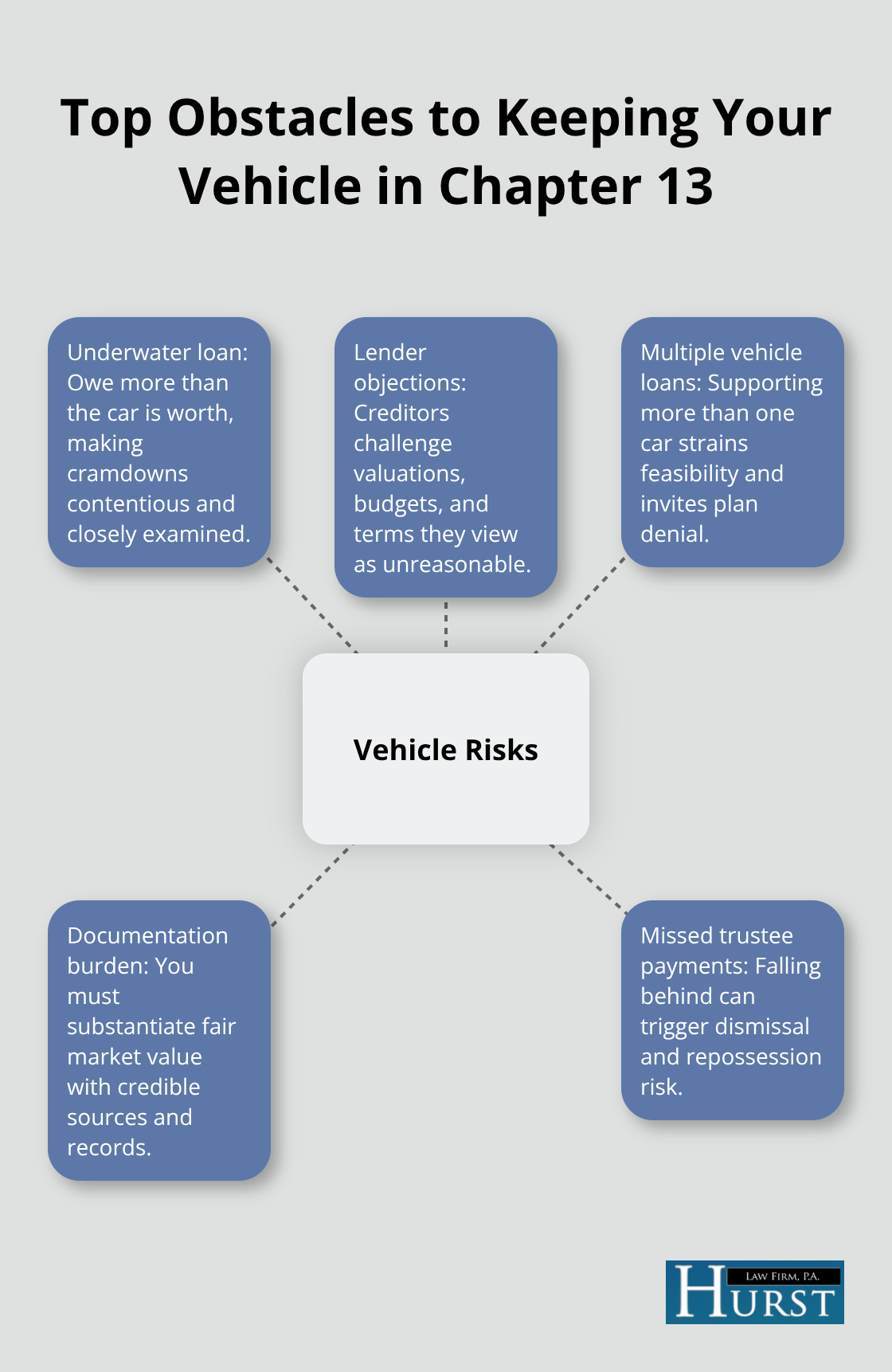

Prioritizing Your Trustee Payment

Missing your trustee payment jeopardizes your entire plan, including your vehicle protection, because the lender can move to dismiss the bankruptcy if you fall behind. Even one missed payment can trigger a lender objection or a motion to dismiss, so treating your trustee payment as your highest priority is essential. Set up automatic payments from your bank account to avoid accidental delays, and contact your trustee immediately if you anticipate difficulty making a payment. Some trustees allow temporary payment deferrals or modifications if you face a temporary income loss, but these require advance notice and approval.

Once you miss a payment, recovery becomes complicated and expensive, potentially costing you the vehicle and the entire bankruptcy protection. Staying current on your trustee payment is the single most practical action you can take to guarantee you keep your car through Chapter 13. The obstacles that threaten your ability to maintain these payments-underwater loans, lender objections, and multiple vehicle obligations-require specific strategies to overcome, and understanding them before they arise positions you to protect your transportation effectively.

Real Obstacles That Threaten Your Vehicle in Chapter 13

Underwater Car Loans and the Cramdown Challenge

Underwater car loans present the most stubborn problem you’ll face in Chapter 13, and cramdowns don’t solve them as cleanly as the law suggests. You qualify for a cramdown only if you’ve owned the vehicle for more than 2.5 years, which eliminates many filers who purchased recently or financed through a buy-here-pay-here dealer. Even when you qualify, lenders fight aggressively because they lose money when the court reduces your debt to the car’s actual value. If you owe $15,000 on a vehicle worth $10,000, the lender loses $5,000 in secured debt, and they will hire their own appraiser to challenge your valuation.

You must document your car’s fair market value using Kelley Blue Book, NADA Guides, or a professional appraisal, and the court accepts whichever valuation is most credible. Lenders typically argue that your vehicle’s condition justifies a higher value than market data suggests, so photographs and maintenance records strengthen your valuation considerably. The cost of defending a cramdown through trial can reach $1,500 to $3,000 in attorney fees, which eats into your savings and complicates your plan approval.

Managing Lender Objections to Your Plan

Lender objections emerge when your plan proposes car expenses that the trustee or creditor considers unreasonable for your income level and circumstances. If you earn $3,500 monthly and your car payment consumes $700 of that, you’re spending 20 percent of gross income on vehicle debt alone, which courts view skeptically. Adding insurance, fuel, and maintenance pushes vehicle costs higher, and lenders challenge plans where these expenses exceed what’s necessary for work and childcare.

Owning a second vehicle or keeping an expensive car triggers immediate objections unless you prove both are essential for employment or family needs. A rideshare driver or someone with multiple jobs might justify a second reliable vehicle, but a luxury sedan or truck financed at 15 percent interest raises red flags. Your trustee will push back if your plan doesn’t account for realistic car maintenance costs (which average $500 to $1,000 annually according to AAA data), and lenders exploit vague budget categories to argue you’re hiding expenses.

Handling Multiple Vehicle Loans

Managing multiple vehicle loans within one plan compounds these challenges because the court must approve payments for each loan while ensuring you can cover all other obligations. If you own two cars and owe $25,000 across both loans, your plan must demonstrate you can pay both vehicles while handling credit card debt, back taxes, or medical bills. Courts rarely approve plans that carry two vehicle loans unless one is nearly paid off or the second vehicle generates income.

The practical solution involves surrendering the second vehicle, refinancing one loan outside bankruptcy to reduce plan obligations, or waiting until your income increases before filing. Evaluating whether keeping multiple vehicles through Chapter 13 is realistic for your specific income and debt load is essential, because filing with an unaffordable plan guarantees dismissal and immediate repossession risk.

Final Thoughts

Chapter 13 bankruptcy protects your vehicle when you stay committed to your plan and communicate honestly with your trustee. The automatic stay stops repossession immediately, cramdowns reduce what you owe on underwater loans, and court-supervised payments make car loans during bankruptcy manageable. Your trustee calculates what you can realistically afford each month and structures your plan so your car payment receives priority alongside essential living expenses.

Lenders will object to cramdowns and challenge plan modifications, but solid documentation of your vehicle’s value and transparent budgeting overcome most objections. Missing even one trustee payment jeopardizes your entire plan and invites immediate lender action, so automatic payments from your bank account protect your vehicle more effectively than any legal argument. If you own multiple cars or drive an expensive vehicle, prepare to justify why both are necessary for work or childcare.

We at Hurst Law Firm, P.A. help Memphis TN residents navigate Chapter 13 bankruptcy and protect their vehicles through this process. Contact us to discuss whether Chapter 13 works for your situation and how to structure a plan that keeps your car while you rebuild your financial foundation.