Debt can feel overwhelming, but you don’t have to face it alone. When you consult a bankruptcy attorney today, you gain access to someone who understands Memphis TN bankruptcy law and can guide you toward real solutions.

At Hurst Law Firm, P.A., we help people navigate Chapter 7 and Chapter 13 options to find the path that works for their situation. Your first consultation is the moment everything changes.

Your First Consultation Explained

Gathering Your Financial Documents

When you come to Hurst Law Firm, P.A. for your initial consultation, we ask you to bring specific documents that paint a complete picture of your finances. Bring recent pay stubs, six months of bank statements, a list of creditors with amounts owed, property deeds or leases, recent tax returns, and a breakdown of your monthly expenses. These documents reveal exactly where you stand financially-this isn’t busywork but the foundation of your strategy.

Understanding What You Own and Owe

We examine your income sources, whether that’s wages, retirement income, or other steady money coming in each month. We also identify what you own: your home equity, vehicle equity, household items, and retirement accounts. Federal law through Title 11, the Bankruptcy Code, protects certain assets through exemptions, and understanding what you can keep matters enormously. We then review every debt you’re carrying-credit card balances, medical bills, mortgage arrears, tax debt, car loans, and personal loans. Some debts can be eliminated entirely; others, like student loans, typically cannot be discharged in bankruptcy. Knowing the difference shapes your entire strategy.

Presenting Your Options Clearly

Once we understand your complete financial picture, we present your options honestly. Chapter 7 bankruptcy liquidates unsecured debts and typically concludes in three to four months, though most consumer cases involve little or no asset liquidation because exemptions protect what matters most. Chapter 13 restructures your debts into a court-approved repayment plan spanning three to five years, allowing you to catch up on mortgage or car payments while keeping your home and vehicle. The automatic stay takes effect immediately upon filing, stopping wage garnishment, collection calls, lawsuits, and foreclosure actions right away.

Understanding Costs and Timeline

We explain the costs involved-bankruptcy filing fees vary, but many attorneys offer flexible payment plans-and what the timeline looks like from filing through discharge. We answer your specific questions about how bankruptcy affects your credit, what happens at the 341 meeting of creditors, and what debtor education courses you’ll need to complete. This consultation removes the guesswork and positions you to move forward with confidence.

Why You Need a Memphis Bankruptcy Attorney

Bankruptcy law is federal law under Title 11, the Bankruptcy Code, and cases must be filed in bankruptcy court, not state court, according to the U.S. Courts. The process involves strict deadlines, specific forms, credit counseling requirements, trustee requests, and court procedures that trip up people who try to navigate them alone. One missed deadline or incomplete form can delay your discharge by months or cost you thousands in additional fees. A Memphis bankruptcy attorney familiar with Memphis bankruptcy court knows the local judges, trustees, and procedural expectations that make the difference between a smooth filing and a frustrating one. Hurst Law Firm, P.A. handles the paperwork correctly the first time, files your petition in the right court, and manages every deadline so nothing falls through the cracks.

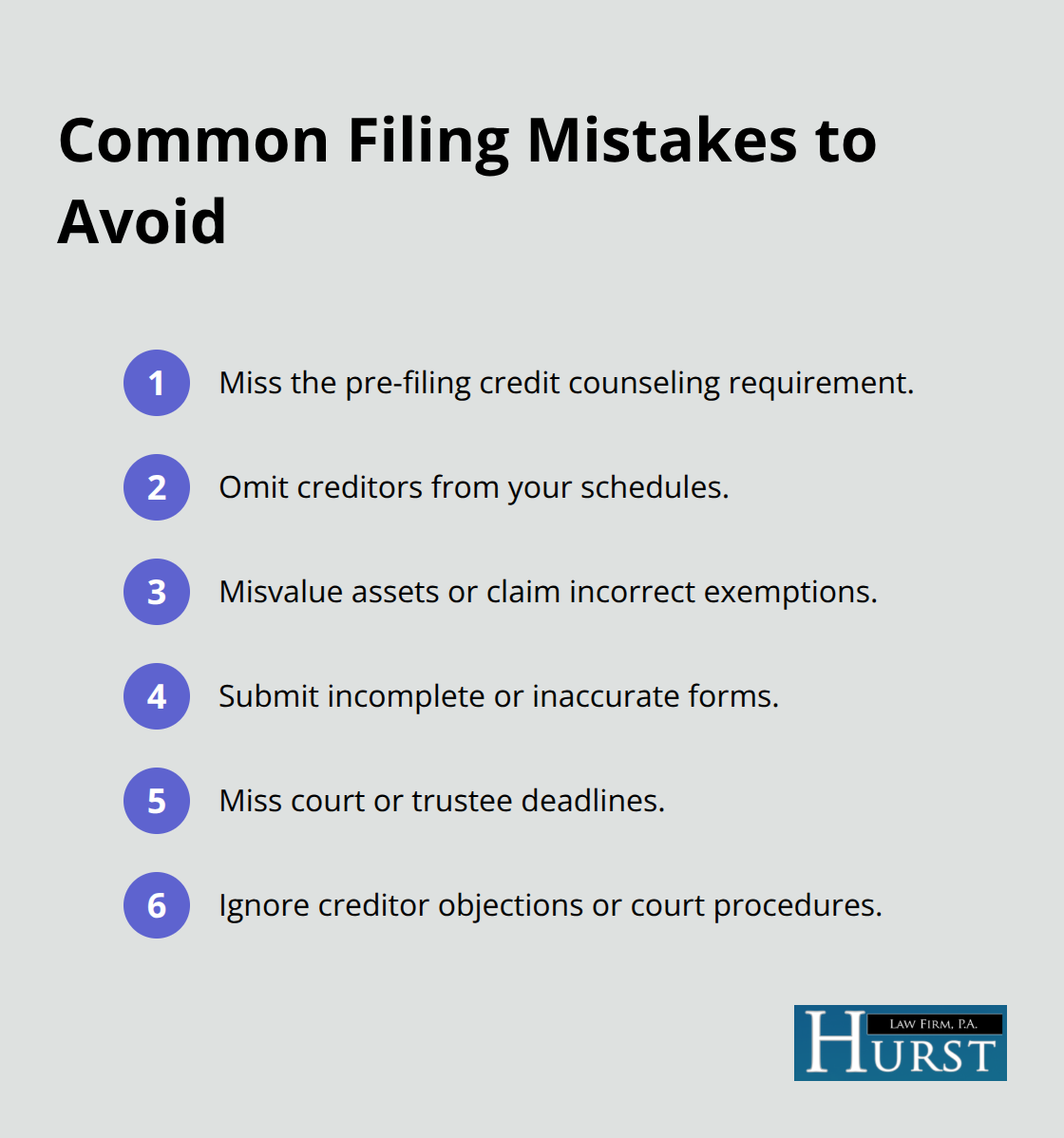

Errors That Compromise Your Case

People who file without an attorney often make errors that compromise their case. Missing the credit counseling deadline before filing results in automatic dismissal. Failing to list all creditors means some debts won’t be discharged, leaving you liable after bankruptcy ends. Incorrectly valuing assets or claiming wrong exemptions leads to loss of property you thought was protected.

The U.S. Courts note that disputes arise about ownership or value of property, the amount owed, or dischargeability of debts, and litigation in bankruptcy follows the same procedures as civil cases with discovery, pretrial proceedings, and trials. When you handle these issues without counsel, creditors challenge your claims, and you face them alone in court. An attorney presents your case properly, responds to creditor objections, and protects your interests before the judge.

Immediate Protection Through Filing

Filing bankruptcy triggers an automatic stay that stops wage garnishment, collection calls, lawsuits, and foreclosure actions immediately upon filing. This protection gives you breathing room, but only if your petition is filed correctly. The automatic stay applies to most creditors and collection efforts, providing the immediate relief you need while your case proceeds through the bankruptcy system.

Long-Term Strategy That Fits Your Situation

Beyond the immediate relief, your attorney builds a strategy for your specific situation. Chapter 7 cases require passing a means test to qualify, and Chapter 13 cases demand a feasible repayment plan that the court will confirm. An experienced attorney knows which chapter positions you best, how to structure your plan to maximize asset protection, and how to handle complications like joint debts, recent job loss, or prior bankruptcy filings. Local knowledge of Tennessee law and Memphis court practices shapes how your case moves forward and what outcomes you can realistically expect.

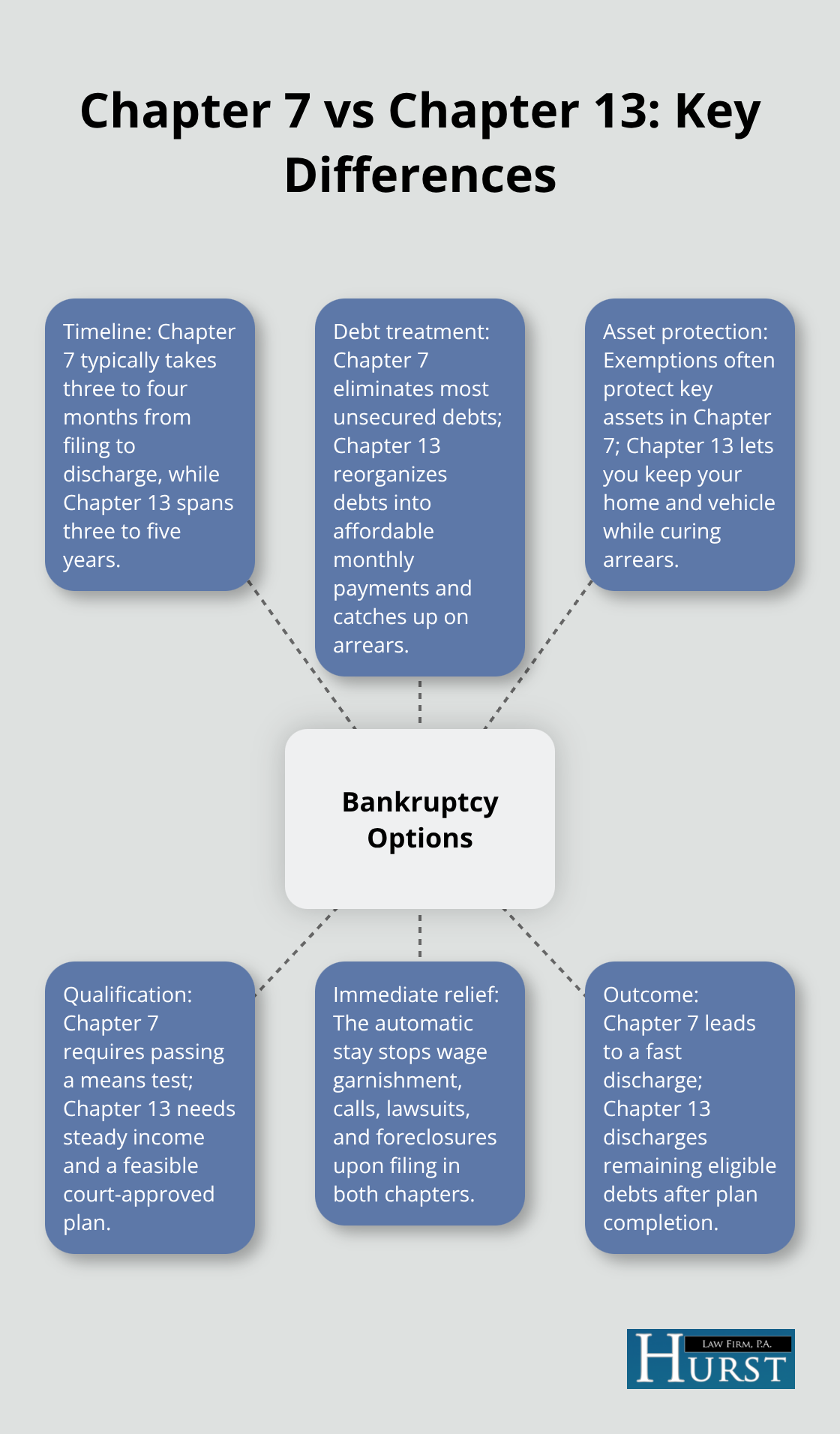

Chapter 7 vs Chapter 13: Which Bankruptcy Path Fits Your Finances

Chapter 7: Fast Debt Elimination

Chapter 7 bankruptcy moves fast and erases most unsecured debts within three to four months after filing. You liquidate non-exempt assets to pay creditors, though in most consumer cases the exemptions under federal law and Tennessee state law protect your home equity, vehicle equity, household goods, and retirement accounts so completely that creditors receive little or nothing. This speed matters enormously when you’re drowning in credit card debt, medical bills, or personal loans. The U.S. Courts reports that in many consumer liquidation cases, there is little or no money available in the debtor’s estate to pay creditors, and the debtor receives a discharge of most debts without objection.

Qualifying for Chapter 7

You must pass a means test to qualify for Chapter 7, which compares your income against the median income in Tennessee for your household size. If your income falls below the median, you qualify immediately. If it exceeds the median, the means test applies expenses and calculates whether you have disposable income to fund a Chapter 13 plan instead. The entire process from filing to discharge typically takes three to four months, making Chapter 7 the fastest path to a fresh start when you qualify.

Chapter 13: Restructured Repayment

Chapter 13 restructures your debts into a court-approved repayment plan spanning three to five years. You keep your home and car by continuing to make regular payments on them while the plan catches up on any arrears and reorganizes everything else into affordable monthly installments. This chapter works when you have steady income from wages, retirement distributions, or other reliable sources and you want to preserve assets that Chapter 7 might force you to liquidate.

What Chapter 13 Covers

The plan covers credit card debt, medical bills, tax debt, and personal loans while protecting your equity in property. Student loans typically cannot be discharged in either chapter, so they remain your responsibility after bankruptcy ends. Your monthly payment under the Chapter 13 plan depends on your income, the total amount of debt, and what assets you’re protecting.

Completion and Discharge

Once you complete the plan and make all payments as required, the court discharges remaining eligible debts at the end of the three to five year period. At Hurst Law Firm, P.A., we help you understand which chapter positions you best based on your income, debts, assets, and goals for protecting your home or vehicle.

Final Thoughts

The path to financial freedom starts with one decision: to consult a bankruptcy attorney today. When you contact Hurst Law Firm, P.A., you take control of your financial future instead of letting debt control you. Prepare your pay stubs, bank statements, tax returns, creditor lists, and expense breakdown before your meeting so we can build your strategy immediately.

We file your petition in the correct bankruptcy court, manage every deadline, and guide you through the 341 meeting of creditors. The automatic stay protects you from wage garnishment and collection calls while your case moves forward, and we handle creditor objections so you face them with representation. Whether Chapter 7 or Chapter 13 fits your situation, we structure your filing to maximize what you keep and minimize what you owe.

We at Hurst Law Firm, P.A. understand Tennessee bankruptcy law and Memphis court procedures that affect your case. Your fresh start becomes a concrete outcome we work toward every day. Contact us today to schedule your free initial consultation and begin moving toward the financial relief you deserve.