Hiring the wrong bankruptcy attorney can cost you thousands in unnecessary fees and delays. A Memphis bankruptcy attorney consultation gives you the chance to evaluate whether someone truly understands your situation and can guide you through Chapter 7 or Chapter 13 bankruptcy effectively.

At Hurst Law Firm, P.A., we’ve seen clients make costly mistakes by not asking the right questions upfront. This guide walks you through the essential questions that separate qualified attorneys from those who won’t fight for your financial fresh start.

What Questions to Ask About Your Bankruptcy Attorney’s Experience

Hiring the wrong bankruptcy attorney can cost you thousands in unnecessary fees and delays. A Memphis bankruptcy attorney consultation gives you the chance to evaluate whether someone truly understands your situation and can guide you through Chapter 7 or Chapter 13 bankruptcy effectively.

Local Court Experience Matters

When you call a bankruptcy attorney in Memphis, TN, ask about their actual caseload in your area first. Local experience matters significantly because bankruptcy courts operate under specific procedures, and judges in the Western District of Tennessee have distinct preferences about how cases should be handled. An attorney who primarily serves clients in Nashville or Knoxville will lack the nuanced understanding of Memphis bankruptcy court dynamics that protects your interests.

Ask directly: How many Chapter 7 and Chapter 13 cases have you filed in Memphis specifically over the last three years? The answer should be substantial-ideally dozens per year. Attorneys handling fewer than 20 cases annually in your jurisdiction lack the volume needed to stay current with local rule changes and judicial trends.

Beyond raw numbers, ask whether the attorney personally appears at the 341 meetings or sends paralegals instead. You need someone who will stand beside you at that critical meeting, not someone delegating your case to support staff who may lack authority to negotiate or respond to trustee concerns on the spot.

Chapter 7 Versus Chapter 13 Selection

The bankruptcy chapter you file under-Chapter 7 or Chapter 13-fundamentally changes your case trajectory and outcomes. Some attorneys push every client toward Chapter 13 because it generates higher fees, while others default to Chapter 7 regardless of whether it protects your home or vehicle.

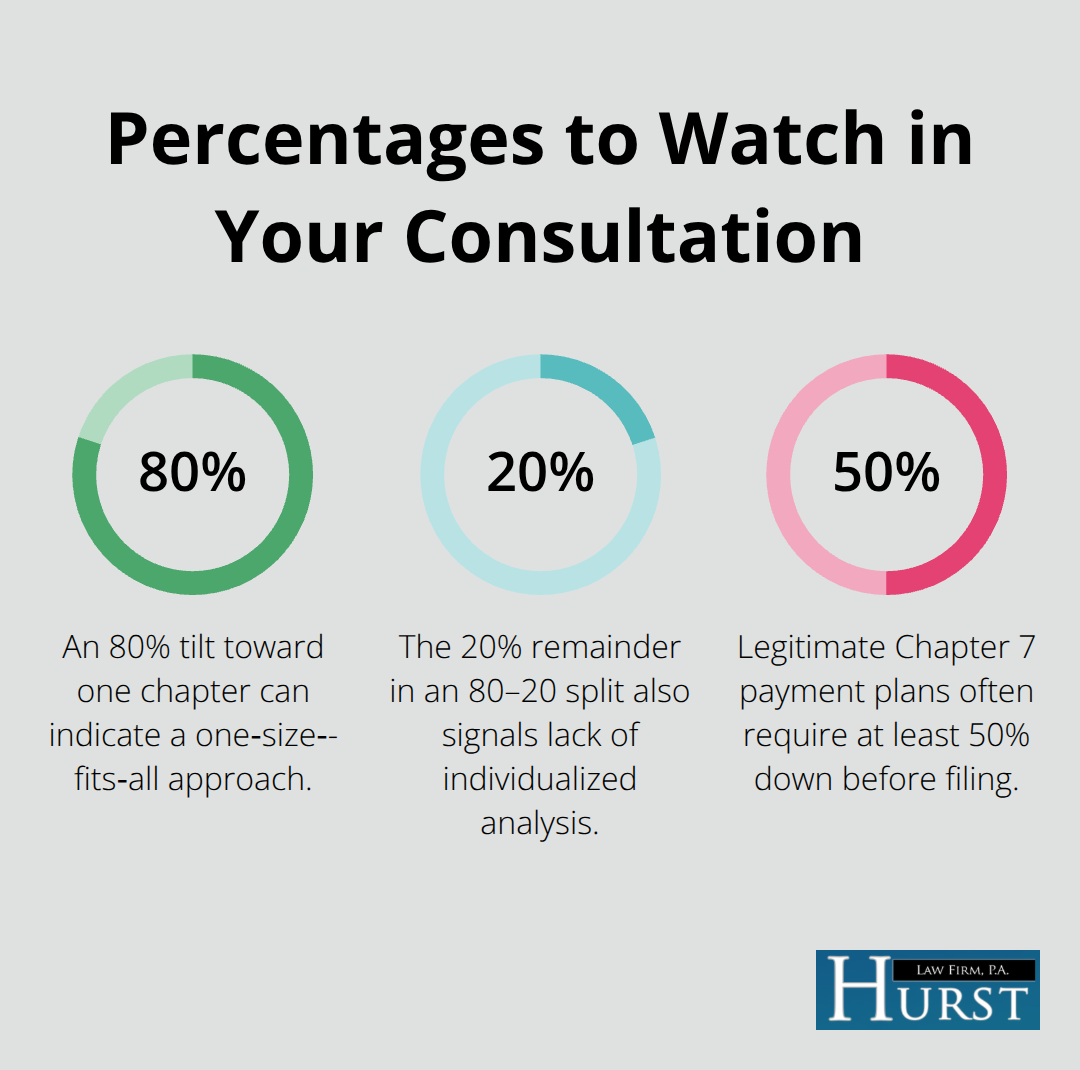

Ask the attorney: What percentage of your Memphis clients file Chapter 7 versus Chapter 13? If the answer is consistently 80-20 in either direction, that signals bias rather than individualized analysis. The right answer depends on your specific situation: whether you own a home facing foreclosure, whether you have a car loan you want to keep, and whether you have non-exempt assets the trustee could liquidate.

An honest attorney will explain why Chapter 13 might actually save your house during a foreclosure crisis, even though it requires a three-to-five-year repayment plan. Conversely, they’ll explain when Chapter 7 makes sense because most of your debts are medical or credit card debt with no assets at risk. Request that the attorney walk through how they’d approach your specific facts-not generic explanations. If they can’t articulate clear reasoning for recommending one chapter over another within 15 minutes of discussing your situation, they’re not thinking critically about your case.

Bankruptcy Law Focus and Professional Involvement

Bankruptcy law has changed substantially since the 2005 reforms, and it continues evolving through court decisions and trustee office interpretations. An attorney practicing bankruptcy for two years versus fifteen years will handle your case differently. That said, years alone don’t guarantee competence-an attorney with 20 years of real estate law who recently added bankruptcy as a sideline is worse than a five-year bankruptcy attorney.

Ask specifically: What percentage of your practice is bankruptcy law? The answer should be at least 75-80% for someone handling your case. Also ask about their involvement in professional organizations like the National Association of Consumer Bankruptcy Attorneys (NACBA). Membership signals commitment to staying current through continuing education and ethical standards.

Request references from clients who filed cases similar to yours within the last two years-not generic testimonials, but actual contact information you can verify. When you speak with former clients, ask whether the attorney explained the consequences of filing (credit impact, asset loss, discharge timeline) honestly or oversold the benefits. A quality Memphis bankruptcy attorney will tell you what bankruptcy cannot do-it won’t eliminate student loans, spousal support, or child support obligations-as clearly as what it can do.

Understanding an attorney’s experience and approach to case selection sets the foundation for your bankruptcy journey. The next step involves evaluating how they structure their fees and what costs you’ll actually pay throughout your case.

Understanding Bankruptcy Costs in Memphis

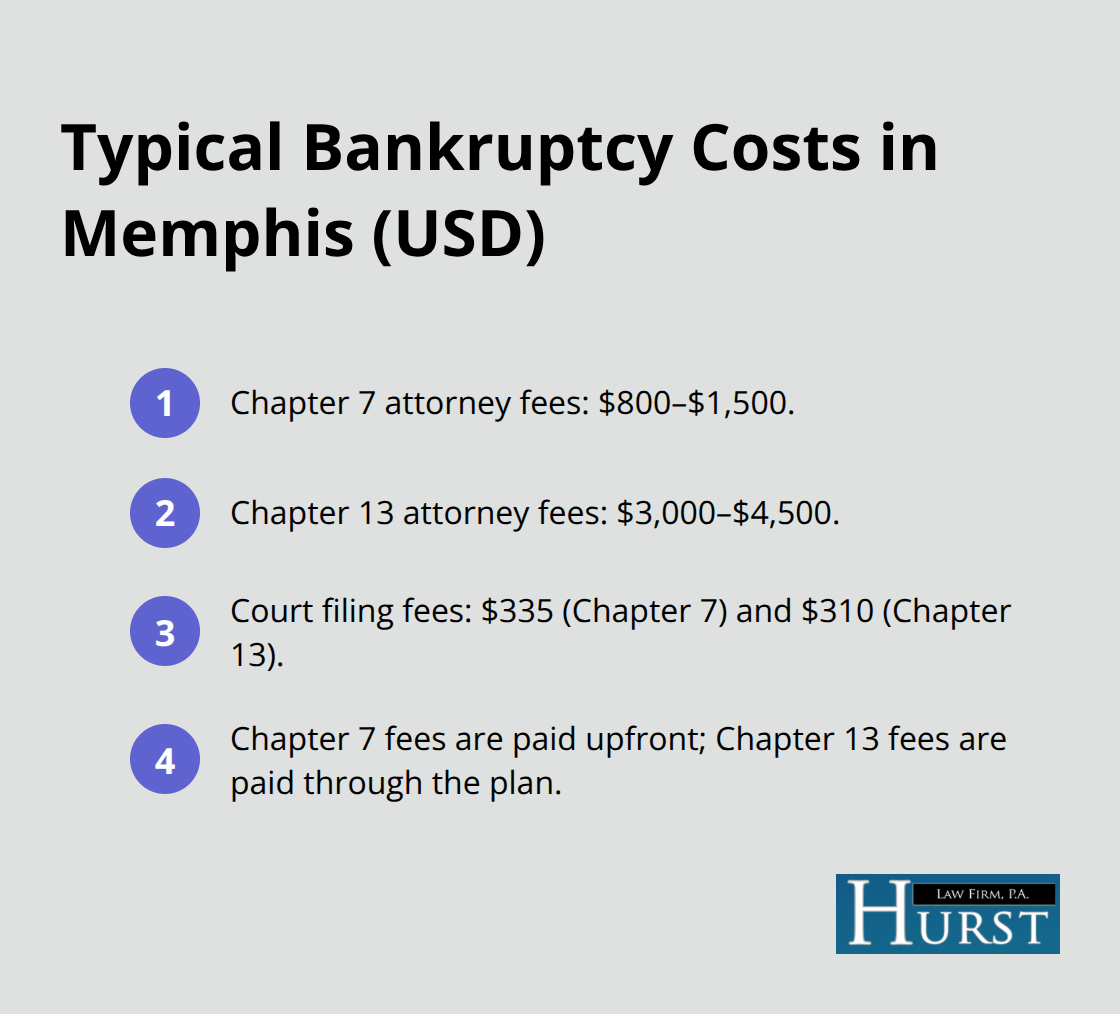

Chapter 7 bankruptcy attorney fees in Memphis range dramatically depending on the chapter you file and the attorney’s experience level. Chapter 7 cases typically cost between $800 and $1,500 in attorney fees, while Chapter 13 cases run $3,000 to $4,500 on average. Court filing fees add another $335 for Chapter 7 and $310 for Chapter 13, though many courts allow you to pay filing fees after you submit your petition.

The critical distinction is how these costs get paid: Chapter 7 requires upfront payment before filing, while Chapter 13 allows the trustee to deduct your attorney fees from your repayment plan itself, meaning you spread payments across three to five years without writing a large check immediately.

Flat Fees Versus Hidden Charges

When you meet with a Memphis bankruptcy attorney, ask exactly how they structure their fee. Some firms quote a flat fee covering all work through discharge, while others charge hourly rates for Chapter 7 cases. Flat fees are superior because you know the total cost upfront and the attorney has no incentive to drag out your case. Ask specifically whether the quoted fee includes preparation of all required documents, attendance at your 341 meeting, communication with the trustee, and representation if creditors object to your discharge.

Some attorneys quote a base fee then tack on $500 to $1,000 for document preparation, credit counseling course enrollment fees, or trustee objection handling. These hidden costs transform what seemed like an $850 Chapter 7 case into a $1,400 reality. Beyond attorney fees, confirm whether the firm charges for credit counseling courses (typically $50 to $100) or debtor education courses (another $50 to $100), since these are mandatory but sometimes bundled into the total cost and sometimes billed separately.

Payment Plans and Upfront Requirements

Ask whether payment plans exist for Chapter 7 if you cannot pay the full fee upfront, though legitimate firms will require at least 50 percent down before filing. If an attorney offers zero-down Chapter 7 representation, they are likely cutting corners or planning to file incomplete documents that the trustee will catch later, creating delays and additional costs for amendments.

For Chapter 13, the real advantage emerges: request a detailed breakdown of how your monthly plan payment divides between the trustee fee (typically 10 percent of your plan payment), the attorney fee (paid through the plan without additional money from your pocket), and your actual debt repayment. Some Chapter 13 plans allocate 40 to 50 percent of your monthly payment to trustee and attorney fees while your creditors receive minimal distribution, which signals either poor case planning or an attorney maximizing their take at your expense.

Understanding fee structures protects you from surprises during your bankruptcy journey. The next critical conversation with your attorney should focus on what actually happens during the filing process and how long you’ll remain in bankruptcy before receiving your discharge.

Timeline and Document Requirements for Your Memphis Bankruptcy Case

A Chapter 7 bankruptcy in Memphis concludes within three to four months from filing to discharge when you submit complete and accurate documents upfront. The U.S. Bankruptcy Court for the Western District of Tennessee processes Chapter 7 cases efficiently with correct paperwork, but incomplete schedules, missing tax returns, or undisclosed assets force amendments that extend your case by two to six months. Chapter 13 cases operate on a longer timeline because you enter a three-to-five-year repayment plan, meaning your case doesn’t close until you complete all plan payments or receive a discharge earlier if circumstances change. Ask your Memphis bankruptcy attorney about their actual average timeline from recent cases in your specific division of the Western District of Tennessee, not what the court’s theoretical timeline suggests. The difference between three months and nine months matters significantly when creditors continue calling or wage garnishments remain in place while your case drags on.

What Documents You Must Provide Before Filing

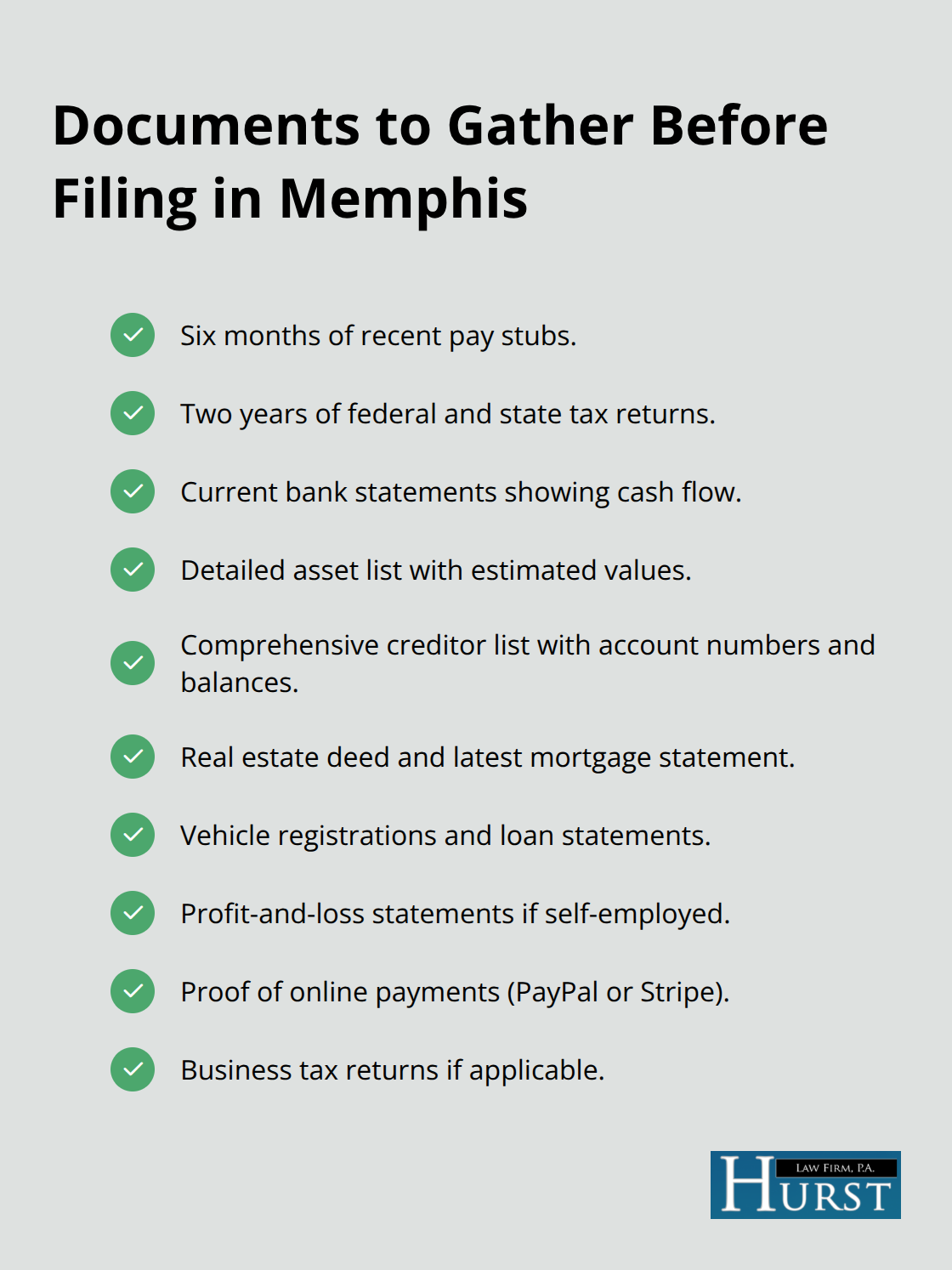

Your attorney will request comprehensive documentation before filing your petition, and the quality of what you provide directly determines whether your case moves smoothly or gets derailed. Collect six months of recent pay stubs, two years of complete tax returns (both federal and state), current bank statements showing cash flow, a detailed list of all assets with estimated values, and a comprehensive creditor list including account numbers, balances, and current payment status. If you own real estate, bring the deed and most recent mortgage statement. If you own vehicles, bring registration documents and loan statements.

Self-employed individuals must provide profit-and-loss statements for the past two years, documentation of client payments through online platforms like PayPal or Stripe, and any business tax returns. The court requires you to list every single creditor, even debts you dispute or family loans, and omitting creditors can result in those debts surviving your discharge, defeating the entire purpose of filing. Clients sometimes struggle when they thought certain debts didn’t matter or forgot about old medical bills sent to collection, then discovered months later that those debts weren’t discharged.

How Often Your Attorney Will Communicate With You

Communication frequency during your case should be clarified upfront because some attorneys go silent after filing except for the 341 meeting, while others provide monthly updates. Ask whether your attorney will contact you proactively about trustee requests or whether you’ll receive a generic email saying you must respond within ten days. Request direct contact information for your attorney or a designated staff member who handles client communication, and confirm whether phone calls get returned within one business day or whether email is the only contact method.

Preparing for Your 341 Meeting and Beyond

The 341 meeting itself typically lasts five to fifteen minutes, though your attorney should prepare you thoroughly beforehand. They should explain exactly what the trustee will ask, what answers you should provide, and what documents to bring. Establish expectations about post-341 communication as well, particularly for Chapter 13 cases where the trustee may request additional documentation or propose plan modifications during your repayment period.

Final Thoughts

The questions you ask during your Memphis bankruptcy attorney consultation directly determine whether you receive competent guidance or costly mistakes. Focus on three core areas: local court experience with Chapter 7 and Chapter 13 cases, transparent fee structures with no hidden charges, and realistic timelines based on actual recent cases. An attorney who handles dozens of Memphis bankruptcy cases annually, explains their fee breakdown clearly, and commits to personal involvement in your 341 meeting will protect your interests far better than someone treating bankruptcy as a sideline practice.

Bankruptcy filing happens rarely in most people’s lives, and the decisions made during your case affect your credit for seven to ten years. An attorney who honestly explains what bankruptcy cannot do-eliminate student loans, spousal support, or child support-demonstrates integrity. One who oversells benefits or pushes you toward Chapter 13 when Chapter 7 fits your situation better prioritizes their fees over your financial recovery.

After your initial consultation, request a written fee agreement before committing, and verify that the attorney’s license is current through the Tennessee Board of Law Examiners. Contact Hurst Law Firm, P.A. to schedule your consultation and begin moving toward the financial stability you deserve.